All the President's Budget Gimmicks

The Trump Administration recently released its full Fiscal Year (FY) 2018 budget proposal, which details the President’s policies for federal spending and revenue over the next ten years and proposes to put the budget on a path toward balance.

Prior to the budget, we warned of eight possible “budget gimmicks” that could be used to make the budget appear more responsible than it is. Though the budget incorporates a number of smart policies, it sadly relies on a number of these gimmicks, including:

- Rosy Growth Assumptions

- Arbitrary Policy Expiration Dates and Timing Shifts

- Magic Asterisks and Unspecified Savings

- Unrealistic Policy Assumptions

- Double Counting

- An Omitted Tax Plan

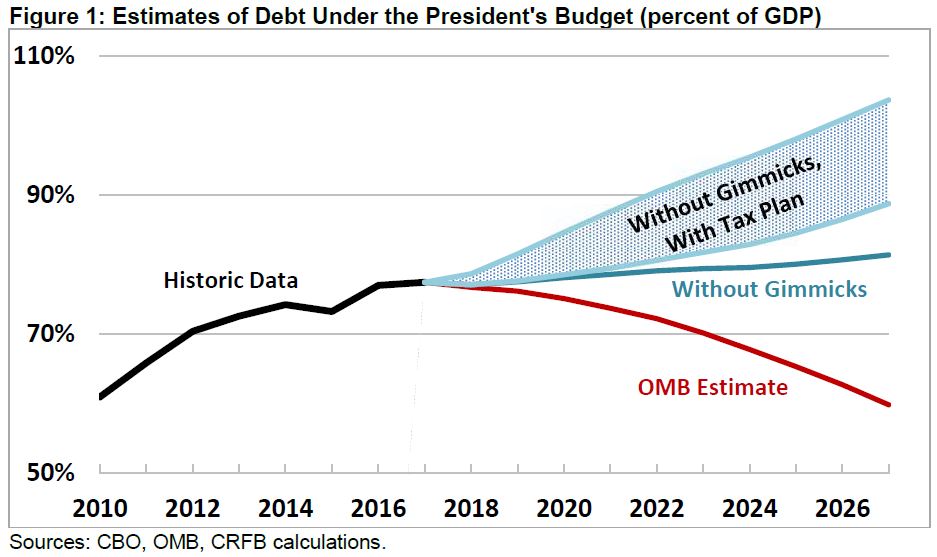

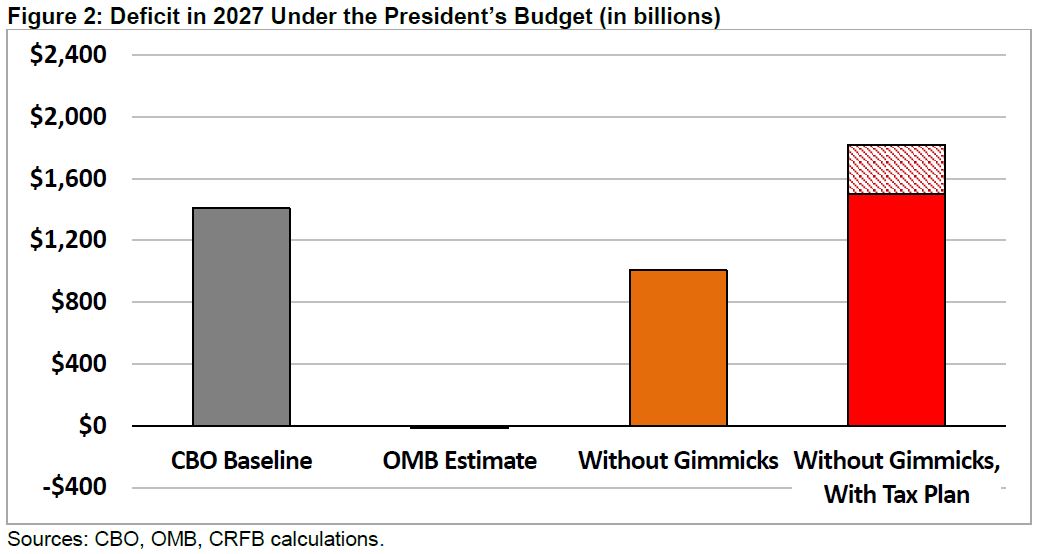

Added together, these gimmicks reduce projected debt under the President’s budget by at least $4.2 trillion and possibly over $10 trillion. This means debt would more likely rise to 81 percent of Gross Domestic Product (GDP), or perhaps even 104 percent, by 2027 rather than falling to 60 percent as in the President’s budget. It also means deficits in the final year will total $1.0 trillion, or as much as $1.8 trillion, rather than the budget reaching balance.

Rosy Growth Assumptions ($2.7 trillion)

One gimmick we warned about prior to the release of the President’s budget was the use of rosy economic growth assumptions to mask projected deficits. While this gimmick is common in small doses among past President’s budgets, the FY 2018 budget takes it to a whole new level.

Over the next decade, the Congressional Budget Office (CBO) projects real long-term economic growth will reach 1.9 percent per year while other private and public forecasters estimate growth rates between 1.6 and 2.1 percent per year. The President’s budget assumes 3 percent growth, an estimate far outside of the mainstream. As we’ve shown before, there is little historic precedent for this level of growth given current demographics, and achieving it would require a combination of very strong pro-growth policy and extremely good luck.

The President’s rosy growth assumptions matter because projections of economic growth significantly impact the projected fiscal outlook. Faster growth means more revenue collection as well as higher GDP and thus less debt as a share of the economy.

As we estimated recently, debt under the President’s budget would be about $2.7 trillion higher using CBO assumptions. As a result, debt would remain roughly stable at today’s level rather than falling below 60 percent of GDP as the budget claims.

To be credible, the President’s budget should rely on reasonable growth assumptions that are similar to those put forward by CBO and other forecasters, adjusted based on established economic evidence to reflect the impact of the budget’s policy proposals. This budget does not adhere to that practice.

Arbitrary Policy Expiration Dates and Timing Shifts ($50 billion)

In our paper “Eight Gimmicks to Look Out For This Budget Season,” we warned about the possibility of the budget using arbitrary policy expirations or unjustified timing shifts to make ten-year budget numbers look better. These gimmicks either mask costs that the Administration intends in the future or play games with when the government pays or receives money.

While the President’s budget does not have any massive timing gimmicks, it contains a few small ones.

For example, the budget proposes a timing shift to net $5 billion in savings by accelerating Pension Benefit Guarantee Corporation (PBGC) premium payments from FY 2028 to FY 2027. The $5 billion of “savings” this produces within the ten-year window would be lost in the following year.

Other one-time policies include the President’s infrastructure plan that stops spending money after 2026, the sale of half of the Strategic Petroleum Reserve, and a few other assets sales and privatizations. These aren’t necessarily gimmicks, but they do make the near-term deficit seem lower than the structural deficit would be in the long term. We don’t count these as gimmicks for the purposes of this paper.

When it comes to arbitrary expirations, the President’s budget is relatively pure compared to past budgets. However, it does extend a number of programs in the Medicare Access and CHIP Reauthorization Act of 2015 only through 2019. The proposal costs about $10 billion but if extended permanently would cost around $50 billion after interest.

Magic Asterisks and Unspecified Savings ($930 billion)

Another gimmick we warned about in our paper was the use of “magic asterisks,” where a budget takes credit for savings without specifying the policies to produce them.

President Trump’s FY 2018 budget includes one gigantic magic asterisk in the form of unspecified non-defense discretionary (NDD) spending cuts.

While the budget is extremely specific about the $54 billion of proposed cuts in 2018 – which would likely save about $550 billion if continued over a decade – it then assumes deep further cuts with no specificity through a “two-penny” plan.

By cutting nominal NDD spending by 2 percent each year, the budget would ultimately reduce NDD levels by 40 percent in 2027, even though the specified cuts only total 10 percent of NDD spending. The remaining cuts come from two sources. First, the budget essentially assumes each agency would be subject to a ten-year spending freeze – with no adjustments for inflation or cost changes and no explanation for how these savings would be met. Much more significantly, the budget establishes $730 billion of cuts that are not even distributed by agency and instead categorized as “allowances” in the budget.

As a result, there are about $850 billion in unspecified cuts to NDD outlays. Including interest, these unspecified cuts claim savings of about $930 billion over ten years.

Unrealistic Policy Assumptions ($180 billion)

Another gimmick we warned about was unrealistic policy assumptions. In this case, the policies are specific, but either the policy itself is unachievable or the savings estimated are unrealistically high.

The President’s budget includes two of these gimmicks. The first invests $100 million per year for five years in pilot projects intended to increase workforce participation among potential Supplemental Security Income (SSI) and Social Security Disability Insurance (SSDI) beneficiaries. This is a smart reform that should ultimately save money. However, the Administration expects this policy to save nearly $50 billion in the last five years of the decade – an unrealistically high return in that period of time.

The President’s budget also assumes that the Administration would cut all improper payments in half with program integrity funding, saving $139 billion. This is an arbitrary assumption that is unlikely to be achieved. President Obama’s last budget contained only $11 billion in program integrity savings, and with deep cuts in agency funding even achieving that much could be challenging. More program integrity savings may be possible, but the President’s budget does not show how they could be achieved – and it’s not clear in any circumstance one could achieve the level of savings in the budget. Therefore, we assume at most 10 percent of the savings will be realized, on net.

Including interest, these gimmicks improve the budget’s numbers by about $180 billion over ten years.

Double Counting ($0-$650 billion)

Though a less common gimmick in detailed budgets, double counting savings is another way to artificially improve budget numbers.

The President’s budget may double count savings from Medicaid, though it is not clear if it does and to what extent. The budget proposes $610 billion of Medicaid savings, which would come from a per-capita cap and/or block grant, but is not specific on the details. At the same time, it assumes a generic Affordable Care Act “repeal and replace” plan and makes it clear that the President supports something similar to (and negotiated from) the House-passed American Health Care Act (AHCA).

Importantly, the AHCA already includes $834 billion of Medicaid savings, some of which would come from a ‘per capita cap’ and some of which would interact with such a cap. In the final analysis, there may very well be overlap between the $610 billion of assumed Medicaid savings and the $1.25 trillion of assumed spending cuts from repeal and replacement.

In fact, Office of Management and Budget (OMB) Director Mick Mulvaney, in his testimony in front of the Senate Budget Committee, said:

“The number I've heard is $1.4 trillion, and that's drawn from the $800 billion from the AHCA and $600 billion from some of the other reforms that we proposed…However, you can't add those two numbers together because there are components of those that overlap…It's someplace between $800 and $1.4 trillion. So, if you wanted to round the difference off, what is that, $1.1 trillion?”

With interest, this suggests between $0 and $650 billion of double counting. For the purposes of this analysis, we assume the budget contains $1.1 trillion in total Medicaid savings, and thus there would be some double counting.

Bonus Gimmick: An Omitted Tax Plan (Possibly $2.1 to $6.2 trillion)

While we did not have the foresight to warn about it, the budget’s treatment of the Administration’s tax plan likely qualifies as at least one type of budget gimmick, if not more. The budget assumes no revenue loss from the Administration’s tax cut/reform plan and actually assumes revenue gains when economic growth is incorporated. This qualifies as an omission, double counting, inconsistency, or potentially some combination.

The budget includes no specific proposals for tax reform despite tax reform being a top priority for the Administration. While the budget does include bullet points consistent with the tax plan summary the Administration released early in April, it assumes neither a cost to this plan nor a way to pay for it.

Based on the available details, we estimated the plan the Administration has put forward so far would most likely cost in the range of $5.5 trillion. Failure to incorporate that cost or further details means that their budget has a major (and potentially very costly) missing piece.

Even assuming the Administration will ultimately achieve revenue neutrality in its tax reform plan, there is still potential double counting. Several members of the Administration, most significantly Treasury Secretary Steve Mnuchin, have said the tax plan would be paid for in part with the revenue gains from economic growth. Yet the budget assumes all revenue gains from economic growth go to deficit reduction.

This means that there is an inconsistency between the Administration’s position outside of the budget and the one put forward within the budget. Assuming that Secretary Mnuchin’s position is the official policy of the Administration – an assumption which is not at all clear based on press reports – there is a sort of double counting between the budget and the tax plan outside of the budget.

Removing double counting of economic growth or inconsistency could add $2.1 trillion to the debt. Incorporating all the available details from the tax plan into the budget could instead add $6.2 trillion, with interest.

Adding It All Up – How Much Does the Budget Really Reduce Deficits and Debt?

On paper, the President’s budget would significantly reduce deficits, putting the federal budget in balance by 2027 while reducing debt from 77 percent of GDP this year to 60 percent by 2027. However, these much-improved numbers rely heavily on the gimmicks mentioned above.

When the rosy economic assumptions, timing gimmicks, magic asterisks, unrealistic policy assumptions, and double counting (taking the midpoint) are removed, ten-year deficits would increase by $4.2 trillion above what the budget projects on paper. The budget would show a deficit of $1.0 trillion in 2027 rather than a small surplus and would show debt rising to 81 percent of GDP by 2027 instead of falling to 60 percent. This would still be an improvement over CBO’s projection that debt will rise to 89 percent of GDP by 2027, but it would be much less so than the Administration purports.

These numbers could be worse if the Administration’s tax plan is incorporated. Depending on how much revenue is lost, incorporating tax reform could add another $2.1 to $6.2 trillion to the debt through 2027, increasing debt in that year to between 89 and 104 percent of GDP. With that tax plan, the total deficit could be between $1.5 and $1.8 trillion by 2027.

Note that all of these estimates assume the gimmicks are fully removed unless otherwise specified; in reality, behind the unrealistic numbers might be a much smaller realistic impact (for example, the budget may be modestly pro-growth relative to current law).

With the gimmicks removed, the President’s budget would at best show a much more modest improvement in our fiscal situation than the budget says, and it would at worst significantly increase the debt.

* * * * *

The United States faces serious fiscal challenges with a high and rising debt. Utilizing gimmicks to the extent that this budget does limits the ability of the American people to take the Administration’s commitment to fiscal responsibility seriously. Reducing deficits and debt on paper means very little if done so through gimmicks. Policymakers are far better off putting forward an achievable (and responsible) fiscal goal and a realistic plan to meet it than putting forward an overly ambitious fiscal goal that can only be met with budgetary sleights of hand.