Five Gimmicks That May Hide the True Costs of Tax Reform

The budget resolution recently passed by Congress sets the stage for fast-track tax reform legislation (a process known as reconciliation) that could add up to $1.5 trillion to the debt over a decade. However, due to the limitations of the reconciliation process, tax reform cannot technically add to the deficit beyond the ten-year window.

Such an increase in debt would come at a time when it is higher than any other time outside of World War II and rising unsustainably. The budget attempts to justify the $1.5 trillion cost by arguing that it will not truly increase deficits, relying on dubious assertions and unrealistic assumptions about economic growth.

Unfortunately, the actual legislation might be even worse – policymakers may use gimmicks to make the legislation appear to add “only” $1.5 trillion to deficits this decade and nothing in future decades while masking significant further costs.

As lawmakers are set to unveil their first tax bill this week and mark it up in the Ways and Means Committee over the coming weeks, it is important to watch out for gimmicks that attempt to justify a $1.5 trillion increase in the debt and make the ultimate cost of tax reform even larger.

This paper outlines the types of gimmicks that may be used to hide the true costs of tax reform in this decade and in the future. The five gimmicks we warn about include:

- Justifying $1.5 Trillion in Additional Debt

- Arbitrary Tax Cut Sunsets

- Arbitrary Phase-Ins

- Rothification and Other Timing Gimmicks

- Delayed or Unsustainable Offsets

Congress must avoid the urge to rely on any of these gimmicks and instead pursue honest and fiscally responsible tax reform that grows the economy without ballooning the national debt.

Gimmick #1: Justifying $1.5 Trillion in Additional Debt

Congressional Republicans have asserted that the $1.5 trillion tax cut would not actually increase deficits by arguing roughly half a trillion represents tax cuts that would have occurred anyway (the current policy rationale) and another trillion or more would come from dynamic feedback effects from faster growth (the rosy growth rationale). Both of these arguments are flawed and are gimmicks intended to hide the true costs of tax reform.

The Current Policy Rationale

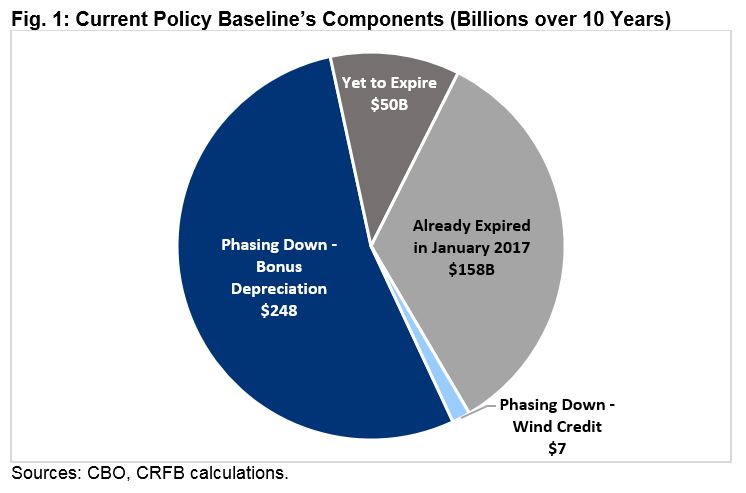

Several tax breaks either expired in 2016, will expire in 2017, or are set to phase down over the next few years. Collectively, Congress has been referring to these as "current policy." Extending all of these tax breaks at 2016 levels would cost about $460 billion over a decade, leading some to argue that under a current policy baseline, $1.5 trillion of tax cuts only “really” costs $1 trillion. This argument is flawed for two main reasons.

First, assuming the continuation of expired/expiring policies that were originally scored as temporary violates the integrity of the budget process by making the true costs of tax cuts “disappear.” These tax breaks are not included in the baseline as permanent costs because they were counted as temporary when they were enacted or extended. There is a valid argument that budget rules should change to count temporary tax breaks as permanent when they are enacted; however, counting them as permanent only after they are enacted allows policymakers to add to the debt without ever having to recognize the true cost.

Second, most of the tax breaks in question have either already expired or are scheduled to phase down as intended by Congress. The 2015 PATH Act explicitly set a number of tax breaks on a path to expire permanently (while permanently extending others) and explicitly phased down the size of bonus depreciation from covering 50 percent of investment costs to covering 30 percent by 2019 and then 0 percent thereafter. Senate Finance Committee Chairman Orrin Hatch (R-UT) described the bill as “putting an end to the repeated tax extenders exercise that has plagued Congress for decades.” Even assuming bonus depreciation continues to cover 30 percent of costs, the total value of extending tax breaks not explicitly intended to expire is closer to $200 billion – not $500 billion.

Using the “current policy rationale” that expirations should not matter would be particularly dubious if tax reform/cuts also included expiring provisions to keep its cost under $1.5 trillion. Presumably, there would be pressure to extend these provisions under a new “current policy” argument years down the road.

The Rosy Growth Rationale

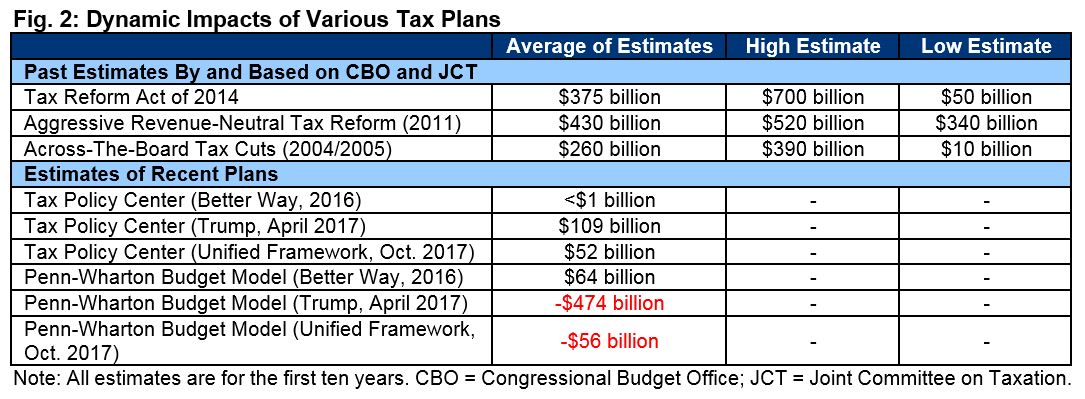

Well-designed tax reform has the potential to improve economic growth and thus generate some additional revenue from “dynamic feedback.” Advocates of tax reform have claimed such feedback could total $1 trillion or even $2 trillion. These numbers are highly unlikely and certainly should not be counted on.

In reality, dynamic feedback for a well-designed tax reform plan is more likely to produce closer to $300 or $400 billion of dynamic feedback over a decade, and debt-financed tax cuts may ultimately slow economic growth over the medium and long term and result in little net positive feedback at all.

Recent estimates of the unified framework – from the Tax Policy Center and the Penn-Wharton Budget Model, which both account for the increased debt from a tax cut – find that this particular framework would result in dynamic feedback of between $52 billion and actually adding $56 billion to the cost.

The below table offers a sense of possible dynamic scores based on estimates of past tax reform plans. Note that the high-end estimates generally assume future deficit-reduction policy, rather than just incorporating the effect of the tax plan itself:

Models that estimate much greater dynamic effects of tax cuts/reform generally do not incorporate any negative effects of debt. Such models either assume debt will be stabilized through future policy changes, assume an unlimited supply of savings, or ignore financing altogether. The Congressional Budget Office (CBO) and other economic studies show that deficit-financed tax cuts have small or negative effects on long-term growth rates because positive effects from lower rates and other tax cuts will be offset by the economic drag from increased government borrowing.

There is a role for dynamic scoring in this debate because economic growth is a key reason to pursue tax reform. However, only official scores from the Joint Committee on Taxation or CBO should be relied upon. Claims of deficit neutrality that rely on overly optimistic dynamic estimates from outside groups should be viewed with skepticism. There is little chance that a $1.5 trillion net tax cut could be paid for fully with dynamic feedback.

Gimmick #2: Arbitrary Tax Cut Sunsets

While there is no good case for even a $1.5 trillion tax cut, policymakers are likely to use various gimmicks to make the “actual” tax cut even larger.

One way in which policymakers may try to fit a larger tax cut into the $1.5 trillion price tag is through arbitrary “sunsets” that allow certain tax cuts to expire before the end of the budget window in order to lower the overall ten-year cost of the package.

Sunsets could also be used to get around the reconciliation procedure’s limitations – specifically the Byrd Rule. The Byrd Rule, which requires that any changes passed through reconciliation do not add to long-term deficits, is one of the best defenses against an irresponsible tax bill. However, it can be circumvented by allowing expensive provisions to expire at the end of the budget window – eliminating their costs past the first ten years. Such sunsets would obscure the bill’s long-term cost and create the expectation that Congress will continue the provisions without offsets, as was the case with the 2001/2003 tax cuts.

There is a high likelihood that Congress will rely on sunsets to make a $1.5 trillion ten-year tax cut appear to cost nothing in the second decade – with the assumption that future Congresses will extend various debt-increasing tax cuts before they expire as they did with the 2001/2003 tax cuts.

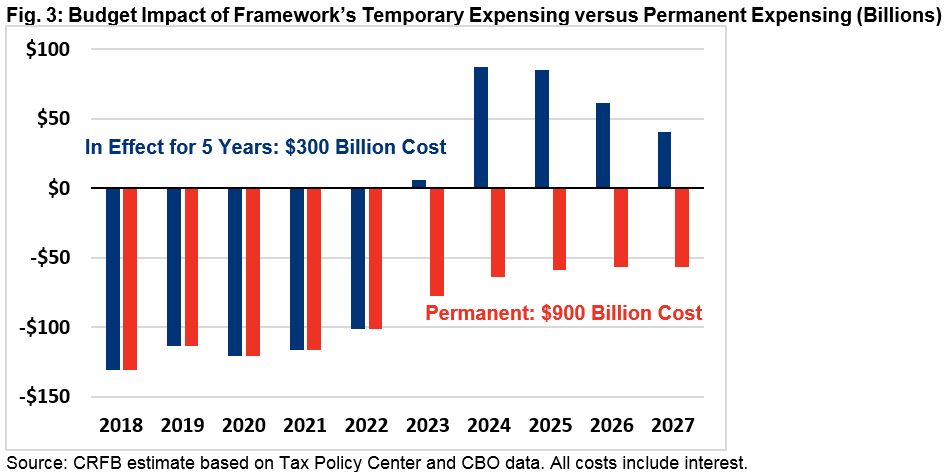

The “Big Six” has already signaled they will pursue at least one expiration to lower ten-year and long-term costs. Their unified framework proposed to allow corporations to immediately deduct the cost of equipment – a provision known as expensing – but proposed that this measure be in effect for "at least five years" rather than permanently.

In addition to undermining the growth impact of expensing, making this provision temporary obscures the cost. While five years of equipment expensing would cost $300 billion, including interest, permanent expensing would cost three times that.

Relying on arbitrary sunsets to limit the costs of tax breaks would be a gimmick in any circumstance, but it is particularly egregious given the “current policy rationale” that essentially says that past and current sunsets should not be counted as such. The current policy rationale creates the precedent that future legislation can eliminate the sunsets (and the “savings” achieved by the sunsets) without ever being charged with a cost.

Gimmick #3: Arbitrary Phase-Ins

One way to reduce the ten-year cost of a tax cut is to delay or phase in its implementation. While sometimes there is a good rationale to phase in a tax cut, the goal is often simply to make the ten-year cost small relative to the steady state cost. A tax bill that adds $1.5 trillion to the debt over a decade but $300 billion to $400 billion in the last year alone, for example, would likely set the stage for massive debt increases in the future.

For example, the 2001 tax cuts called for rate reductions to take place gradually over five years, with the top rate falling from 39.6 percent in 2000 to 38.6 percent in 2001, 37.6 percent in 2004, and 35 percent by 2006; other rates fell on a similar schedule. These rate reductions lost about $60 billion of revenue when fully phased in but only $20 billion in the first year., This phase in effectively reduced the cost of the tax cut by $150 billion without reducing its actual size. (Note that future legislation ultimately accelerated this phase-in.)

While not all phase-ins are gimmicks, efforts to use phase-ins to obscure structural costs should be avoided.

Gimmick #4: Rothification and Other Timing Gimmicks

One way to raise revenue in the near term without raising taxes or cutting tax breaks is by shifting the payment of taxes from the future to the present. These gimmicks exploit the ten-year budget window used to evaluate legislation by changing when taxes are paid rather than the amount of taxes paid, bringing revenue into the window sooner than it would have otherwise. These timing shifts improve the near-term impact of the bill to reduce the cost of the bill within the budget window at the expense of the long term.

One particularly egregious gimmick is something called “Rothification,” which would encourage or require people to save for retirement in Roth-style accounts (where contributions are post-tax and proceeds are tax-free) instead of traditional tax-deferred retirement accounts (where contributions are pre-tax and proceeds are taxed). Counterintuitively, policymakers could expand the limit on contributions to Roth-style accounts and still raise revenue in the near term – even as losses compound in the future. Even without expanding the tax break, moving people from traditional pre-tax to Roth-style retirement accounts could lose massive amounts of revenue in the future – at least as much and likely more than what is raised up front through the timing shift.

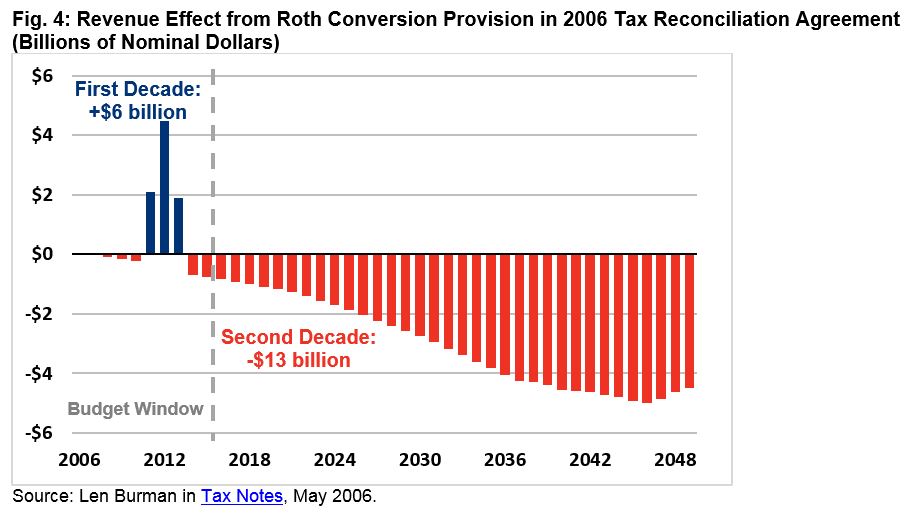

For example, then-director of the Tax Policy Center Len Burman modeled the Roth conversion provision in the Tax Increase Prevention and Reconciliation Act of 2005, which allowed the conversion of traditional Individual Retirement Accounts (IRAs) into Roth-style IRAs. While revenue would increase by $6 billion in the budget window, the loss in the second decade is more than double the size. The Rothficiation under discussion for tax reform is potentially several orders of magnitude worse, resulting in much more revenue loss than this example.

While there may be a policy rationale for Roth-style accounts, if the funds are used for rate reduction rather than set aside, then such Rothification is mainly a timing gimmick.

Gimmick #5: Delayed or Unsustainable Offsets

One way to reduce the reported cost of tax reform is by including unpopular offsets that do not take effect until several years in the future. The horizon between passage of tax reform and implementation can allow Congress numerous chances to cancel offsets should they prove unpopular. The most egregious version of this gimmick would be to enact provisions with the expectation and intent that Congress will repeal them before they take effect; even if policymakers today intend to allow an unpopular provision to take effect, delaying its enactment reduces the likelihood that it will ever actually take effect.

As one example, the 2010 Affordable Care Act (ACA) called for a tax on high-cost health insurance plans (the “Cadillac Tax”) to go into effect in 2018 – over seven years after the ACA’s enactment and four years after new subsidies were in place. This provision has since been weakened and its implementation delayed to 2020, with policymakers from both parties calling for further delay or repeal.

Should tax reform legislation propose to repeal or severely limit a popular tax break starting several years in the future, it might meet the same fate. Similarly, if Congress proposes aggressive phase-ins or indexing that ultimately lead to an unsustainable policy, future Congresses are unlikely to let that occur. Unindexed caps or similar provisions could tee up a future Congress to enact “patches” that increase the limits in the future.

Watchers should beware of legislation that offers “goodies” up front but only includes “vegetables” a number of years in the future.

***

Despite Congress's unwillingness to pass a budget that requires tax reform to be at least deficit neutral, there is still time for lawmakers to reject both the justification of $1.5 trillion in additional debt and a deficit-increasing tax cut. Tax reform has significant potential to improve the economy and our fiscal situation; it should not be used as an excuse to cut revenue and should not be justified by gimmicks masking the true costs of additional debt.