Break Glass Here: A Responsible Plan to Combat the Next Recession

The United States is in the midst of one of the longest periods of sustained economic growth in its history, but there are signs that this prolonged expansion may be coming to an end. The inversion of the Treasury bond yield curve and recent Federal Reserve rate cut suggests that markets and experts are expecting the economy to soften. We need to be prepared to combat the next economic downturn.

Given today’s low interest rates, the Federal Reserve will have only limited ability to fight the next recession with monetary policy alone, and fiscal stimulus will almost certainly be needed. But debt is at post-World War II era record-high levels and growing rapidly, so any further expansions in the deficit must be enacted judiciously. Failure to stem rising debt levels will mean slower long-term economic growth and less fiscal space to respond to future recessions or other priorities and emergencies.

Still, policymakers should not allow the very serious threat of rising long-term debt to prevent them from considering near-term stimulus if the economy weakens substantially. In fact, we recommend that policymakers develop a “Break the Glass” stimulus package in advance of the next recession so that it can be activated quickly once the downturn begins. That plan should do the following:

- Increase spending and cut taxes through policies with high “bang for buck”

- Credibly ramp up stimulus as the economy is weakening and withdraw stimulus as the economy recovers

- Offset near-term deficit increases through gradual long-term deficit reduction

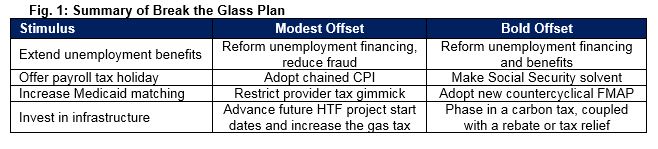

In this paper, we put forward an illustrative ”Break the Glass” plan that includes extended unemployment benefits, a payroll tax holiday, an increase in Medicaid matching to states, and new investment in infrastructure.

For illustrative purposes, we assume the package will cost about $600 billion, and we offer two possible offset packages. Our “Modest Offset” framework would couple each stimulus measure with a relatively conventional policy to cover its costs over ten years. Our “Bold Offset” framework would couple the policies with long-term structural reforms that will ultimately put the debt on a more sustainable trajectory.

Coupling short-term stimulus with long-term deficit reduction would help to support both short- and long-term economic growth and will leave future policymakers better equipped to combat recessions in the future.

Two Frameworks for a Break the Glass Plan

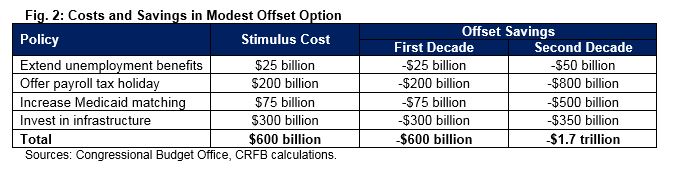

The exact size and composition of any stimulus package will depend on economic and political conditions of the next recession. Nevertheless, we expect a package will likely include spending for the unemployed, tax relief for workers, aid to states, and public investment. For illustrative purposes, we assume a simple and straightforward package that extends the availability of unemployment benefits, temporarily reduces the payroll tax, temporarily increases Medicaid payments to states, and invests in infrastructure. We assume this package will cost about $600 billion – nearly 3 percent of this year’s Gross Domestic Product – though it could be dialed up or down.

While it would be counter-productive to offset the cost of stimulus measures while the economy is in recession, it would be prudent to pay for their costs over time so they do not add to the debt. Ideally, a bill to rescue the economy would reduce debt over the long term, which would both improve long-term growth and leave the nation better prepared for future recessions.

We offer two options to offset our illustrative stimulus package over time. Specifically, we offer a Modest Offset option, which would pay for the policy over a ten-year window, and a Bold Offset option, which would both pay for stimulus and enact important long-term structural reforms.

Extend Unemployment Benefits

In most states, unemployed workers can qualify for up to 26 weeks of unemployment benefits. An extended benefit (EB) program also offers an additional 13 weeks to those in states with high unemployment rates, and lawmakers often offer additional weeks on an ad-hoc basis during economic downturns. Extending unemployment benefits both provides support to those unable to work and provides a temporary boost to the economy by giving money to unemployed workers to spend.

Our Break the Glass plan would modify the current EB program to offer additional weeks of unemployment benefits during longer or deeper economic downturns, taking the condition of the national as well as local economies into account. Specifically, state EB programs should be tiered so they offer more weeks when state and federal unemployment rates are higher and fewer weeks when they are lower. Over the course of an ordinary recession, this expansion would likely cost about $25 billion.

To ensure expanding unemployment benefits doesn’t add to the debt, our Modest Offset framework would reduce fraud and improper payments within the unemployment program and adjust its tax base. Currently, federal unemployment costs are generally financed by a 0.6 percent payroll tax on each worker’s first $7,000 of income. Reducing that tax rate to 0.2 percent while increasing the tax base to $40,000 and indexing it to wage growth would likely generate $20 billion to $30 billion over a decade.

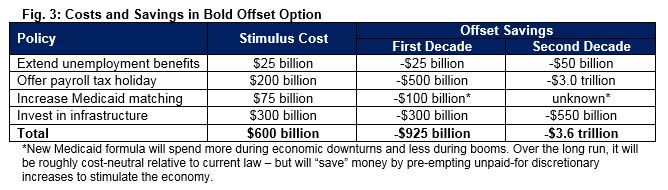

Our Bold Offset framework would include the above offsets but would also identify changes to the unemployment program to encourage and facilitate faster reemployment, such as providing reemployment bonuses, offering targeted wage insurance, subsidizing transitional jobs, and establishing personal reemployment accounts. Depending on net cost, these reforms might require further adjustments to the tax base.

Offer a Payroll Tax Holiday

One way to encourage more consumption and employment during a recession is to increase take-home pay. Our Break the Glass plan would include a temporary payroll tax holiday to reduce the payroll tax withheld from a worker’s wages. A temporary 2 percent reduction in the Social Security tax in the first year of a recession and 1 percent reduction in the second year, split evenly between employers and employees, would cost about $200 billion and widen Social Security’s 75-year actuarial shortfall by about 0.04 percent of payroll (2 percent).

To offset this cost and strengthen Social Security over the long term, our Modest Offset plan would adopt a more accurate measure of inflation – the chained Consumer Price Index (CPI) – for inflation-indexed provisions government-wide. The chained CPI is already used to index provisions in the tax code, and applying it to spending programs would save about $200 billion over a decade according to the Congressional Budget Office (CBO). Non-Social Security savings could be credited to the trust fund through a one-time general revenue transfer. Because these savings would materialize gradually, they would have virtually no effect on the economic recovery but would significantly reduce long-term deficits and would close about one-fifth of Social Security’s 75-year shortfall.

Under our Bold Offset plan, a temporary payroll tax holiday would be coupled with a comprehensive plan to restore 75-year solvency to Social Security through a combination of benefit adjustments, revenue increases, and changes to the retirement age. A well-designed reform plan would not only help the near-term economy but could also promote long-term economic growth by promoting work, savings, investment, and productive aging.

Increase the Medicaid Match to States

The federal government assists states in financing their Medicaid costs through a formula known as the Federal Medical Assistance Percentage (FMAP). While FMAP matching rates are based in part on state need, and therefore vary from state to state, they are not designed to significantly adjust due to changing macroeconomic conditions. As a result, states often have to raise taxes or cut services during recessions in order to afford their Medicaid programs, which can increase in cost during a recession due to a higher number of unemployed individuals who would otherwise receive coverage from employer-provided insurance plans.

In the last two recessions, the federal government temporarily increased FMAP payments to all states, with larger increases awarded to states with particularly high unemployment rates.

Under our Modest Offset plan, we would re-instate a version of the temporary FMAP expansion enacted under the American Recovery and Reinvestment Act of 2009, which we estimate would cost about $75 billion. To ensure these costs are not added to the debt, we would also restrict the ability of states to inflate their Medicaid matching rates through the use of provider taxes. CBO estimates that prohibiting this practice entirely would save over $50 billion per year once phased in. A much more gradual approach would be wise in order to avoid major disruptions to states and providers and allow the policy to go into effect without hurting the recovery or counteracting stimulus.

Instead of temporarily increasing the Medicaid match, our Bold Offset plan would permanently reform the FMAP formula so that it automatically adjusts payments to states based on local and national economic conditions.

In 2019, Matthew Fielder, Jason Furman, and Wilson Powell proposed a framework to increase states’ FMAP matching rates by 4.8 percentage points for every 1-percentage point increase in a state’s unemployment rate. Their proposal would measure this increase in unemployment relative to the 25th percentile of the state’s historic unemployment rate plus 1 percent; they estimate their proposal would cost roughly $200 billion over a decade. Similar proposals have been put forward by the Government Accountability Office (GAO) and other individuals and organizations.

We suggest setting the threshold somewhat higher than Fielder, Furman, and Powell (for example, at the median unemployment rate) and reducing the FMAP when unemployment rates are significantly below the threshold. Making the adjustment two-sided would ensure that the proposal provides short-term relief but does not increase the long-term debt. To achieve the same goal, policymakers could instead consider structuring FMAP increases as loans to states, reducing the average FMAP in concert with this policy change, or reducing the current 50 percent floor on FMAP payments so that states with high fiscal capacity cover a larger share of their own costs.

Invest in Infrastructure

During a recession, increased infrastructure spending can help create jobs and promote long-term economic growth. Since prices and interest rates are often low when economies are weak, recessions also provide an opportunity for the government to increase its return on investment. In addition, because most infrastructure spending takes years to fully outlay, it can continue to support the economy even after other stimulus measures end.

Our Break the Glass plan would appropriate about $300 billion in infrastructure spending, though the amount could be adjusted. These funds could support some combination of transportation infrastructure, green infrastructure, and improvements to energy grids, with a focus on projects that are “shovel ready” (especially repairs and improvements to existing infrastructure) or have a high economic return. The plan could include a combination of direct spending, support for states, public-private partnerships, and tax credits, as well as an infrastructure bank to facilitate more sustained investment.

To ensure the cost of new infrastructure spending is not added to the debt, our Modest Offset option would ensure some of the spending came from advancing the start date of future Highway Trust Fund (HTF) projects and would fund the rest with a gas tax increase. According to CBO, increasing gas and diesel taxes by 15 cents and indexing them to inflation would raise about $240 billion. To avoid disrupting the economic recovery, the gas tax could be indexed to inflation immediately, but any further increases could be postponed until the unemployment rate falls below 5 percent and phased in by half-a-cent per month.

Under our Bold Offset option, increased infrastructure spending could instead be offset by a carbon tax. CBO estimates a $25 per-metric-ton tax that goes into effect immediately and grows by about 4 percent per year would raise about $1.1 trillion over a decade. Realistically, it would take time to set up the infrastructure to tax carbon, and the initial tax could be set much lower with a schedule to increase substantially over time. In addition, a large share of the revenue from a carbon tax could also be used to provide tax relief to families and small businesses affected by higher carbon prices.

Fiscal Effect of Proposals

Our Break the Glass plan includes a number of features that could be dialed up or down depending on the needs of the economy. We estimate the illustrative version put forward in this memo would cost about $600 billion – mostly over a two-year period.

Both the Modest Offset and Bold Offset options would offset the cost of these policies over ten years and produce longer-term deficit reduction, though the Bold Offset option would provide more substantial deficit reduction over the long term.

The policies in the Modest Offset option are designed to offset the stimulus policies, so they would save roughly $600 billion over ten years despite mostly being implemented only once the stimulus has run its course. Since these policies generally save a growing amount over the longer term while the stimulus policies are temporary, they would likely generate $1.5 trillion to $2 trillion of savings in the second decade.

The Bold Offset option would save significantly more than the Modest Offset plan, particularly over the long run. While exact savings would depend on the details, we believe they could exceed $900 billion in the first decade and $3 trillion to $4 trillion in the second.

Importantly, these estimates are all conventional and do not account for the fact that the Break the Glass plan would likely increase the size of the economy both during and after a recession.

Conclusion

Responding to an economic downturn is one of the most basic functions of fiscal policy. However, our rapidly rising national debt and growing structural deficits due to the aging of the population, rising costs of health care, and stagnant revenue will make it much more difficult for policymakers to enact bold measures when we enter the next recession.

By having a Break the Glass plan ready to go, policymakers can respond to a recession in a fiscally responsible way that addresses the unsustainable growth of the long-term debt. Doing so will not only improve the recovery by reducing the negative effects of debt, but also will give the country more fiscal space to incur debt during recessions and crises that require large fiscal responses.

This paper offers two frameworks for policymakers to consider that would strengthen the economy during and after the next recession.