Analysis of CBO’s Updated Budget and Economic Outlook (August 2019)

Today, the Congressional Budget Office (CBO) released its updated Budget and Economic Outlook, showing that the national debt is on an unsustainable path and recent legislation has made an already challenging fiscal situation even worse.

CBO’s report shows:

- Under current law, debt held by the public will rise by more than $12.8 trillion over the next decade – from $16.5 trillion today to $29.3 trillion by 2029.

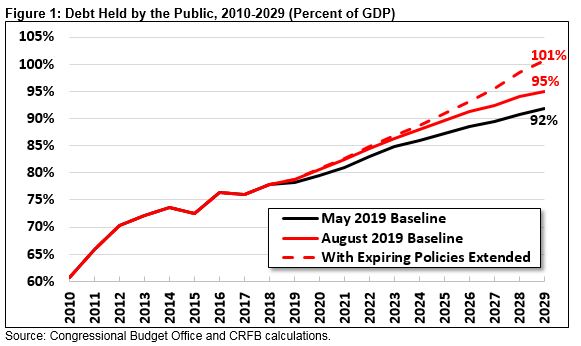

- Debt as a share of the economy will rise rapidly, from today’s post-World War II record of 78 percent of Gross Domestic Product (GDP) to 95 percent of GDP by 2029 (up from 92 percent under the previous baseline in May). If the 2017 tax cuts and other policies are extended, it would reach 101 percent by 2029.

- Annual budget deficits will exceed the trillion-dollar mark next year and rise to $1.4 trillion, or 4.5 percent of GDP, by the end of the decade.

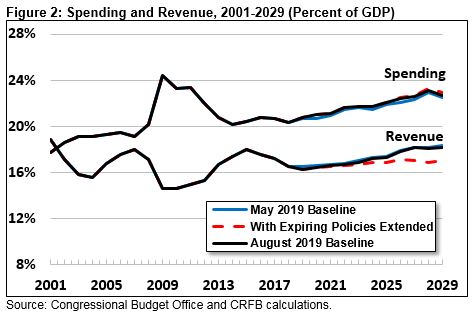

- Growing debt and deficits are driven by a disconnect between spending and revenue. Under current law, spending will grow from 20.8 percent of GDP this year to 22.7 percent of GDP by 2029, while revenue will remain roughly between 16 and 17 percent of GDP through 2025 and rise to 18.2 percent of GDP by 2029, assuming recent tax cuts expire as scheduled.

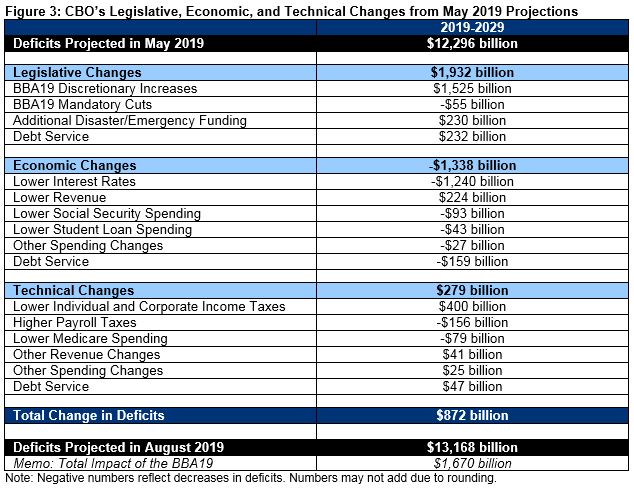

- The Bipartisan Budget Act of 2019 substantially worsened the fiscal outlook, adding $1.7 trillion to projected deficits over the decade. Other legislative changes increased deficits by an additional $260 billion. Partially offsetting this, revised forecasts for interest rates and other factors will reduce projected deficits by $1.1 trillion. In total, CBO projects deficits to be $872 billion higher than projected in May.

- CBO projects the economy to grow a bit faster than 2 percent next year, slowing to 1.7 to 1.8 percent per year thereafter. It projects interest rates to rise from their current lows but remain very low by historic standards.

CBO’s latest projections show our fiscal situation will continue to deteriorate as a result of irresponsible tax and spending policies and the growth of health, retirement, and interest spending. Lawmakers must act sooner rather than later to prevent slower wage growth, higher interest payments, reduced fiscal space, and the increased risk of a fiscal crisis that would likely result from our current path.

Deficits and Debt Are Projected to Grow

CBO projects debt will rise by more than $12.8 trillion over the next decade, from $16.5 trillion today to $29.3 trillion by 2029. As a share of GDP, debt will rise from a post-war record-high of 78 percent of GDP today – about twice the historic average – to 95 percent of GDP by 2029. Debt will continue to rise over the long term.

We estimate that debt could be significantly worse if lawmakers extend various expiring tax policies, including the individual tax cuts from the 2017 Tax Cuts and Jobs Act (TCJA) and the delay of several health taxes. Specifically, we estimate debt would grow by $14.6 trillion over the next decade, to $31.1 trillion, or 101 percent of GDP, by 2029. This suggests debt would exceed its previous record – 106 percent of GDP set immediately after World War II – around 2030.

Rising debt is the result of large and growing annual budget deficits.

Under current law, CBO projects deficits will exceed the trillion-dollar mark next year and rise from $779 billion in 2018 to $1.4 trillion by 2029. As a share of the economy, CBO projects deficits will increase from a decade low of 2.4 percent of GDP in 2015 to an average of 4.7 percent of GDP over the next decade.

These projected deficits are significantly higher than what most experts view as sustainable, but deficits would be even larger if current policies are extended. We project deficits could reach nearly $1.5 trillion by 2026 and eclipse $1.8 trillion by 2029 under CBO’s Alternative Fiscal Scenario. As a share of GDP, the deficit would reach 5.9 percent of GDP by 2029.

Spending and Revenue Will Continue to Diverge

Rising debt and deficits are driven by the disconnect between spending and revenue. Next year, CBO projects spending to total $4.6 trillion, or 21.0 percent of GDP, while revenue will total $3.6 trillion, or 16.4 percent of GDP. Over the past half-century, spending averaged 20.3 percent of GDP while revenue averaged 17.4 percent, so both will be worse than their historical averages.

Over the next decade, CBO expects spending and revenue to both grow as a share of GDP. Specifically, CBO projects spending to rise from 20.8 percent of GDP this year to 22.1 percent of GDP by 2025 and 22.7 percent by 2029. Revenue is projected to rise slowly from 16.3 percent of GDP this year to 17.3 percent of GDP by 2025; it will then rise rapidly to 18.2 percent of GDP by 2029, mainly due to the expiration of major provisions in the TCJA.

If lawmakers extend various expiring tax policies, including the individual tax cuts from the TCJA and postponement of several health-related taxes, revenue would reach only about 17 percent of GDP by 2029 and spending would rise to almost 23 percent.

While discretionary spending played a significant role in spending growth over the past few years, growth over the next decade can be explained by rising health, retirement, and interest costs. Spending in those three areas is projected to rise from 11.9 percent of GDP ($2.5 trillion) in 2019 to 15.0 percent of GDP ($4.6 trillion) in 2029 and comprise 80 percent of the $2.6 trillion increase in nominal spending and 161 percent of the growth as a share of GDP through 2029.

On the revenue side, CBO projects individual income tax receipts will rise slightly, from 8.0 percent of GDP this year to 8.6 percent of GDP by 2025, and then grow significantly to 9.6 percent of GDP by 2029 due to expiring tax cuts. Other sources of revenue will remain relatively steady as a share of the economy.

The Bipartisan Budget Act of 2019 Substantially Worsened the Budget Outlook

CBO’s budget projections have deteriorated since its previous baseline in May. Specifically, CBO projects deficits will total $13.2 trillion from 2019 through 2029 – an $872 billion increase from its previous projection of $12.3 trillion. As a result, CBO estimates debt will reach 95 percent of GDP in 2029, compared to its prior estimate of 92 percent of GDP. The entire difference can be explained by the passage of the Bipartisan Budget Act of 2019 (BBA19).

The BBA19 increased the prior law caps on discretionary spending by about $320 billion for Fiscal Years (FY) 2020 and 2021. Because negotiators chose not to extend the caps beyond 2021, however, levels for that year set the baseline for all future years. According to CBO, the net effect is a $1.5 trillion increase in projected primary spending and a $1.7 trillion increase in debt, including interest.

In addition, lawmakers enacted $24 billion of emergency funding this year for disaster relief and the southern border. This funding also carries through to projections of future spending, increasing deficits by $230 billion, or about $260 billion with interest.

Though the BBA19 substantially worsened the fiscal outlook, other factors will partially offset its impact. In particular, lower interest rate projections will reduce projected deficits by about $1.2 trillion excluding debt service, while remaining factors will worsen the outlook by about $430 billion on net.

Economic revisions in total reduce CBO’s projected deficits by $1.3 trillion through 2029. In addition to the $1.2 trillion reduction in interest costs, primary spending will be about $163 billion lower largely due to lower Social Security and student loan spending caused by lower inflation and interest rates, respectively. On the other hand, revenue will be $224 billion lower, largely due to lower expected wages and salaries reducing payroll taxes and lower Federal Reserve remittances caused by lower interest rates.

Technical revisions increase deficits by $279 billion through 2029 through lower revenue that is slightly offset by lower primary spending. Individual and corporate income taxes are a combined $400 billion lower largely due to lower-than-expected 2019 collections, a greater share of withheld taxes going to payroll taxes, and lower retirement account withdrawals. Lower income taxes are offset by $156 billion from higher payroll taxes due to the same withholding change that affected income taxes. Technical changes reduce primary spending by a net $46 billion, entirely due to lower Medicare spending from the withdrawal of the Administration’s prescription drug rebate rule. The primary spending change total includes a $34 billion increase in student loan spending from updated information on borrowers.

Economic Projections

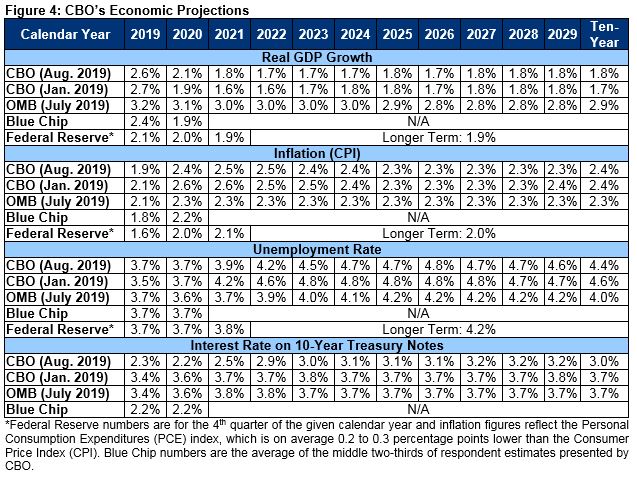

CBO’s latest baseline is built on a new set of economic projections, updated for recent economic data and the effects of the BBA19 and other legislation. The last set of economic projections was issued in January.

CBO projects economic growth to slow in 2019 and 2020 before leveling off at around 1.8 percent per year. It projects interest rates – which have fallen substantially over the past year – to rebound somewhat over the next few years but remain well below historic levels. Compared to its January projections, CBO projects similar levels of growth but lower interest rates over the entire projection window.

In 2018, real GDP grew by 2.9 percent. CBO projects further growth of 2.6 percent this calendar year, 2.1 percent in 2020, and 1.7 to 1.8 percent per year thereafter. CBO does not explicitly predict if there will be a recession or when one might occur, though its projections are meant as an average, incorporating the possibility of a recession. These projections are relatively similar to CBO’s estimates from January, though near-term projections are a bit higher in light of the stimulative effects of the BBA19.

According to CBO, the unemployment rate will hold steady at 3.7 percent in 2019 and 2020 before rising to around 4.7 percent in the years following. CBO believes the current unemployment rate is below what is permanently sustainable and that the economy is currently operating above its potential. It does not believe this will remain true over the long term.

The most significant change in CBO’s forecasts relates to interest rates. In January, CBO projected (in line with the Blue Chip Survey and others) that the rate on 10-year Treasury bonds would rise above 3 percent in 2019 and reach 3.8 percent by 2029. In reality, these Treasuries peaked at 3 percent in the fourth quarter of 2018 and are currently paying an interest rate of only 1.6 percent. CBO projects interest rates on 10-year bonds will average about 2.2 percent over the next year and rise slowly to 3.2 percent by the end of the decade. CBO previously estimated rates would rise to 3.8 percent, and over the past three decades they have averaged 4.6 percent.

In terms of inflation, CBO projects Consumer Price Index (CPI) growth of 2.3 to 2.5 percent per year over the next decade. Other chain-weighted measures of economy-wide inflation are projected to rise by about 2 percent per year, in line with the Federal Reserve’s target.

Overall, CBO’s projections are well within the consensus and very similar to projections from the Federal Reserve, Blue Chip, and other forecasters. The Administration’s forecast of nearly 3 percent sustained growth is far outside the consensus and highly unlikely based on economic evidence.

Conclusion

CBO’s latest budget projections confirm that our country remains on an unsustainable fiscal path and our trajectory has worsened. Trillion-dollar deficits are slated to become the new normal even sooner than previously projected, and debt will grow rapidly as a share of GDP.

Driving this growth is the rising costs of Social Security, health care, and interest on the debt. Yet rather than control or finance this cost growth, policymakers have worsened the fiscal outlook through large, unpaid-for tax cuts and spending increases. The recently-passed Bipartisan Budget Act of 2019 alone added $1.7 trillion to projected debt levels.

Under current law, debt will rise from a post-WWII era record-high 78 percent of GDP today to 95 percent of GDP by 2029. If various tax policies are extended, debt will exceed the size of the economy within a decade. In either case, debt will continue to rise unsustainably over the long term.

As we’ve explained before, high and rising debt slows wage growth, increases interest payments, reduces the fiscal space available to respond to recessions or other emergencies, places an undue burden on future generations, and heightens the risk of a fiscal crisis. Action must be taken sooner rather than later to avoid these consequences.

The first step toward a sustainable fiscal outlook is to stop making the situation worse. Policymakers must offset the total cost of any new legislation as well as any extensions of expiring tax cuts.

Beyond that, lawmakers must secure Social Security and other trust funds headed toward insolvency, control the growth of health care costs, increase revenue, reduce spending, and pursue a pro-growth economic agenda. Without including all of these elements, it would be incredibly difficult to fix our nation’s budgetary challenges and place the country on solid fiscal ground.