Analysis of CBO’s January 2019 Budget and Economic Outlook

The Congressional Budget Office (CBO) released its Budget and Economic Outlook today, projecting high and rising deficits and debt over the next decade and beyond.

CBO’s report shows:

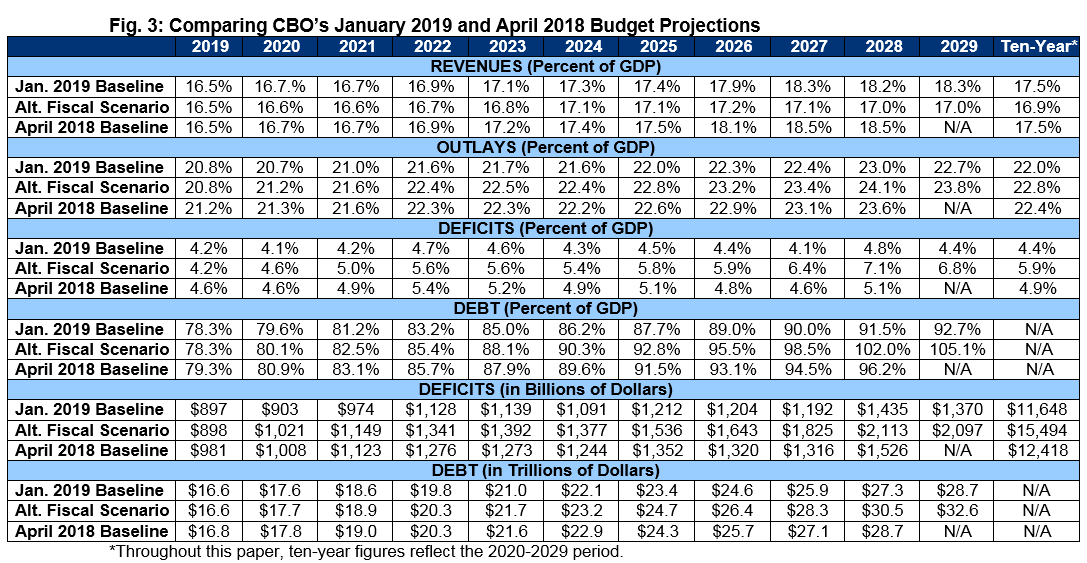

- Debt held by the public will increase by more than $12.5 trillion under current law over the next decade – from $16.1 trillion today to $28.7 trillion by 2029.

- Debt as a share of the economy will rise rapidly, from today’s post-war record of 78 percent of GDP to nearly 93 percent of GDP by 2029. Under CBO’s Alternative Fiscal Scenario (AFS), debt will reach 105 percent of GDP by 2029, approaching the all-time record set just after World War II.

- Annual budget deficits will also steadily rise under current law, eclipsing $1.1 trillion by 2022 and reaching nearly $1.4 trillion late in the decade. Under the AFS, trillion-dollar deficits will return by next year and the budget deficit will exceed $2 trillion late in the decade. Depending on the scenario, budget deficits will range between about 4.5 percent of GDP to 7 percent by 2029.

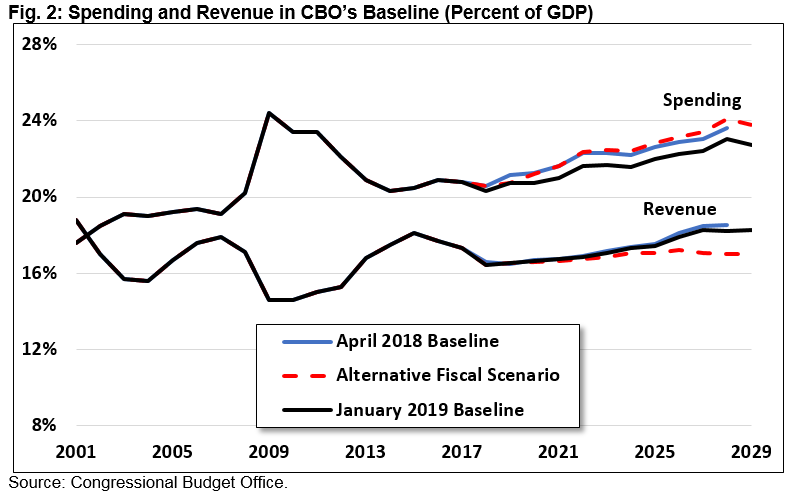

- Growing deficits and debt are the result of rising spending and depressed revenue. Under current law, spending will grow from 20.3 percent of GDP in 2018 to 22.7 percent by 2029 while revenue will remain around 17 percent of GDP through 2025 and rise to 18.3 percent by 2029, assuming many recent tax cuts expire. Under the AFS, revenue will remain at 17.0 percent of GDP in 2029 while spending rises to 23.8 percent.

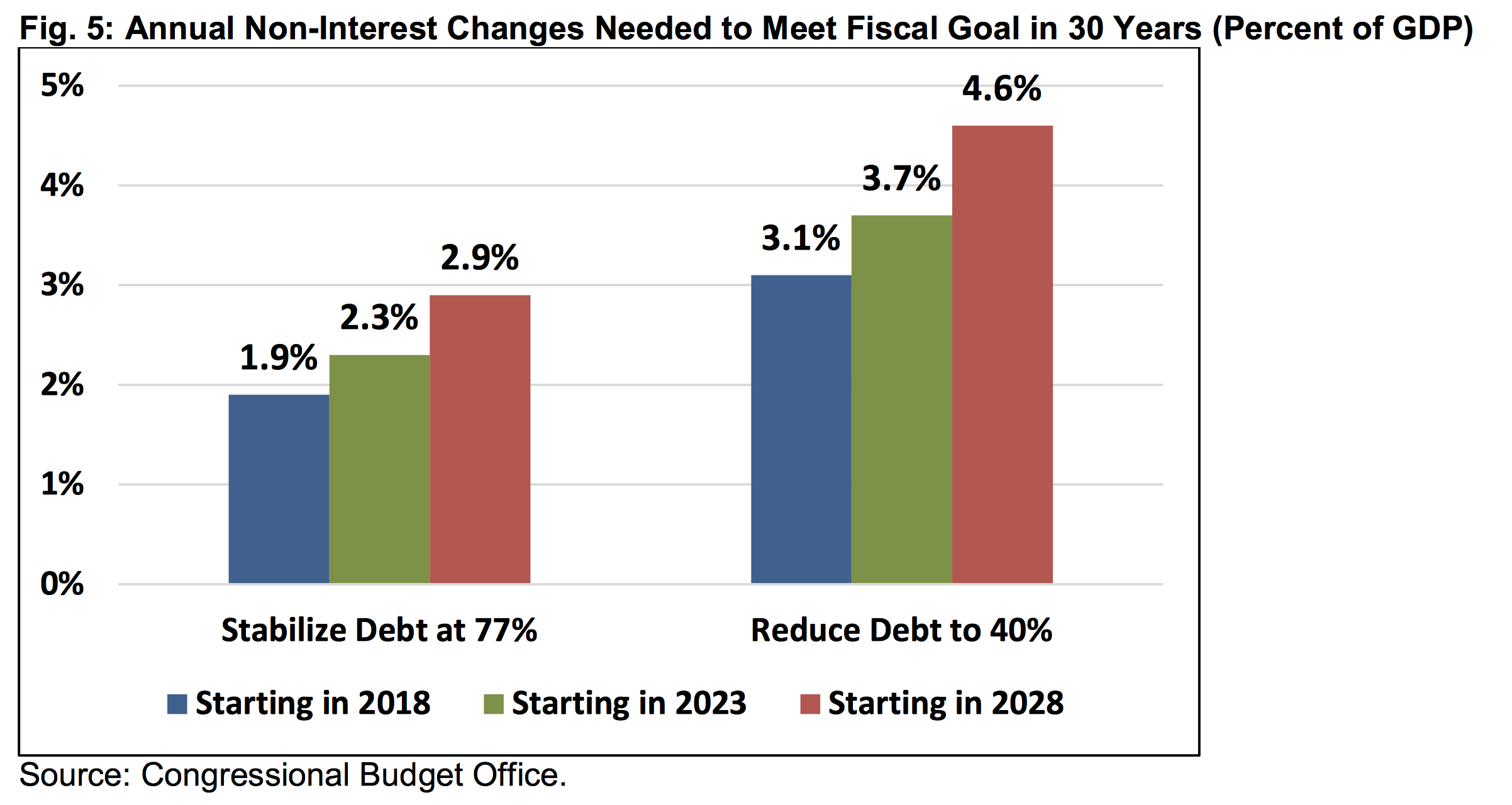

- Cumulative deficits through 2028 are projected to be $1.2 trillion lower under current law than in CBO’s last baseline from April 2018. The entire improvement can be attributed to two factors that may not ultimately materialize: lower assumed disaster spending and new tariffs imposed by the Administration.

- CBO continues to project strong economic growth for 2019, but real annual growth will fall below 2 percent for most of the decade.

CBO’s latest projections show that the fiscal situation will continue to deteriorate as a result of irresponsible tax and spending legislation and the growth of health, retirement, and interest spending. Lawmakers must act sooner rather than later to prevent the slower wage growth, higher interest payments, reduced fiscal space, and increased risk of fiscal crisis that would likely occur on our current path.

Deficits and Debt

CBO projects debt will rise by more than $12.5 trillion over the next decade, from $16.1 trillion today to $28.7 trillion by 2029. As a share of GDP, debt will rise from a post-war record-high of 78 percent of GDP today – about twice the historic average – to 93 percent of GDP by 2029. CBO projects debt will reach record levels by 2035 and eclipse 150 percent of GDP in three decades.

Under CBO’s Alternative Fiscal Scenario (AFS), which offers a more realistic forecast of our current trajectory by assuming various expiring tax and spending provisions will continue, the situation would be far worse. Specifically, debt will grow by $16.5 trillion over the next decade, to $32.6 trillion, or 105 percent of GDP, by 2029. This suggests debt will exceed the highest share in our nation’s history, set immediately after World War II, in 2030.

Rising debt is the result of large and growing annual budget deficits.

Under current law, CBO projects deficits will grow from $779 billion last year to $897 billion in 2019, $1.1 trillion in 2022, and $1.4 trillion by 2029. As a share of the economy, CBO projects deficits will increase from a prior-decade low of 2.4 percent of GDP back in 2015 to an average of 4.4 percent over the next decade.

These projected deficits are significantly higher than what most experts view as sustainable, but sadly deficits would be even higher if current policies are continued. Under CBO’s AFS, trillion-dollar deficits will return next year and the deficit will exceed $2 trillion by 2028. As a share of GDP, the deficit would reach 6.8 percent of GDP by 2029 under the AFS – higher than any time in history outside of World War II or the Great Recession.

Spending and Revenue

Rising deficits are driven by the disconnect between spending and revenue. Spending in 2019 will total $4.4 trillion (20.8 percent of GDP), while revenue will total only $3.5 trillion (16.5 percent of GDP). In the coming years, CBO projects spending to rise rapidly while revenue remains low (particularly through 2025).

Specifically, CBO projects spending to rise from 20.3 percent of GDP last year to 22.0 percent by 2025 and 22.7 percent by 2029. Revenue, meanwhile, is projected to remain between 16.5 and 17.4 percent of GDP through 2025, rising to 18.3 percent by 2029 as a result of the expiration of individual provisions from the Tax Cuts and Jobs Act.

Under the Alternative Fiscal Scenario – which assumes various tax and spending provisions continue – revenues will only reach 17.0 percent of GDP by 2029, while spending will total 23.8 percent of GDP.

Whereas spending growth between 2017 and 2019 was largely a result of the discretionary spending increase from the Bipartisan Budget Act of 2018, future spending growth is driven mainly by rising health, retirement, and interest costs. Spending for Social Security, Medicare, and net interest are projected to account for 75 percent of the $2.6 trillion increase in nominal outlays between 2019 and 2029.

As a share of the economy, CBO projects Social Security will grow from 4.9 percent of GDP in 2019 to 6.0 percent by 2029, federal health spending will grow from 5.2 percent in 2019 to 6.8 percent by 2029, and interest will rise from 1.8 percent of GDP in 2019 to 3.0 in 2029. Meanwhile, discretionary spending will shrink from 6.3 percent of GDP in 2019 to 4.9 percent by 2029, and other spending will shrink from 2.6 percent to 2.2 percent of GDP.

On the revenue side, CBO projects individual income tax receipts will rise slightly from 8.3 percent of GDP in 2019 to 8.6 in 2025 and then grow significantly to 9.6 percent by 2029 as a result of expiring tax cuts. Corporate income tax revenue will rise from 1.2 percent of GDP in 2019 to 1.6 percent in 2025 and then shrink to 1.4 percent by 2029.

CBO projects payroll taxes, excise taxes, and other sources of revenue will remain relatively steady as a share of GDP through 2029.

Over the next decade, CBO projects revenue to average 17.5 percent of GDP under current law and 16.9 percent under the AFS, compared to a 50-year historic average of 17.4 percent. CBO projects spending to average 22.0 percent of GDP under current law and 22.7 percent under the AFS, compared to a 20.3 percent historic average.

Changes in the Budget Outlook

CBO’s budget projections have improved modestly since its last baseline in April 2018, though these improvements may prove illusory. In total, CBO projects deficits through 2028 will be roughly $1.2 trillion lower than previously projected.

The entirety of this improvement can be explained by two factors – almost two-thirds is the result of reductions in assumed disaster spending (and related interest savings), while the remaining third is the result of tariffs imposed by the Administration last year. It is possible that a large share of these reductions will ultimately not materialize.

Under CBO’s baseline conventions, discretionary disaster spending is assumed to continue at current levels (plus inflation). That convention resulted in artificially high disaster spending assumptions after last year’s $108 billion for disaster relief but artificially low assumptions based on the $2 billion that has been appropriated so far this year (more will likely be enacted soon). Over the next decade, actual disaster spending is likely to be somewhere between the two.

Tariff revenue may fall if this or a future Administration negotiates additional trade deals or reverses recent tariffs through executive authority. However, tariff revenue could rise if the President follows through with increasing certain tariffs from 10 percent up to 25 percent.

Outside of these factors, changes in economic assumptions reduced projected deficits by $336 billion (mainly due to reduced interest costs), while changes in technical assumptions (other than tariffs) increased projected deficits by a similar amount (due to lower revenue projections).

Economic Projections

In addition to budget projections, CBO’s baseline incorporates new economic projections. While CBO does not try to predict recessions or forecast the business cycle, its projections anticipate that growth will slow toward a long-term trend of below 2 percent per year.

CBO estimates that real GDP grew by about 2.9 percent last year and will grow 2.7 percent this year, in part because of the stimulative effects of recent tax cuts and spending increases. However, CBO projects growth will slow to 1.9 percent next year and will average 1.7 percent in the subsequent nine years. Overall, CBO’s projections are well within the consensus and very similar to projections from the Federal Reserve, Blue Chip, and other forecasters. The Administration’s forecast of nearly 3 percent sustained growth beyond the next year or so are far outside the consensus and highly unlikely based on economic evidence.

Under CBO’s projections, the unemployment rate will decrease from 3.9 percent in 2018 to 3.5 percent in 2019 before rising to 3.7 percent in 2020 and the years following, ultimately reaching 4.7 percent by 2029. CBO estimates that actual employment has been above full potential employment since early 2018, reflecting higher demand for labor due to the recent economic boost.

Meanwhile, CBO projects interest rates on ten-year bonds will rise from 2.9 percent last year to between 3.7 and 3.8 percent in 2021 and beyond. CBO projects inflation, as measured by CPI, will rise to 2.6 percent in 2020, falling to between 2.3 and 2.4 percent later in the decade.

Conclusion

CBO’s latest budget projections confirm our country remains on an unsustainable fiscal path. Even under current law, trillion-dollar deficits will become the new normal, and debt will grow indefinitely as a share of the economy.

If lawmakers continue recent tax cuts and spending increases without offsets, the fiscal situation would be even more dire. Under CBO’s Alternative Fiscal Scenario, the deficit will eclipse the trillion-dollar mark next year and the two-trillion-dollar mark by 2028. Under that scenario, debt as a share of GDP would likely exceed its prior record – set just after World War II – by 2030.

As CBO explains, high and rising debt will slow wage growth, raise interest payments, reduce fiscal space, and increase the risk of an eventual fiscal crisis. Action must be taken to avoid these consequences.

The first step to prevent these outcomes is to stop making the fiscal situation worse. Policymakers must offset the cost of any new initiatives as well as any extensions of expiring tax cuts and any increase in statutory spending caps.

Beyond that, lawmakers must secure Social Security and other trust funds headed toward insolvency, control the growth of health care costs, increase revenue, reduce spending, and pursue a pro-growth economic agenda. Without ultimately including all of these elements, it would be incredibly difficult to truly fix our nation’s budgetary challenges and put the country on sound fiscal footing.

Update 1/29/19: The Alternative Fiscal Scenario numbers were corrected after publication to exclude a timing shift adjustment and allow an apples-to-apples comparison with current law.