The More the Budget Changes, the More Things Stay the Same

With FY 2014 officially in the book, it’s time to look back at how spending and revenues have changed since the FY 2009’s highest nominal deficit of all time (and 5th highest as a percentage of GDP since 1930).

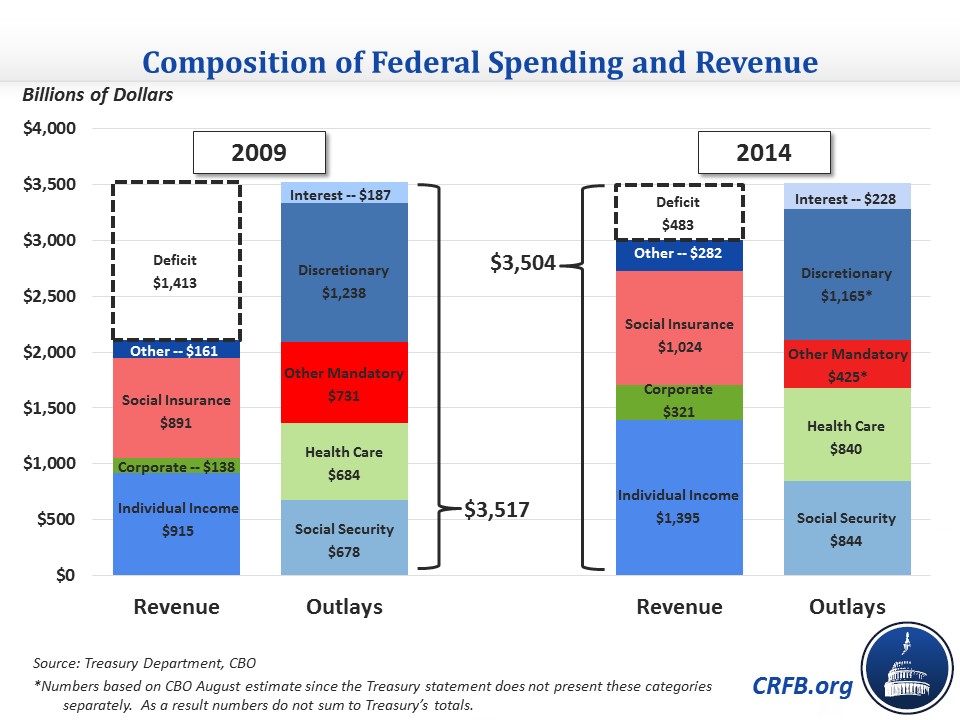

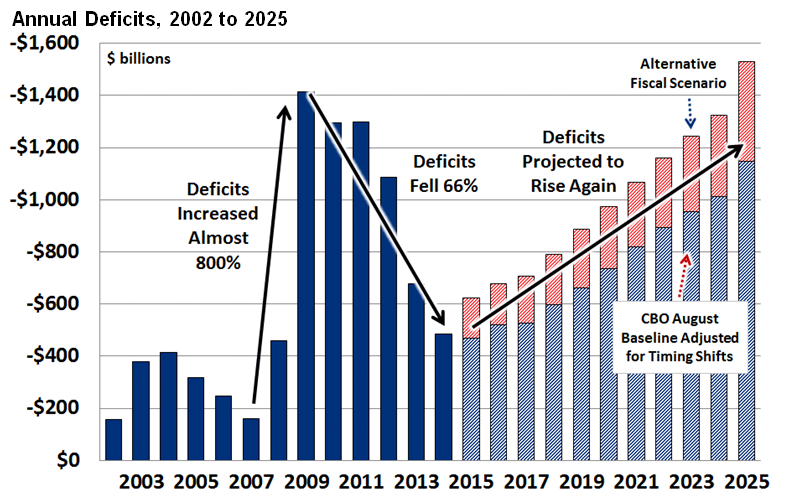

The FY2014 budget deficit totaled $483 billion with $3.02 trillion of revenue and $3.50 trillion of spending. This deficit was nearly 30 percent below the FY2013 deficit and 66 percent below its 2009 peak. In FY 2009, the budget deficit was $1.41 trillion with $2.11 trillion in revenue and $3.52 trillion of spending.

Annual deficits have fallen substantially over the past five years, largely due to rapid increases in revenue (mostly from the economic recovery), the reversal of one-time spending during the financial crisis, small decreases in defense spending, and slow growth in other areas. This temporary improvement in our nation's short-term finances, while likely too quick for the struggling economy, comes as nominal spending is only about $15 billion lower (though it has declined sizably as a percent of GDP).

Between that time, health care and Social Security spending have grown significantly due to natural upward pressure, aging of the population, and to a lesser extent, the coverage expansions in the Affordable Care Act. Interest spending is also higher as a result of the huge increase in debt since 2009. Meanwhile, discretionary and other mandatory spending are down from fading stimulus, the economic recovery, and legislated deficit reduction like the sequester.

This deficit reduction was drastically helped by the 44 percent (roughly $900 billion) increase in tax collections, primarily a result of the economic recovery, which restored revenues as a share of GDP from their depressed 2009 levels to about their historical average. New taxes from the American Taxpayer Relief Act and the Affordable Care Act have also played a role in the recovery of individual income tax revenue. Corporate income receipts more than doubled thanks to the recovery of corporate profits and the (likely temporary) expiration of the tax extenders. Remittances from the Federal Reserve and excise taxes have also bolstered federal revenue.

As we discussed both last week and this week, the problem with the nation's finances is not over. It is clear that health care and Social Security spending, the drivers of long-term debt, are continuing to rise and will continue to do so. The lower projected deficits of the next few years are not a sign that the mission is accomplished. Lawmakers will have to go further in order to truly put the federal debt on a sustainable path.

{kind=link}