Millennials to Receive $2 Million in Social Security & Medicare Benefits

The Urban Institute published a new report showing that younger generations will receive much more in lifetime Social Security and Medicare benefits than today's retirees, and all generations will receive more benefits than they have paid in taxes, leading to ballooning economic shortfalls in the two programs.

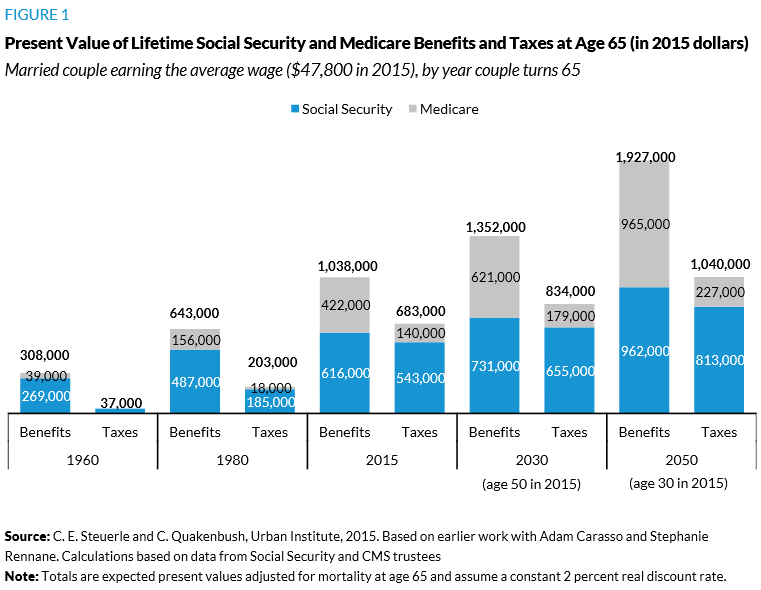

The study, by CRFB board member Eugene Steuerle and Caleb Quakenbush, shows that benefits for an average-earning couple retiring today are valued at $1 million and expected to be $2 million for millennials turning 30 this year. Left unchanged, this trend will continue to rise for future generations.

The expected growth in benefits is due to rising life expectancy (which means people spend more years in retirement but the same amount of time working), rising health care costs, and the fact that Social Security benefits are wage-indexed so that benefits will grow in inflation-adjusted terms. These numbers reflect the troubling finances of both Social Security and Medicare, with Social Security on a path to insolvency within 20 years and Medicare being financed less and less by payroll taxes.

In a related blog, Steuerle points out that this increase is “hardly sustainable,” noting that these programs account for a large proportion of government spending growth over the long term. Also, these programs, along with other health care programs and tax expenditures, are on autopilot as a result of legislators’ past decisions. Spending for children, defense, infrastructure, and basic government functions, however, is scheduled to remain flat or in many cases decline as a share of the economy over time.

The projected growth in Social Security benefits is one reason that many proposals to establish solvency in Social Security would slow the growth of future benefits, at least for higher-earners, so millennials would receive more than retirees today, but not as much. Experiment with our Social Security Reformer to see how you would correct the imbalance in Social Security's funding.