IRA Energy Provisions Cost Could Double With New Emissions Rule

Last April, the Environmental Protection Agency (EPA) proposed a new rule for stricter vehicle emissions standards starting in model year (MY) 2027. If finalized, this rule would increase federal deficits both by increasing the number of electric vehicle tax credits awarded and reducing the collection of gas tax revenue. Based on information from the Congressional Budget Office’s (CBO’s) latest Budget and Economic Outlook and other sources, we find:

- The new emission rule will cost about $280 billion through 2033, including $200 billion through 2031, if finalized in its current form.

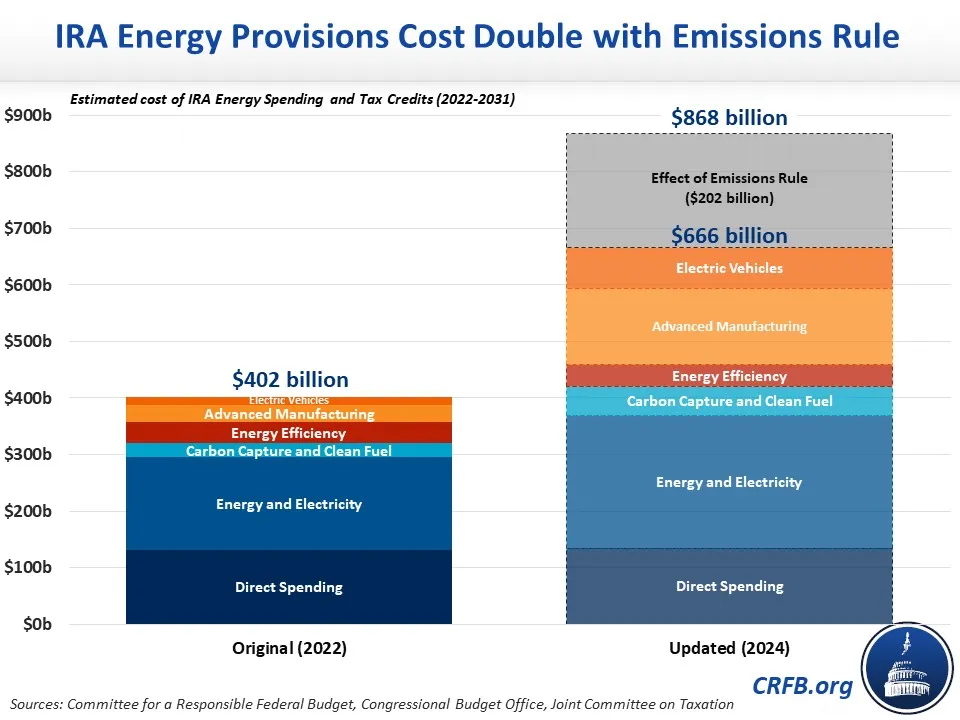

- With the emission rule in place, energy-related provisions from the Inflation Reduction Act (IRA) will cost almost $870 billion through 2031, more than double the original $400 billion estimate.

- Of the total increase, about two-fifths would be the result of the emission rule and the rest is due to a mixture of laxer-than-expected regulations on new credits, higher-than-expected demand for green technologies, and other economic and technical changes.

The EPA’s proposed rule aims to drop the average target for new light-duty vehicle (car) emissions from 186 grams of carbon dioxide per mile under the existing MY 2026 standards to 82 grams per mile by 2032 and drop the target for medium-duty vehicles (primarily large pickups and vans) from 491 to 275 grams per mile. The rule would be phased in beginning in MY 2027 and would also include changes to other pollutant standards, batteries, and general certification and testing provisions. The likely result would be a significant shift away from gas-powered vehicles and toward electric or hybrid vehicles.

At the time of passage, CBO and the Joint Committee on Taxation (JCT) estimated the IRA’s energy and climate spending and tax breaks would cost about $400 billion through Fiscal Year (FY) 2031 and would be more than fully offset by other parts of the law.

Since then, the combination of higher inflation, greater demand for credits, and looser-than-expected regulations significantly boosted the cost of those credits. Last June, we estimated the cost of the IRA energy provisions had grown by two-thirds, to $660 billion through 2031. Assuming the new vehicle emissions rule proposed by the EPA is finalized, we now estimate the cost of the provisions will more than double to $870 billion through 2031, or $1.1 trillion through 2033.

Relative to the original score, CBO’s latest baseline included a $206 billion upward revision through 2031 to the cost of energy-related tax provisions other than for electric vehicles. This increase is mostly due to greater expected investment in battery manufacturing and wind and solar energy, and it is similar to our prior estimates, based on various JCT and CBO scores, of a $198 billion revision.

CBO’s latest baseline also revised the original costs for “clean vehicle tax credits and gasoline excise taxes” upward by about $159 billion through 2031, from only $14 billion in the original score to $173 billion in their latest baseline. This revision is over $100 billion higher than in prior estimates, suggesting the remaining increase is due mainly to the new emissions rule. Because CBO applies a 50-percent weight to the effects of the proposed rule, we believe the rule itself would cost about $200 billion through 2031 once in effect.

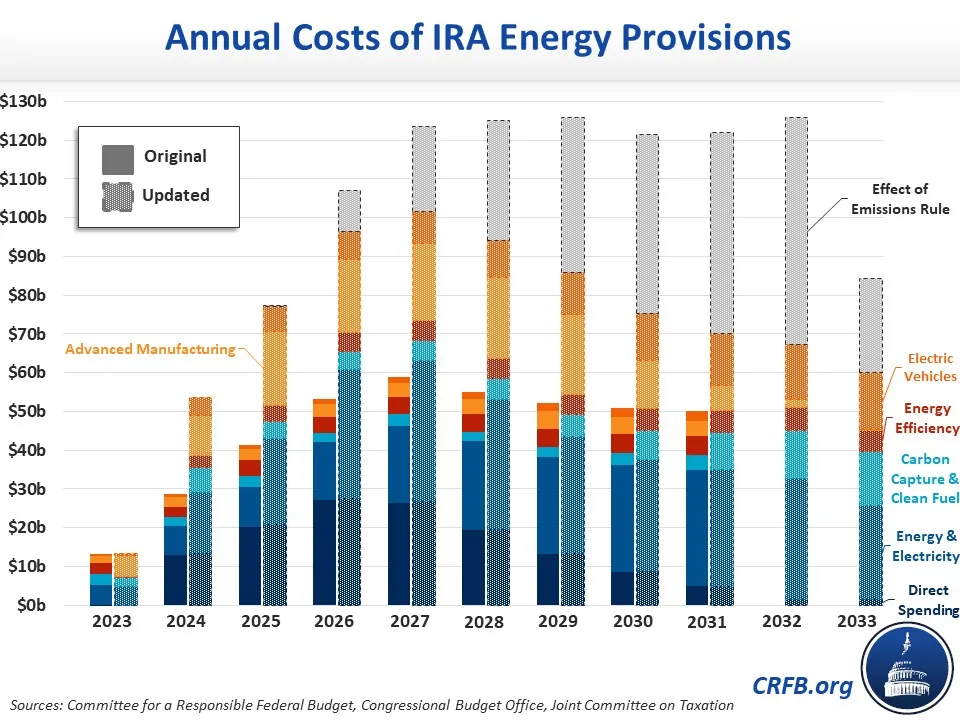

Through 2033, CBO’s new numbers suggest that the IRA energy provisions will cost about $1.1 trillion if the EPA’s emissions rule is finalized, or closer to $800 billion if the rule is abandoned or reversed. If the rule is finalized, the cost of IRA energy provisions would peak in 2032 at about $125 billion (half that without the emissions rule), before starting to fall as the tax credits expire.

Importantly, these estimates do not provide enough information to “re-score” the Inflation Reduction Act itself, which also includes various policies to raise revenue and reduce prescription drug costs. Such a re-score would require determining which new costs should be attributed to the IRA rather than to subsequent regulations and would also require re-estimating revenue and savings from other provisions, which have likely risen in light of higher nominal output and other factors.

Nonetheless, the IRA tax credits themselves are expected to cost substantially more than originally believed, suggesting ample room to pare them back.

As a starting point, the Administration could abide by Administrative PAYGO as required under the Fiscal Responsibility Act. This rule would require putting forward additional regulations to offset the cost of emissions rules, revisiting the structure of those emissions rules, or some combination of the two.

Lawmakers could also consider sunsetting some of the credits earlier than intended, in light of their stronger effectiveness, or putting in place caps, targets, and triggers to keep costs down. Such mechanisms already existed for the electric vehicle tax credits prior to the IRA and will apply to the new clean electricity production tax credit starting in 2032 under current law.

Policymakers could also enact more incremental reforms. For example, they could reverse the Treasury Department’s loose interpretations of the clean vehicle tax credit rules or close various loopholes, such as the one counting leased electric vehicles as commercial rather than personal vehicles to qualify for a bigger tax credit.

Lastly, they could work to identify new revenue sources to replace the declining gas tax or finance the cost of expanding tax credits. Lawmakers could also consider enacting a carbon tax, which could reduce carbon emissions and budget deficits at the same time.