Interest Rates Remain Near Record Highs

Interest rates continue to surge, hitting new post-financial crisis records. Over the past month, yields on the ten-year Treasury note have risen more than 50 basis points, to 4.8 percent, a 16-year high. This is well above the 4.3 percent yield we observed in August. Meanwhile, 20-year Treasuries are paying a 5.1 percent yield and three-month Treasury bills are paying 5.6 percent.

With interest rates on new debt now well above the expected growth rate (R>G), this could spell trouble for long-term debt sustainability (see a helpful twitter thread explaining the relationship between R, G, and debt here).

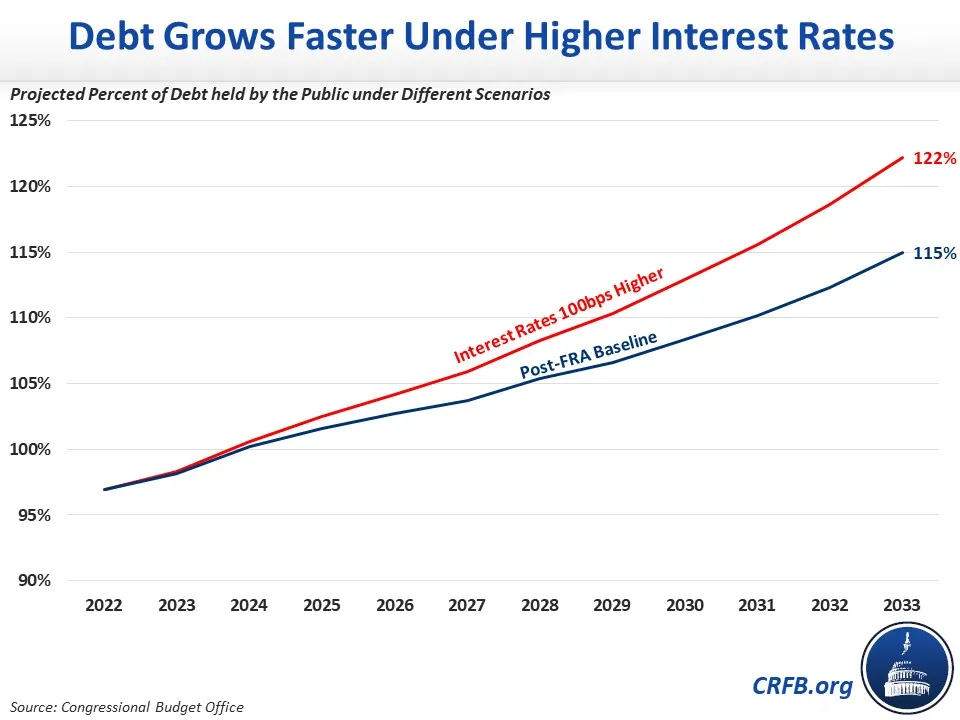

Interest rates are also well above those assumed in the Congressional Budget Office's (CBO) February baseline projections. For this quarter, CBO's baseline assumed a ten-year yield of 3.9 percent (currently 4.8 percent) and three-month yields of 4.2 percent (currently 5.6 percent).1

On average, current rates are about one percentage point above those assumed in CBO’s baseline. If that gap were to continue for the next decade, debt would grow an additional $2.8 trillion (about 7.2 percent of Gross Domestic Product) through 2033. In 2033 alone, deficits would be nearly $500 billion (1.2 percent of GDP) higher than projected.

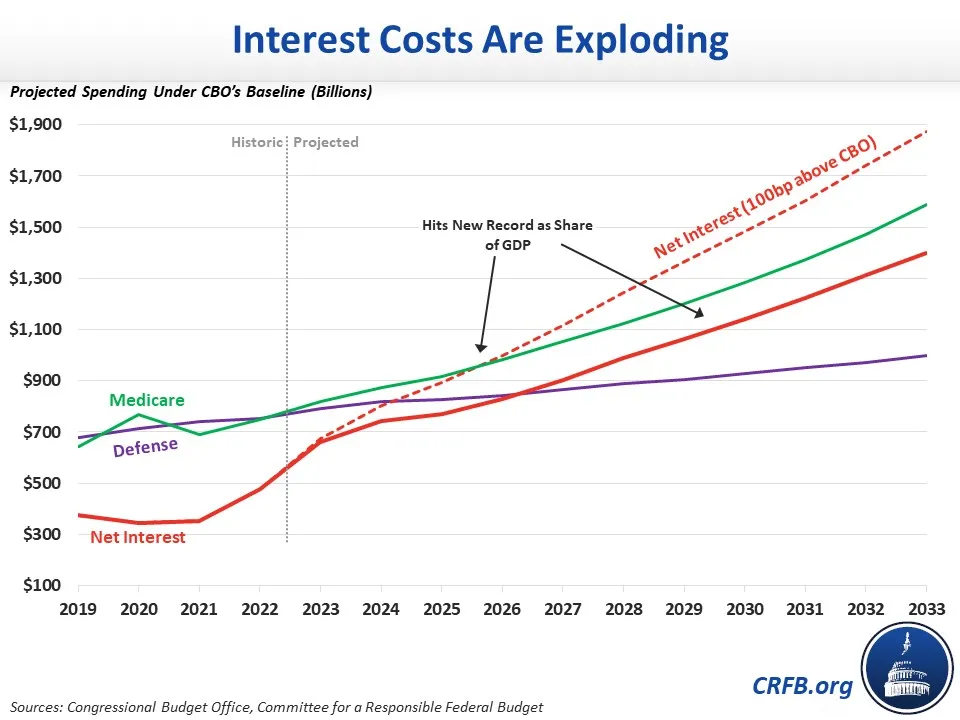

Interest was already the fastest growing part of the budget. Assuming these higher rates, interest costs would exceed defense spending by 2025 and exceed the net cost of Medicare by 2026. Under this scenario, interest would reach a record share of the economy within three years, at which point it would become the second largest federal program.

These additional interest costs also spell trouble for long-term debt sustainability, and could create the risk of a debt spiral.

Most long-term forecasts suggest nominal GDP is likely to grow by 3.5 to 4.0 percent per year over the long term. This is well below the interest rate on new bonds, which means existing debt may grow faster than the economy can keep up with.

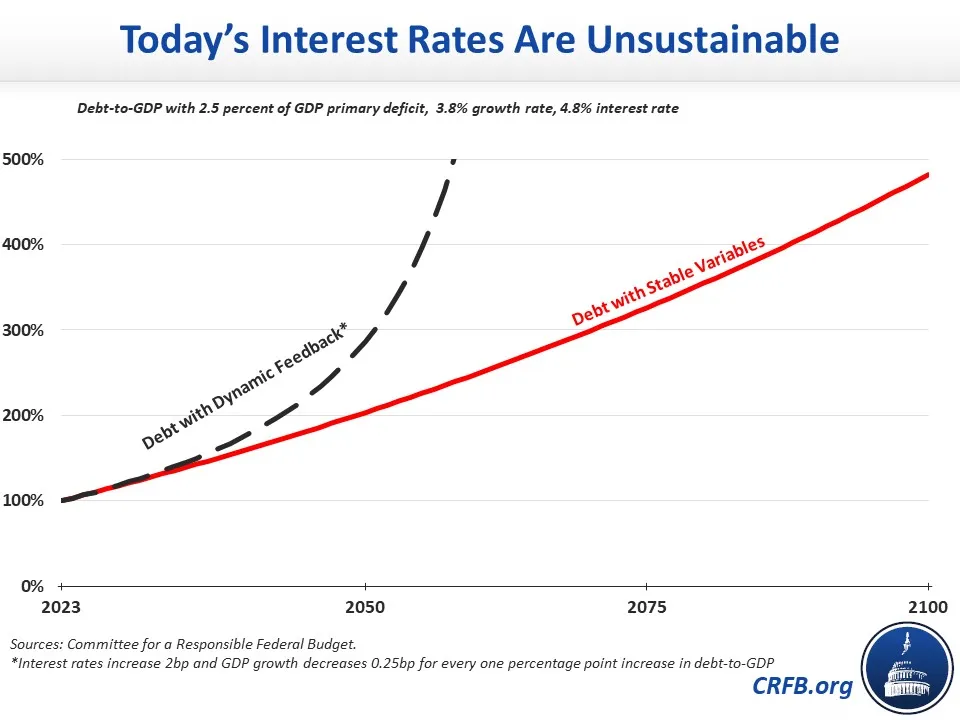

As an illustrative example, stable primary deficits of 2.5 percent of GDP would drive debt above 400 percent of the economy by the 2080s, assuming interest rates are 100 basis points above the growth rate. If high debt further pushes up interest rates and stifles growth, as economists expect, debt could spin out of control in the 2050s, breaching 500 percent of GDP.

Although most of our national debt was issued when interest rates were low, that debt is quickly rolling over into a high-rate debt environment, and further borrowing continues. Without corrective action, interest costs could total more than $13 trillion over the next decade and $1.9 trillion per year by 2033.

Rising interest costs pose a growing danger and are increasingly difficult to ignore. To mitigate these costs, lawmakers should enact thoughtful and responsible fiscal reforms that limit additional borrowing, reduce inflationary pressures, push down interest rates, and support stronger economic growth. A fiscal commission can help them to design and reach agreement on such a plan.

1 Note that CBO has since updated its near-term economic forecasts but it has not yet applied these economic changes to its budget projections.