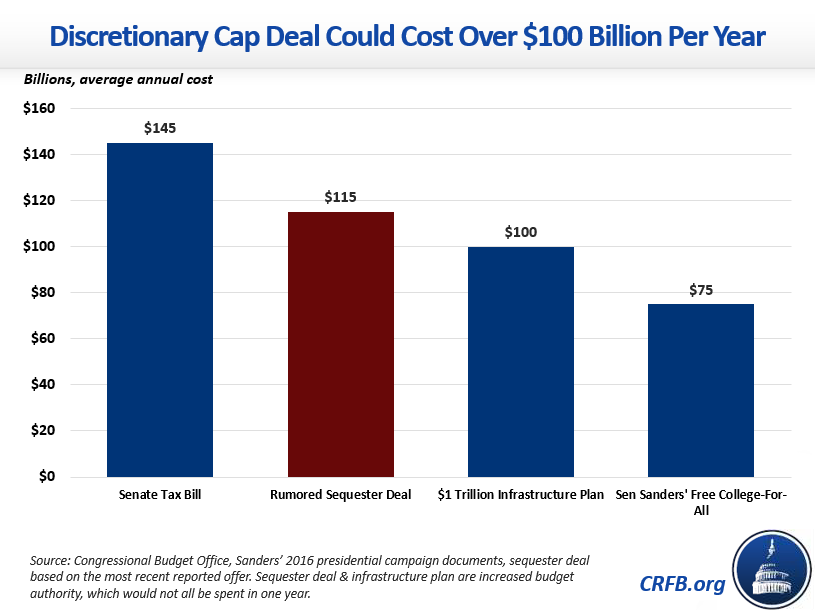

Discretionary Cap Deal Could Cost Over $100 Billion Per Year

Lawmakers are reportedly considering a year-end deal to repeal the sequester and increase discretionary spending potentially as much as $230 billion over the next two years. The sequester replacement deal in 2013 was fully offset, and any new deal should do likewise with new revenue or reductions in mandatory spending to avoid adding to the debt and to establish a strong precedent for future Congresses.

Although the sequester deal being negotiated would only affect the next two years, it sets a standard for future budget legislation. If this agreement is the first to abandon the concept of fiscally-responsible sequester replacement, it will be that much easier for future Congresses to do so.

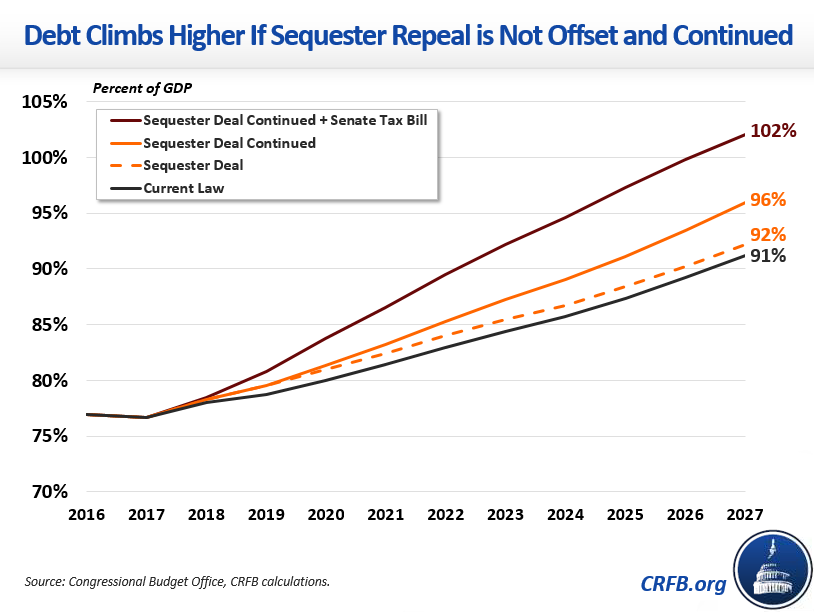

A sequester deal of $230 billion over two years would increase spending by $115 billion each year. If it's not offset, the deficit increase of the sequester deal would be 80 percent of the deficit increase of the tax bill. Over 10 years, the House and Senate tax bills cost $1.4 trillion, while continuing this discretionary spending increase would cost almost $1.2 trillion. Continuing the sequester relief deal without offsets would cause debt will rise from 77 percent of Gross Domestic Product (GDP) today to 96 percent by 2027 (as opposed to 91 percent under current law).

And if lawmakers repeal the sequester and pass the tax bill, debt would increase to 102 percent of GDP. It could rise even higher if lawmakers do not offset any other potential legislation in December, such as reconstruction spending in response to this fall's hurricanes and other disasters.

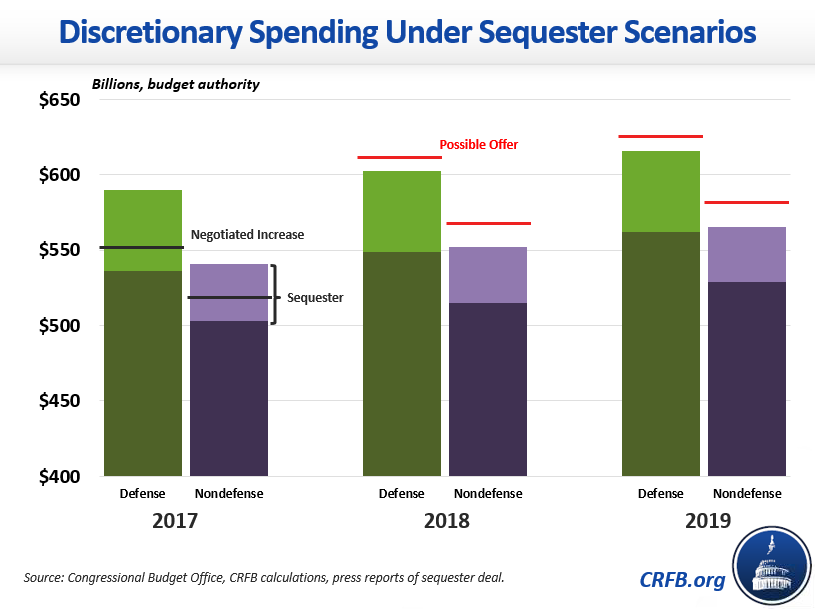

The "sequester" refers to reductions in caps on defense and non-defense discretionary spending, scheduled after a 2011 debt committee failed to come to an agreement on deficit reduction. As a result, the sequester reduced future defense and non-defense spending by equal amounts, although some of it also fell on mandatory programs. As a result, the defense sequester is slightly larger than the one for non-defense discretionary spending.

The sequester is responsible for a $54 billion decrease in the defense budget and a $37 billion decrease in the non-defense budget for next year from what would have otherwise been provided. If the sequester is allowed to take effect, both defense and non-defense spending would fall slightly from this year to next year: defense spending would decrease from $551 billion this year to $549 billion next year while non-defense spending would drop from $519 billion to $515 billion.

On the other hand, if the sequester were fully repealed, defense spending would increase to $603 billion (a 9 percent increase from current levels), while nondefense spending would increase to $553 billion (a 7 percent increase from current levels). None of these figures include war spending (called "Overseas Contingency Operations"), which is not constrained by the spending caps.

The exact size of the year-end spending deal is still being negotiated, but press reports suggest the offers started at a full repeal of the sequester and increased higher with each counteroffer, putting both defense and non-defense spending above pre-sequester levels.

Although Congress has never let the sequester fully go into effect for discretionary spending, this sequester deal could set a troubling precedent if it is unpaid for. In contrast, a 2013 deal that partially replaced the sequester was fully paid for, while a 2015 deal was at least fully paid for on paper, even if it relied on gimmicks.

If this increase above sequester limits was permanently continued without offsets, debt would rise to 96 percent of GDP by 2027 (as opposed to 91 percent under current law). And if lawmakers also pass the tax bill under consideration without reducing its cost, debt would exceed the size of the economy by 2027.

With discretionary spending scheduled to decline to historic lows as a share of GDP, there is a case for increasing it. Lawmakers should not add to the debt to do so, however. There are plenty of mandatory spending or revenue options available. As one example, our Mini-Bargain To Improve the Budget proposes adopting a more accurate measure of inflation government-wide to offset the cost of permanent (rather than two-year) sequester relief. It also offers $400 billion of other potential offsets – everything from Medicare reforms to federal retirement changes to user fees.

What's Next

-

Image

-

Image

-

Image