Deficits are a First-Order Problem

Yesterday, Former Treasury Secretary and director of the National Economic Council Larry Summers argued that “budget deficits are now a second-order problem” and the focus should instead be on economic growth. Although the piece is in many ways insightful, it could perpetuate the myth in Washington that our debt problems are either solved or are no longer a pressing concern. In addition, Summers’ piece suggests that deficit reduction and “growth strategies” are in conflict – when in fact they are complements. Below, we respond to a number of the arguments in the FT piece.

Our Debt Problems are Far From Solved

In his piece, Summers argues that deficits need not be a major concern given that they will fall to 2 percent of GDP by 2015. While it is true that deficits are falling and debt is projected to decline from 72.5 percent of GDP now to 69.5 percent by 2018, this decline is only temporary. After 2018, debt levels will again begin to rise – reaching the size of the economy by 2035 under CRFB's Realistic Baseline, and doubling it by the 2060s. Although these levels have fallen significantly as a result of the deficit reduction enacted over the past few years, they are nonetheless unsustainable.

Even if this unsustainable growth in debt levels were stopped, moreover, more would need to be done to reduce the debt from its extraordinarily high levels. Debt as a share of GDP is currently twice its historic average and highest they have ever been since the aftermath of World War II. Once the economy recovers, these high levels of debt are likely to “crowd out” investment and growth; and are certain to reduce our fiscal flexibility. It is not clear that, under these levels of debt, the United States would have the capacity to appropriately respond to another recession, a war, or another large-scale national emergency.

Our debt problems remain far from solved, by our estimates, and an additional $2.2 trillion in deficit reduction to put debt on a downward path as a share of the economy this decade alone.

Uncertainty is Not So Uncertain

In his piece, Summers argues that even if debt levels are projected to rise, those projections could be off as they are well within a margin of error. Yet while CBO’s estimates are certainly imperfect, there is little reason to think they are directionally wrong. While economic variables and health care costs are particularly hard to project, demographics are destiny. Over the next quarter century, 19 percent of the projected increase in entitlement spending is due to increased spending from the health law and 54 percent from population aging, which have long been baked in the cake. We've known about the retirement of baby boom generation for years now so forecasters can make better informed projections about demographics than they can about health care costs or economic growth.

Moreover, uncertainty is a double-edged sword. The fiscal situation could be far worse than projected as easily as it could be far better. And considering our high levels of debt and risk of unattainability, it would be prudent to lock in a sustainable path now and relax enacted policies later if projections are too pessimistic. This is especially true given that most of the necessary entitlement changes will have to phase in slowly, meaning they will need to start soon to have a significant impact when they are needed most.

Growth is Not Enough

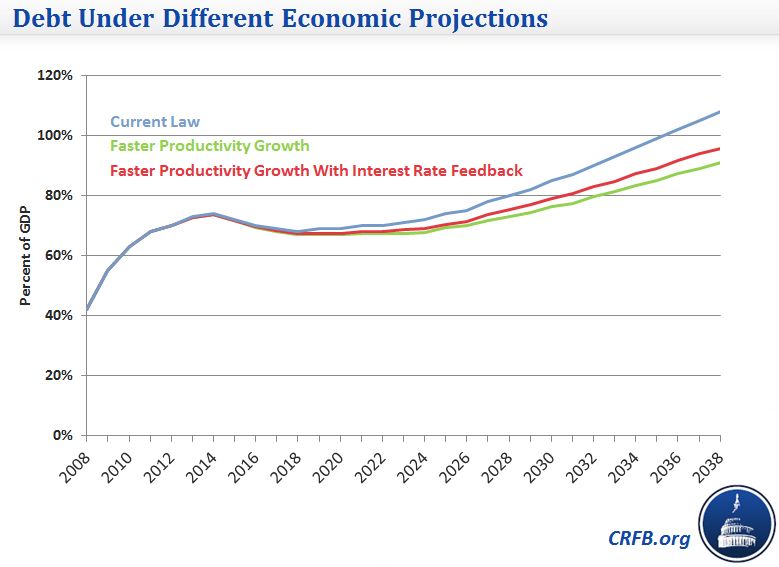

One common myth surrounding the nation's debt problem is we can grow our way out of the problem. Summers, in fact, suggests that an increase of just 0.2 percent in annual growth would be enough to close the gap. Although we do not have access to Dr. Summers’ calculations, our math suggests that 0.2 percent faster growth would be far from sufficient. While it is true that economic growth would increase revenues, it would also increase spending in a number of areas such as Social Security and thus reduce the budgetary improvement. In CBO's Long-Term Outlook, a 0.5 percentage point increase in productivity growth still resulted in debt levels that debt would still be between 65 and 77 percent of GDP in 2038, and on an upward path. We used these results to roughly approximate the effect of a 0.2 percentage point increase in productivity growth, under current law, and found that debt levels would remain on a clear upward track – reaching between 89 and 94 percent of GDP by 2038. Or in other words, growth certainly helps but will not solve the problem alone.

Long-Term Deficit Reduction is a Growth Strategy

In his piece, Summers rightfully calls for pursuing “growth strategies.” Yet long-term deficit reduction is a growth strategy, and is an important complement to many other growth strategies. Because lower debt levels reduce “crowd out,” of investment, deficit reduction on its own is likely to promote growth. CBO's recent Long-Term Budget Outlook found that a $2 trillion illustrative plan would increase real GNP by 0.8 percent by 2023 and 4 percent by 2038.

In addition to this direct impact, a comprehensive plan to reduce the debt may be the best avenue for pursuing a number of other growth strategies. For example, most plan to reduce impact of sequestration – which is currently reduced GDP by 0.6 percent in the fourth quarter of 2013 alone – would rightly do so by offsetting the cost through future deficit reduction. In addition, a comprehensive debt deal offers one of the best opportunities to pursue individual and corporate tax reform, which could increase the size of the economy significantly by offering lower rates and a broader base to better encourage work and investment while reducing various distortions. On the spending side, policies which reprioritize public investment over consumption and encourage work and investment can also promote growth. And finally, just the announcement of a comprehensive plan could have some positive growth impact by offering households and businesses increased certainty, stability, and confidence in the nation's economy.

At the end of the day, deficit reduction remains a first-order concern exactly because it is the key to economic growth. Or at least it can be if it focuses on putting in place the gradual tax and entitlement reforms which are so sorely needed.