CBO Baseline Highlights Troubling Long-Term Future

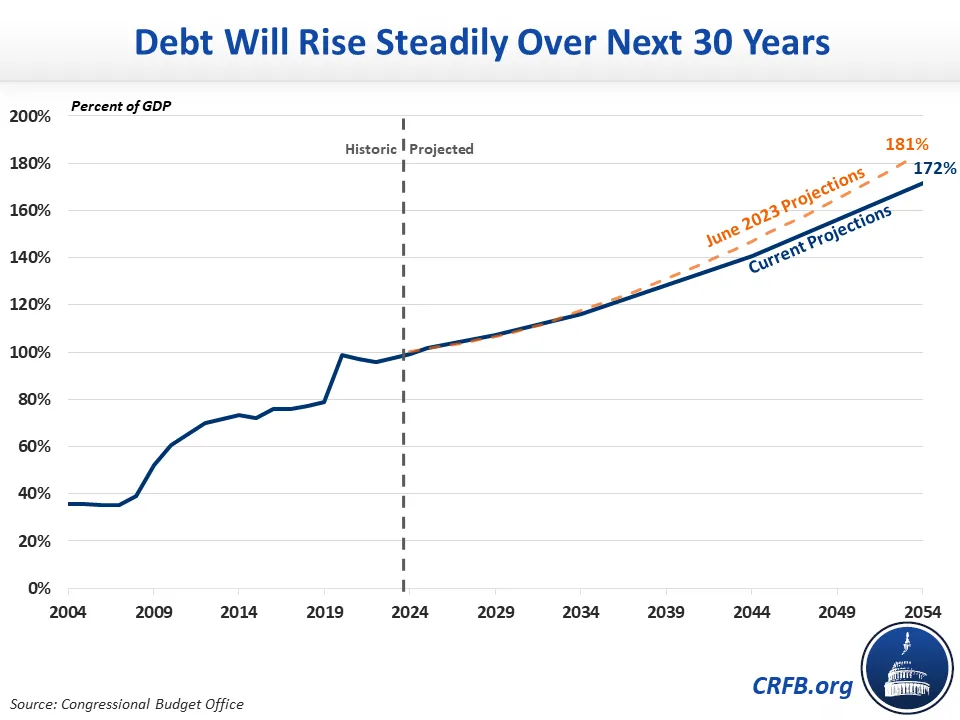

The Congressional Budget Office’s (CBO) February 2024 Budget and Economic Outlook projects that the national debt will exceed its record as a share of the economy in Fiscal Year (FY) 2028, rising to a massive 172 percent of Gross Domestic Product (GDP) by 2054. While this is a modest improvement over its June 2023 projections, CBO’s estimates spell out an increasingly unsustainable fiscal situation.

Over the next decade, the national debt held by the public will grow from roughly 97 percent of GDP today to 116 percent by 2034 under CBO’s baseline. Debt will continue to grow by about 2 percentage points of GDP per year over the following decade and 3 percentage points the decade after that, reaching an unprecedented 172 percent of GDP by 2054. That’s nearly $150 trillion in nominal dollars.

After 2034, debt will rise by more than two percentage points of GDP per year over a decade, reaching 138 percent of GDP by 2043, and then by three percentage points of GDP per year after that, reaching 172 percent of GDP by 2054.

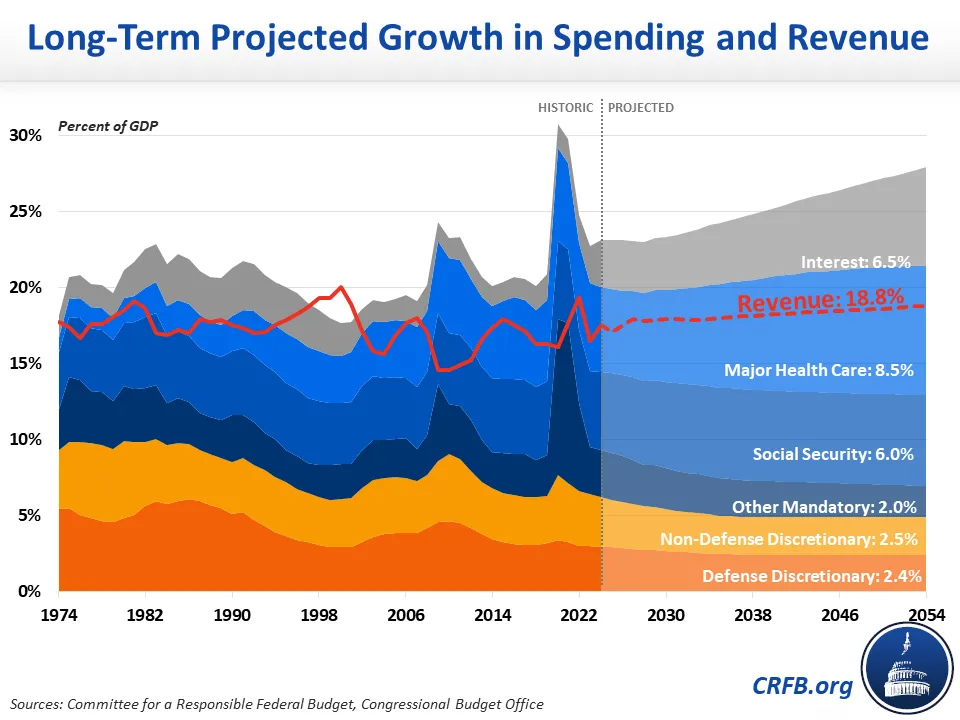

Driving this debt is a large and growing disconnect between spending and revenue. Total spending is projected to rise from 22.7 percent of GDP in 2023 and reach 24.1 percent in 2034, 26.1 percent in 2044, and 27.9 percent of GDP in 2054. Revenue will grow from 16.5 percent in 2023 to 17.9 percent in 2034, 18.4 percent in 2044, and 18.8 percent in 2054. As a result, annual deficits will explode, from a low of 5.2 percent of GDP in 2028 to 6.2 percent of GDP by 2054.

Driving the spending growth is increases in Social Security, health care, and especially interest. Social Security spending has already grown from 4.1 percent of GDP in 2001 to 5.2 percent today, and it is projected to rise further to 6.0 percent of GDP by 2054. Major health care spending rose from 3.3 percent of GDP in 2001 to 5.6 percent in 2024 and will reach 8.5 percent in 2054. And interest costs will grow from 2.0 percent of GDP in 2001 to 3.1 percent this year and 6.5 percent in 2054.

Under CBO’s baseline, large parts of the 2017 Tax Cuts and Jobs Act as well as enhanced Affordable Care Act credits would expire at the end of 2025 as written under current law, while discretionary spending would fall to historic lows as a share of the economy. Extending current policy like these (instead of letting them expire) would dramatically increase structural deficits, which would in turn push up interest rates, stifle economic growth, and lead to even higher debt.

Importantly, the long-term budget outlook assumes that revenue will rise as a share of GDP while discretionary spending will fall slightly before remaining steady throughout the latter 15 years of the window, putting revenue above and discretionary spending below historical averages. Last July, CBO estimated that a baseline that set revenue and discretionary spending on a course toward historic levels would drive debt above 250 percent by 2050, after which it would continue to grow rapidly.

Under those same estimates, CBO found that debt would rise significantly less than under the baseline – to 132 percent of GDP by 2053 – if action is taken to rescue Social Security from insolvency. Also restoring solvency to Medicare Part A and the Highway Trust Fund would result in further improvements.

The current long-term outlook is unsustainable. Policymakers should enact deficit reduction measures that slow spending growth and increase revenue to prevent such a dismal fiscal future.