ARCHIVE: Introducing the CRFB Debt Thermometer (2023)

Note: This is an archived version of the initial CRFB Debt Thermometer. For the most recent thermometer, see this page.

Fiscal policy has profound consequences on the economic health and national security of the country. Yet little is done to track the effects of legislation or executive orders enacted in a given year in a way that reaches the public. In fact, it is probably safe to say that few Members of Congress are aware of the effects of the policy changes in any year.

The CRFB Debt Thermometer has been created to bring more transparency to the process. We will track annually the fiscal impact of all major new legislation and executive orders through a tool created to make it easy for citizens, lawmakers, and the media to keep up with the ten-year costs or savings associated with new policies.

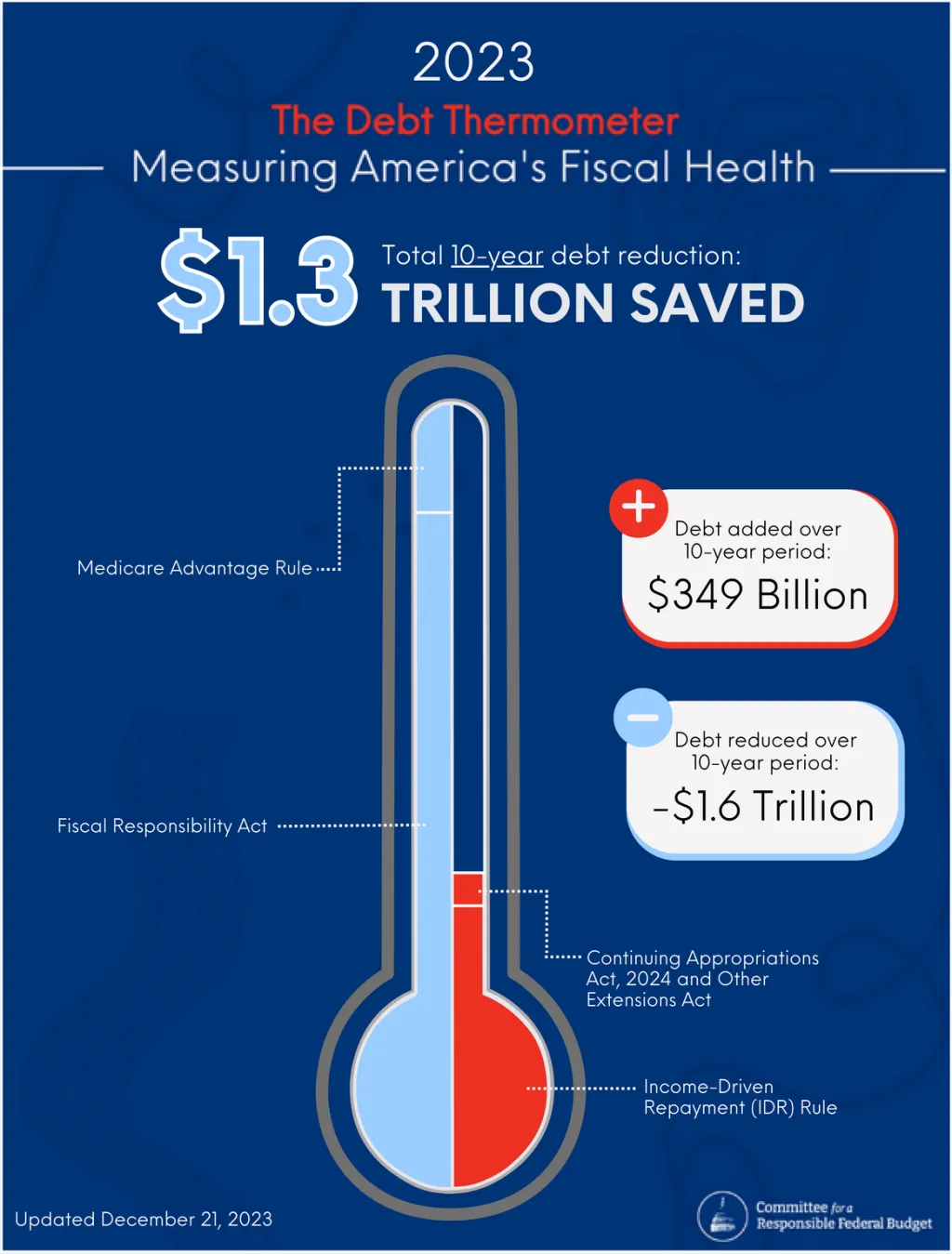

As of October 2023, policymakers have enacted $1.3 trillion of ten-year deficit reduction this year so far, consisting of more than $1.6 trillion of savings and roughly $350 billion of costs. Notably, 2023 has been an extremely positive year thus far from a fiscal perspective. We will continue to update the Debt Thermometer throughout the year.

The $1.3 trillion in net savings under the 2023 Thermometer is the result of two pieces of legislation and two additional executive orders. Specifically:

- Fiscal Responsibility Act ($1.5 trillion savings) – Enacted in June 2023, the Fiscal Responsibility Act (FRA) established binding caps on defense and nondefense discretionary spending for FY 2024 and 2025, rescinded some COVID relief and IRS funding, reformed work requirement rules in the Temporary Aid for Needy Families and Supplemental Nutritional Assistance Program, and suspended the debt ceiling through January 1, 2025, among other changes. Our $1.5 trillion savings estimate assumes appropriations grow with inflation beyond 2025 and include debt service, but they do not incorporate any side deals nor non-binding caps included in the FRA through 2029. Read more about the FRA here.

- Continuing Appropriations Act, 2024 and Other Extensions Act ($20 billion cost) – Enacted in September 2023, this law funded the government for the first 48 days of FY 2024 at FY 2023 levels, appropriated $16 billion for emergency disaster relief, and temporarily extended several expiring program authorizations. We estimate that this law will add $20 billion to deficits over a decade including debt service.

- Medicare Advantage Rule ($113 billion savings) – The Centers for Medicare and Medicaid Services finalized a regulatory action in March 2023 that would phase in a new risk adjustment model for Medicare Advantage payments over the following three years. The Congressional Budget Office estimated that an earlier version of this rule – phased in immediately rather than gradually – would have reduced deficits by more than $200 billion over a decade. Because of the changes in the regulation between its announcement and finalization, we estimate that the rule is likely to reduce deficits by closer to $100 billion over a decade or $113 billion including debt service. This estimate is subject to change.

- Income-Driven Repayment (IDR) Rule ($329 billion cost) – The Department of Education finalized a regulatory action in July 2023 creating a new income-driven repayment (IDR) plan for student loan borrowers. The new plan would increase the amount of income exempt from payment calculation, reduce the required percentage of income paid on undergraduate loans, eliminate interest accrual when payments don’t cover the entire amount of interest, and reduce the number of years in payment from 20 to 10 for borrowers who took out less than $22,000, among other changes. The Congressional Budget Office estimated that this plan will add $276 billion to deficits over a decade; we estimate a cost of $329 billion including debt service. Read more about the IDR rule here.

The 2023 Thermometer also flags several policy ideas that policymakers are considering putting forward over the remainder of 2023, marked as “Policies That May Not Be Paid For.” These include:

- Aid to Israel and Gaza – Lawmakers are considering an emergency aid package consisting of military and humanitarian aid to Israel and humanitarian aid to Gaza as a result of the Hamas terrorist attacks in October 2023. The White House requested an emergency supplemental package in October 2023 that included more than $14 billion for this purpose. Read more here.

- Aid to Ukraine – Lawmakers are considering additional emergency aid to help the Ukrainian military and economy in its ongoing war with Russia. The White House requested $24 billion in supplemental aid for Ukraine in August 2023; in October 2023, this sum was revised to $61 billion. Read more here.

- Border Security – Lawmakers are considering emergency supplemental funding to strengthen security at the southern U.S. border. The White House requested $4 billion in border security funding in August 2023 for Immigrations and Customs Enforcement, Customs and Border Protection, and migration assistance, among other needs. In October 2023, this request was revised to $14 billion. Read more here.

- Health Extenders – Lawmakers routinely extend certain expiring health policies – often referred to as “health extenders” – alongside the appropriations process. This currently includes various policies related to the health care workforce, Disproportionate Share Hospital cuts, and payments for certain Medicare programs. These policies are currently authorized through November 17 and could cost several billion dollars to extend through the end of the fiscal year.

- Physician Bonus Payment Extension – Since 2020, physicians have received bonus payments for Medicare services as part of COVID-19 fiscal support. Lawmakers began phasing the bonus payments down from 3 percent in 2022 to 2.5 percent in 2023, and they are scheduled to phase down further to 1.25 percent in 2024. However, lawmakers have begun discussing options to either avoid this phase-down or alter it. Read more here.

- Windfall Elimination Provision / Government Pension Offset Repeal – Retirees receiving benefits from the Social Security program that had some years of earnings not subject to Social Security taxes – mainly public-sector workers in certain states – have their benefits reduced by either the Windfall Elimination Provision (WEP) or the Government Pension Offset (GPO). Replacing or eliminating WEP/GPO has long been an interest in Congress, and a House bill to eliminate them without any replacement or offset has been added to the chamber’s “consensus calendar.” The Congressional Budget Office estimated a previous version of this bill would add $183 billion to deficits over the next decade. Read more here.

- Research & Experimentation Expensing – The 2017 Tax Cuts and Jobs Act changed the tax treatment of Research & Experimentation (R&E) investments starting in 2022, requiring R&E investments to be amortized over five to 15 years instead of immediately. Policymakers in both parties have proposed reverting to the previous treatment, which would cost roughly $200 billion over a decade if done permanently. Read more here.

- Looser Interest Deduction Limit – The 2017 Tax Cuts and Jobs Act placed a limitation on the deductibility of net interest expenses. For 2018 through 2021, the limit was 30 percent of earnings before interest, taxes, depreciation, and amortization, and since 2022 it has been applied to earnings before interest and taxes only. Lawmakers have discussed loosening this limit to its pre-2022 definition, which would cost $50 billion over a decade if done permanently. Read more here.

- State and Local Tax (SALT) Deduction Cap Increase – The 2017 Tax Cuts and Jobs Act capped the deductibility of taxes paid to state and local governments at $10,000 per taxpaying household. Since its enactment, some lawmakers from both parties have proposed repealing or increasing the cap. Full repeal would cost about $90 billion per year, while increasing the cap to $20,000 for individuals and to $40,000 per couples would cost about $30 billion per year. The current cap will expire alongside the rest of the individual tax provisions in 2025. Read more here.

- Child Tax Credit Expansion – The Child Tax Credit was increased from $1,000 per child to $2,000 per child under the Tax Cuts and Jobs Act of 2017 and was temporarily increased further to $3,000 per child ($3,600 per child under age 6) in 2021 under the American Rescue Plan (ARP) Act. The ARP also expanded eligibility to 17-year-olds and made the credit fully refundable, offering it to virtually all taxpayers regardless of lack of earnings or income tax liability. Lawmakers in both parties have discussed reviving some expansions of the Child Tax Credit. Restoring full refundability would cost $45 billion to $80 billion over a decade, while restoring the full ARP credit would cost $1.1 trillion to $1.6 trillion. Build Your Own Child Tax Credit here.