America Needs Tax Reform, Not More Debt

A New York Times op-ed written by Steve Forbes, Larry Kudlow, Arthur Laffer, and Stephen Moore argued that since tax reform is hard, Republicans should stop worrying about how to pay-for tax reform and just pass a giant business tax cut. But not paying for tax reform is extremely misguided, would explode the federal deficit, and end up harming long-term economic growth prospects.

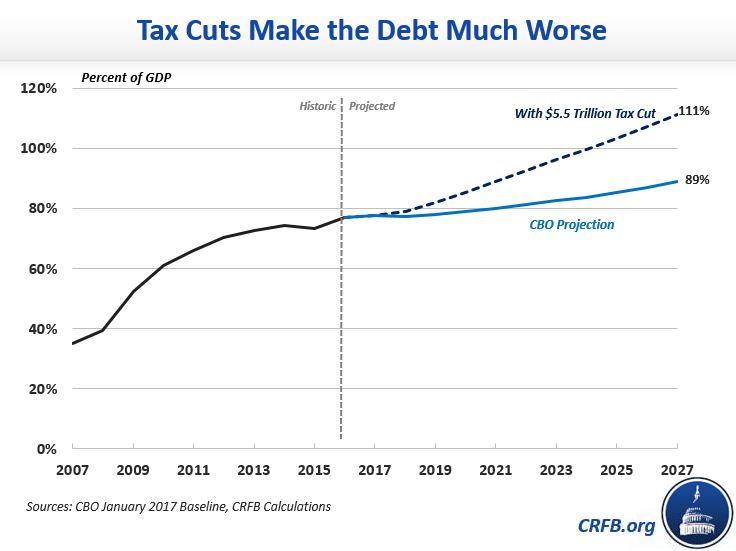

The plan the authors propose – cutting the business tax rate to 15 percent, allowing full expensing, offering a reduced rate on repatriation, and increasing infrastructure spending – could cost $5.5 trillion by our estimates. With interest, that would be enough to increase debt to 111 percent of Gross Domestic Product (compared to 89 percent of GDP in CBO's baseline) by 2027. That would be higher than any time in U.S. history, and no achievable amount of economic growth could finance it.

| Policy | 2027 Debt Impact | |

|---|---|---|

| Cost ($) | % of GDP | |

| Reduce corporate rate to 15% | +$2.2 trillion | 7.9% |

| Reduce pass-through rate to 15% | +$1.5 trillion | 5.4% |

| Enact full expensing, allow businesses to deduct items in the year they are purchased | +$1.5 trillion | 5.4% |

| Enact lower rate on repatriated tax revenues or move to territorial system* | +$100 billion | 0.4% |

| Increase infrastructure funding | +$200 billion | 0.7% |

| Subtotal | +$5.5 trillion | 19.7% |

| Interest Costs | +$700 billion | 2.5% |

| Total | +$6.2 trillion | 22.2% |

Source: CRFB calculations based on estimates of similar policies by the Tax Policy Center and the Tax Foundation. Our estimate is extremely rough, as an op-ed lacks many specified details that could change the score significantly. *The policy "impose a low tax on the repatriation of foreign profits" is particularly unclear whether it is a switch to a territorial system or simply a lower rate on repatriated earnings. We used a placeholder of $100 billion, which is close to either the Tax Policy Center's estimate of switching to a territorial system as part of the House GOP tax plan or the Joint Committee on Taxation's estimate of a voluntary repatriation holiday (though a permanently lower rate would be more expensive). Our infrastructure placeholder is a rounded amount similar to the size of the tax credits that then-Trump campaign advisors Peter Navarro and Wilbur Ross presented late in the 2016 campaign.

Tax Cuts Are More Effective When They are Paid For

As we explained in 5 Reasons to Pay for Tax Reform, fiscally responsible tax reform is far better for the country than debt-financed tax cuts.

For one, the country currently spends $1.6 trillion per year on tax breaks – many of which distort economic decision-making and result in a misallocation of resources. Tax reform can repeal or reform many of these tax breaks and thus improve economic efficiency. The International Monetary Fund (IMF) recently estimated that this effect could be significant. The op-ed authors' plan would in some ways worsen allocative decisions by allowing companies to fully expense investments while fully deducting interest costs.

Outside of the allocative effects, debt-financed tax cuts are also generally less pro-growth than responsible tax reform. Last year, for example, the Tax Policy Center estimated President Trump's $6 trillion campaign tax plan would reduce GDP by 0.5 percent after a decade and 4 percent after two. By comparison, estimates of former Ways and Means Chairman Dave Camp's (R-MI) deficit-neutral tax reform from 2014 found it would improve GDP by 0.1 to 1.6 percent after a decade.

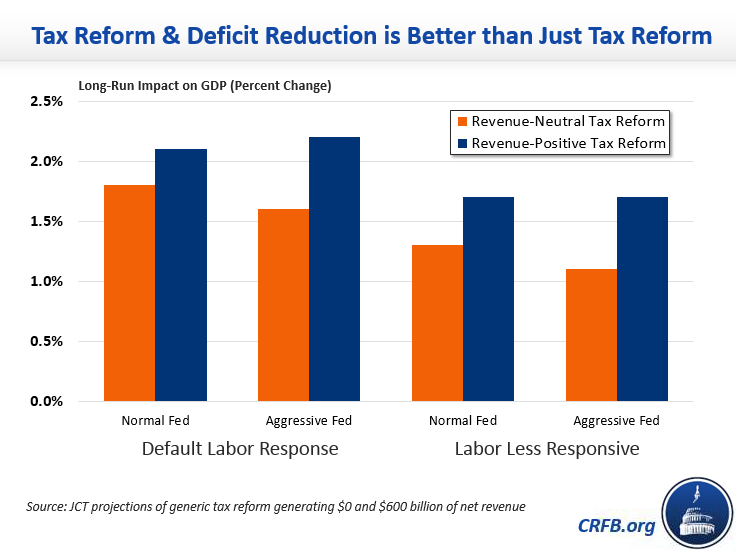

Indeed, looking at two nearly-identical tax reform packages, the Joint Committee on Taxation estimated in 2011 that one producing $600 billion of net revenue would generate about one-third more growth over the long run than a revenue-neutral tax reform with the same structure.

America Can't Afford a $5 Trillion Tax Cut

At 77 percent of GDP, debt is currently higher than at any time in history outside of World War II and its aftermath. Even under current law, debt will rise to 89 percent of GDP by 2027. Under the plan put forward by the authors, debt would rise to 111 percent of GDP by 2027 – a new historical record. In dollar terms under their plan, debt held by the public would total $31 trillion and gross debt would total $36 trillion.

Growth Can't Pay for This Tax Cut

The authors acknowledge that the plan will add to short-term deficits but contend that faster economic growth will pay for the plan and reduce deficits in the long run. However, there is no evidence that broad-based tax cuts can pay for themselves completely, and economic studies from across the spectrum have found that deficit-financed tax cuts only pay for a fraction of their cost (including from the Congressional Budget Office and other economists). Indeed, tax reform that slows economic growth by adding too much to debt can actually cost more once economic effects are incorporated.

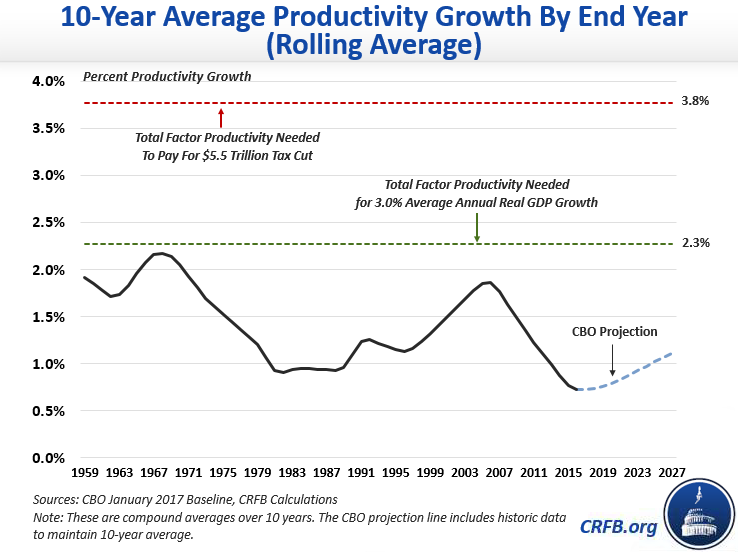

Even if tax cuts could generate more growth than estimated, no plausible amount of economic growth would be able to pay for the tax plan, let alone reduce deficits. The country would need roughly 4.5 percent sustained growth to pay for the tax plan – two-and-a-half times the 1.8 percent that CBO projects to occur over the next decade. As we explained in Don't Count on 4% Growth, the last time the country achieved even 4 percent sustained growth was in the late 1960s and early 1970s (though we came close during the technological boom of the 1990s). With an aging population, those growth rates are no longer possible. Achieving just 3 percent growth would require productivity growth to rise to the record levels set in the late 1960s and early 1970s.

Further, the Trump Administration and many members of Congress have talked about using economic growth to pay for other proposals and reduce the deficit. If all the gains from growth are being used to pay for tax cuts, then none are being used to pay for anything else or reduce the deficit.

In order to fulfill the campaign promise of using growth to reduce the deficit, any tax reform plan should be at least revenue neutral before accounting for economic growth, so all the gains from growth can be devoted to deficit reduction.

Forbes, Kudlow, Laffer, and Moore cite the historic examples of President Reagan's 1981 tax cut. However, they fail to mention that President Reagan's 1981 tax cut was too steep. After 1981, it was clear that the budget projections that allowed the cut were overly optimistic, and the cuts needed to be rolled back. It was followed in 1982 by the second-largest tax increase in history (in inflation-adjusted dollars) and another tax increase in 1984. The Office of Management and Budget estimated that about 40 percent of President Reagan's tax cut was offset with subsequent increases during President Reagan's term.

Tax reform is hard. It requires that policymakers make tradeoffs between lowering rates and deciding which tax provisions to eliminate. But paid-for tax reform is better for growth than deficit-increasing tax reform. The proposal put forward by Forbes, Kudlow, Laffer, and Moore would explode the national debt and diminish growth prospects.

Tags

What's Next

-

Image

-

Image

-