What We’d Like to See in President Trump’s FY 2018 “Skinny Budget”

The Trump Administration is expected to soon release its first budget outlining the President’s priorities for Fiscal Year (FY) 2018 and the subsequent decade. The release will most likely be a “skinny budget,” a summary document often used by incoming presidents to advance their proposals before additional details are released later in the year.

The President’s first budget is a critical opportunity to translate campaign promises into policy proposals and show how those proposals will affect the government’s bottom line. Historically, many of the policies from the first budgets of past presidents were eventually enacted into law in some form.

Although a skinny budget will understandably not have the same level of detail as a full budget, it will have enough to assess the President’s priorities. Fiscal responsibility should be one of them.

Specifically, President Trump’s first budget should:

- Put Debt on a Clear Downward Path Relative to the Economy

- Pay for New Initiatives with Specific Offsets

- Use Realistic Economic Growth Assumptions

- Avoid Gimmicks and Unspecified Savings

- Propose Entitlement Reforms to Slow Cost Growth and Improve Solvency

- Propose Tax Reform that Grows the Economy and Raises Revenue

The choices made in the President’s budget could have a major impact on fiscal policy for the next four years and beyond. A budget that addresses the country’s historic fiscal challenges will demonstrate that the new Administration is serious about controlling the unsustainable growth of federal debt that threatens to undermine America’s future.

Put Debt on a Clear Downward Path Relative to the Economy

President Trump entered office with higher debt as a share of the economy than any U.S. President besides Harry Truman. And unlike under President Truman, debt is projected to grow continuously over the course of Trump’s presidency and beyond. Currently, debt held by the public totals $14.4 trillion or 77 percent of Gross Domestic Product (GDP), which is nearly twice the historical average. Under current law, it is projected to reach $25 trillion or 89 percent of GDP by 2027. And by 2050, debt is on course to reach about 150 percent of GDP.

Fig. 1: Historical and Projected Debt-to-GDP Ratio, 1790-2050

Source: Congressional Budget Office, CRFB calculations

President Trump should set a fiscal goal that puts the debt on a clear downward path relative to the economy over the next decade and beyond. The budget should also contain specific policy proposals that meet that goal under reasonable assumptions.

Fig. 2: Deficit Reduction Needed to Meet Fiscal Goals (Trillions over 10 years)

Source: CRFB calculations based on the January 2017 CBO baseline and assuming deficit reduction scales up over time as in former House Budget Chairman Price’s FY 2017 budget proposal

There is no one right fiscal goal, and many different options could put debt on a downward path. One possible goal would be to bring the budget into balance over the next ten years. We recently estimated that achieving this goal would require just over $8 trillion of total deficit reduction over a decade. Another option would be to reduce the debt-to-GDP ratio to 70 percent within a decade, which would require over $5 trillion in ten-year savings.

Pay for New Initiatives with Specific Offsets

Any new administration will enter office with its own priorities that require new spending or tax reductions. So far, President Trump has proposed building a wall on the Mexican border, strengthening the military, increasing infrastructure spending, repealing and replacing the Affordable Care Act (ACA), and reducing taxes for individuals and businesses.

If enacted without offsets, most of these initiatives would add to the already large and growing national debt. To avoid this outcome, the budget should propose that each new initiative is fully paid for with spending cuts or additional revenues.

Although a skinny budget might not have quite as much detail as a full budget, it should not make vague promises of offsets. Any offsets should be at least as detailed as the policies they are intended to pay for.

When stuck in a hole, the first rule is to “stop digging.” Paying for new initiatives will prevent the debt from getting worse and help assure that policymakers have weighed the tradeoffs involved in pursuing any new initiatives.

Use Realistic Economic Growth Assumptions

President Trump has made economic growth a centerpiece of his agenda, and rightly so. Faster economic growth can create jobs, lift wages, strengthen retirement security, and improve the lives of individuals and families.

Faster economic growth can also improve the nation’s fiscal situation – just a 5 percent (0.1 percentage point) increase in the projected annual growth rate can reduce the debt by nearly $300 billion over the next decade.

President Trump’s budget should propose an agenda that supports economic growth, but it should use growth assumptions that are realistic and grounded in economic evidence and theory. Over the next decade, the Congressional Budget Office (CBO) estimates real GDP growth will average about 1.9 percent per year – an estimate based on current law and roughly in line with outside forecasts.

Since the Office of Management and Budget’s (OMB) economic projections are based on the policies the President puts forward, it would not be unusual for their GDP projections to differ modestly from CBO’s. However, any reasonable deviation from CBO would likely be measured in basis points or perhaps decimal points, not percentage points.

Claims of four or even three percent sustained economic growth should be viewed as aspirational and have no place in any official government projection. The last time the United States achieved four percent average annual growth for ten years was the late 1960s and early 1970s, and this faster growth was largely driven by demographic tailwinds that no longer exist.

With an aging population, growth today would need to come largely from improvements in productivity. Four percent economic growth from productivity alone would require productivity growth rates of 3.2 percent over the next decade, which the U.S. has never sustained in its history.

Even if productivity reached its previous record of sustained growth seen in the 1960s, total GDP growth would only reach three percent annually. There is no justification for assuming such a high level of growth.

Fig. 3: Total Factor Productivity Growth Needed to Meet Real GDP Growth Targets

Source: CBO January 2017 Baseline, CRFB Calculations

Policymakers should work to encourage and achieve as much economic growth as possible. But fantasy growth projections obscure our very real fiscal challenges while setting expectations that cannot possibly be fulfilled.

Avoid Gimmicks and Unspecified Savings

The budget should show that the Administration’s policies are fiscally responsible without resorting to gimmicks or budgetary sleights of hand. Past budgets have used a variety of gimmicks to hide the cost of proposals and exaggerate the savings they would achieve. Using such deception to make the budget look fiscally responsible would signal that the Administration is not serious about dealing with the debt.

As a general rule, the budget should avoid relying on “magic asterisks” or other placeholders that assume budgetary savings without policies to back them up. Because of the rush to produce a skinny budget, there is room for a small amount of leeway on this principle, as policies may still be in development. However, the Administration should offer as much specificity as possible, ensure offsets are at least as specific as the policies they are paying for, and follow up soon with further detail where it is lacking.

The budget should also avoid timing gimmicks that save money in the first decade only by pushing costs to future decades. These should not be considered a net gain for the Treasury. Similarly, temporary or one-time savings, such as asset sales, should not be used to offset permanent costs.

Finally, the budget should use a traditional current law baseline and not attempt to hide the cost of tax cuts or spending increases by burying them in the baseline. For example, if President Trump wants to preserve all expiring tax extenders and continue delaying various ACA taxes, his budget should include the $750 billion revenue loss from these proposals – not build the cost into the baseline and pretend the cost is $0.

Propose Entitlement Reforms that Slow Cost Growth and Improve Solvency

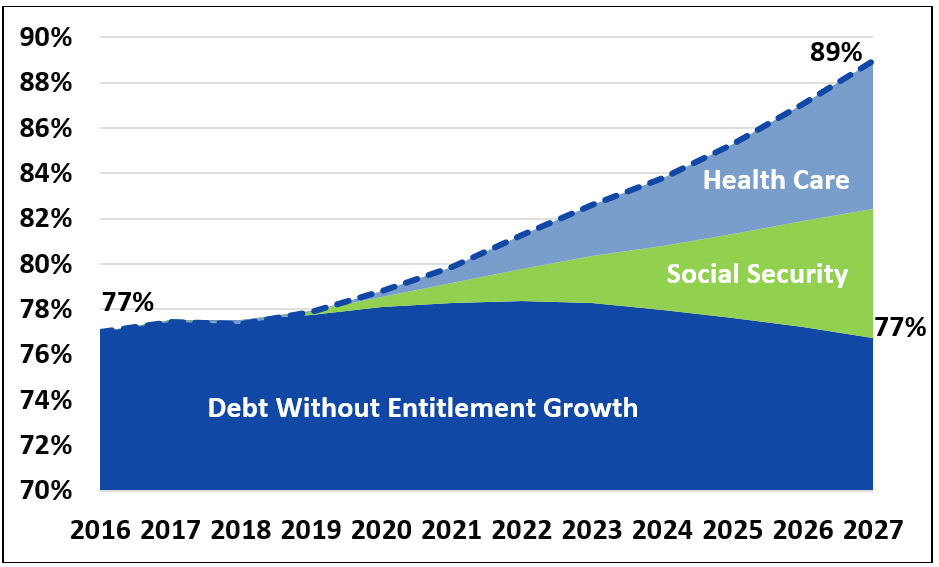

An aging population and rising health care costs will put significant pressure on the budget during and after President Trump’s time in office. Social Security and health care spending currently constitute over half of all non-interest spending and are responsible for more than three-quarters of nominal non-interest spending growth over the next decade. As a share of GDP, they are responsible for more than the entirety of projected spending growth; other parts of the budget are projected to shrink relative to the economy.

Fig. 4: Debt Held by the Public With and Without Entitlement Growth (Percent of GDP)

Source: CRFB calculations based on CBO January 2017 Baseline; “Health Care” refers to major federal health programs such as Medicare, Medicaid, and ACA insurance subsidies.

By driving up spending faster than revenue, the growth of Social Security and health care programs is a major contributor to rising debt levels. If neither grew faster than the economy over the next decade, debt would be stable and ultimately decline as a share of the economy.

The rising cost of entitlement programs also puts their internal financing at risk. Currently, Social Security spends more than it raises in dedicated revenue, and CBO projects this trend will continue (and worsen) until its trust funds are depleted (on a theoretical combined basis) by 2029. Similarly, the Medicare Hospital Insurance trust fund is projected by CBO to become insolvent by 2025. (The programs’ Trustees estimate depletion dates of 2034 and 2028, respectively.)

To slow rising debt levels, create fiscal space for other programs, and ensure Social Security and Medicare solvency, President Trump should put forward significant entitlement reforms in his budget.

On the health care side, he should focus on measures that encourage providers and beneficiaries to deliver and use care more efficiently in order to bend the health care cost curve downward. For Social Security, President Trump should propose gradual and targeted adjustments to ensure long-term solvency and ultimately bring revenue and costs in line or, at minimum, move significantly in that direction.

Propose Tax Reform that Grows the Economy and Raises Revenue

The federal tax code has not been reformed in over three decades and is in clear need of updating. By reducing the $1.6 trillion in annual tax breaks in the current code, thoughtful tax reform can lower tax rates, reduce distortions, improve simplicity and fairness, enhance competitiveness, promote economic growth, and help address our rising debt.

Comprehensive tax reform is an in-depth process that requires going line by line through the tax code. While we do not expect to see a full proposal fleshed out in the skinny budget, the Administration should use the opportunity to outline the basic framework of the tax reform they are proposing, including their (preferably revenue-positive) revenue target.

The Administration should put forward as many specific tax proposals as possible and highlight which tax breaks they believe should be repealed or reformed. Proposals that raise revenue for tax reform should be at least as large and as specific as those that would reduce revenue.

* * * * *

The President’s budget is one of the first meaningful statements of the Administration’s legislative priorities. On the campaign trail, President Trump frequently spoke out about the dangers of a high and rising national debt. His budget should include a detailed, thoughtful, and honest plan to begin addressing the nation’s historic fiscal challenges.