Re-Estimating the President’s Budget with Reasonable Economic Assumptions

Today, the President released his full Fiscal Year (FY) 2018 budget proposal. The Administration finds that its policies would balance the budget by 2027 and reduce debt from 77 percent of Gross Domestic Product (GDP), or $14.3 trillion, today to 60 percent of GDP, or $18.6 trillion, by the end of the decade. However, this projection appears to be based on unrealistic growth assumptions that are unlikely to materialize.

In this paper, we show that:

- The Administration’s projections of 3 percent economic growth are far above those of outside forecasters and would require exceeding the economic performance of the 1990s.

- Under realistic economic assumptions from the Congressional Budget Office (CBO), debt in the President’s budget would remain roughly at current levels rather than fall precipitously; deficits would remain above 2 percent of GDP rather than disappear by 2027.

- Using different sets of assumptions, debt will range from 72 to 83 percent of GDP by 2027, and deficits will range from 1.7 to 4.0 percent of GDP.

The unrealistic assumptions in the President’s budget help it to achieve substantial debt reduction and an ultimately balanced budget on paper but do nothing to assure a strong fiscal footing in reality. These growth numbers are not only unrealistically high, but using the revenue from feedback from economic growth toward deficit reduction – which we support – is inconsistent with recent statements that economic growth would be used to help finance tax reform.

Rather than making unrealistic assumptions, the President must make the hard tax and spending choices needed to truly bring the national debt under control.

Re-Estimating the President’s Budget

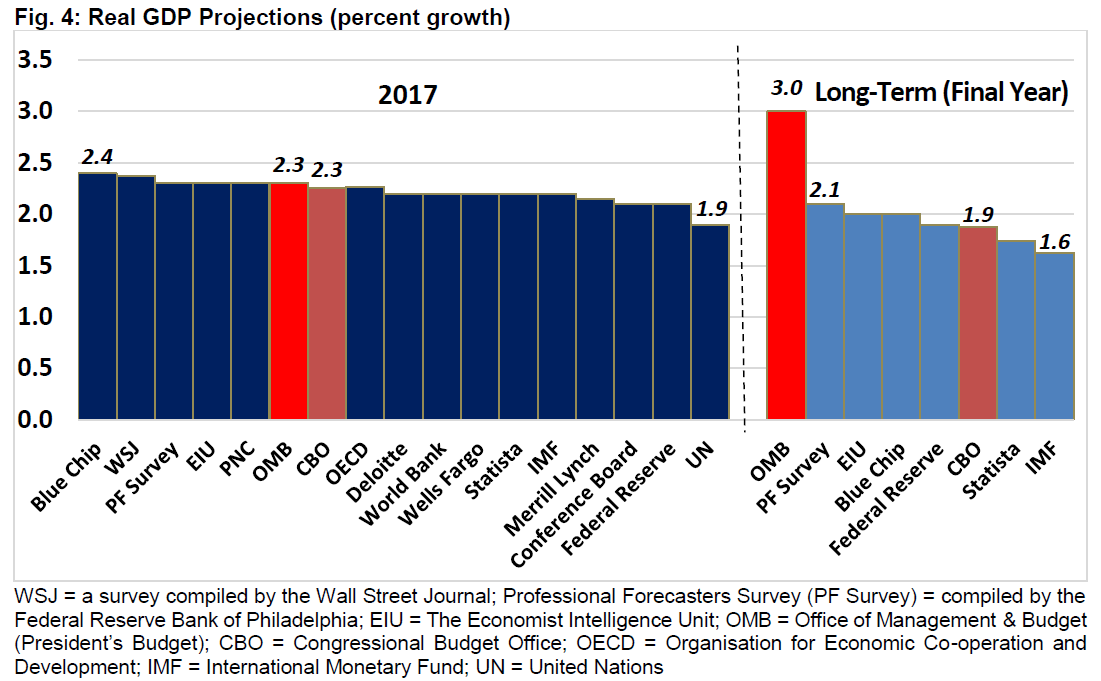

In constructing its budget numbers, the President’s budget uses much more favorable economic growth assumptions than CBO, projecting average real growth of 2.9 percent over ten years compared to 1.8 percent in CBO’s projection. Part of this is due to the Office of Management and Budget (OMB) assuming higher baseline growth of 2.2 percent, while the rest comes from the budget’s effects on growth.

OMB often assumes faster growth than CBO, in part because its growth estimates are inclusive of the President’s presumably pro-growth policies. Yet in the past two decades, OMB’s growth estimates have averaged just 0.2 points above CBO’s, with the largest difference being 0.4 points. The 1.1 percentage point difference between this budget and CBO is an outlier.

Higher growth rates lead the budget to show much lower debt levels than would otherwise be the case, mainly due to higher projected tax revenue. Higher growth also means a larger economy and therefore lower debt and deficits as a share of GDP. OMB estimates nominal GDP will be 11 percent higher by 2027 than what CBO estimates.

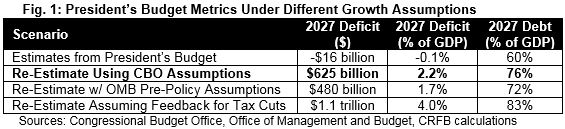

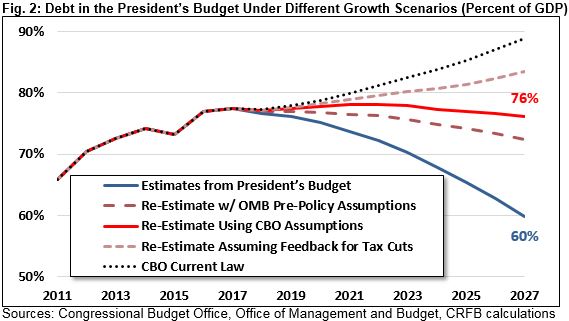

In large part due to this growth, OMB projects debt under the President’s budget to fall from 77 percent of GDP ($14.2 trillion) today to below 60 percent of GDP ($18.6 trillion) by 2027. By comparison, our rough estimates suggest debt would total 76 percent of GDP ($21.3 trillion) using CBO’s economic assumptions. In other words, debt would be 16 percent of GDP and $2.7 trillion higher using CBO’s economic projections than it would be under OMB’s.

To be sure, CBO’s economic projections may be too pessimistic, particularly in light of the pro-growth policies included in the President’s budget. Using OMB’s pre-policy assumptions, which project average growth of 2.2 percent per year rather than CBO’s 1.8 percent, debt would fall modestly to 72 percent of GDP ($20.6 trillion) by 2027.

On the other hand, it is possible that debt would be even higher. Though the budget dedicated all revenue from economic growth toward deficit reduction, in recent weeks the Administration has been touting economic growth as a way to pay for its tax plan.

If the White House decides to dedicate all its estimated gains from additional growth to pay for tax reform, debt would rise to 83 percent of GDP ($23.4 trillion) by 2027 using CBO’s economic assumptions.

In all three of these cases, debt under the budget would be lower than the 89 percent of GDP ($24.9 trillion) CBO estimates will occur by 2027 under current law. Still, debt would be much higher than OMB’s estimates.

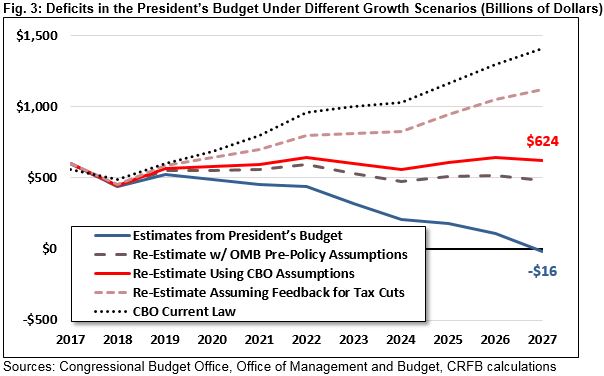

The same story is true for deficits. While OMB projects the budget will be in balance by 2027, the deficit will total $625 billion (2.2 percent of GDP) using CBO economic assumptions.

Under the more optimistic OMB pre-policy assumptions with 2.2 percent annual growth, deficits in 2027 will total $480 billion (1.7 percent of GDP). Assuming claimed gains from growth are used for tax reform and using CBO’s growth assumptions, deficits will total $1.1 trillion (4.0 percent of GDP) by 2027. All are improvements relative to current law but not nearly as much as claimed by the budget.

The President Should Not Count on 3 Percent Growth

While working toward 3 percent economic growth is laudable, assuming it will materialize to make budget math work is extremely unrealistic. Achieving 3 percent economic growth would require a heroic combination of good policy and good luck.

As we detailed in a recent analysis “How Fast Can America Grow?” most forecasters expect the economy to grow by about 2 percent per year on a sustained basis. CBO projects real growth of just 1.9 percent in the long term, while the highest forecast we identified – from the Professional Forecasters Survey – projects 2.1 percent. The International Monetary Fund (IMF) projects the U.S. economy will grow by 1.6 percent in its final year of analysis.

The Administration’s economic growth assumptions are well outside of the consensus of what other economic forecasters think is reasonable.

Given the aging of the population, there is little precedent for the level of labor, capital, or productivity growth that would be necessary to achieve 3 percent sustained economic growth. In “How Fast Can America Grow?” we estimated that economic fundamentals would have to exceed levels reached during the 1990s boom in order to achieve 3 percent growth. This scenario is not completely unfathomable, but it is highly unlikely given current trends and certainly should not be counted on.

To be sure, if enacted, the President’s budget would very likely result in faster economic growth than what CBO projects under current law. Deficit reduction, Affordable Care Act repeal, and pro-work reforms to several means-tested and disability programs should all help to improve growth. So too would tax reform and regulatory reforms, though these policies are not detailed in the budget.

However, these changes are likely to improve the country’s growth rate by decimal points, not percentage points. A reasonable guestimate would be that these policies lift average projected growth rates from 1.8 to 2.2 percent – or, put another way, from CBO’s current law baseline to OMB’s pre-policy growth rate. Further growth may be possible, but anything approaching 3 percent is unlikely.

Conclusion

The President’s budget includes significant spending-side deficit reduction, but it also relies on unrealistic growth assumptions to make its numbers look better. Without that added growth, debt in the budget would total 72 to 83 percent of GDP by 2027 instead of the 60 percent estimated by OMB. The deficit in 2027 would total $480 billion to $1.1 trillion rather than the budget being in balance.

Even with realistic growth estimates, the budget would result in lower deficits and debt than under current law. However, they would not be nearly as low as the Administration claims and certainly not if the final detailed tax plan dramatically reduces revenue.

The use of rosy growth assumptions sets a bad example for other budgets or major legislation that may be considered. Rosy growth assumptions may also open the door to dangerous deficit-increasing policies that may ultimately slow rather than accelerate economic growth.

Faster economic growth must be a central goal for policymakers, but it should not be a crutch used to avoid difficult choices.

This paper was updated after publication to include OMB's growth projections in Figure 4, a graph made for our full paper on the President's Budget released on May 24.