A Mini-Bargain to Improve the Budget

A new version of this paper exists that was updated to include savings for disaster relief.

The national debt is currently at its highest share of the economy since just after World War II and is set to rise rapidly. Fixing our unsustainable fiscal situation will require a multiyear plan with a mix of spending cuts, structural reforms to slow the rising costs of entitlement programs, and an increase in revenue.

Unfortunately, policymakers are far from negotiating a “grand bargain” to fix the debt. Instead, many are pursuing policies that would further increase debt by cutting taxes under the guise of tax reform and increasing defense and non-defense discretionary spending above current law caps.

To refocus efforts in the right direction, America needs a “mini-bargain” on the budget. That bargain should put in place measures to prevent unpaid-for tax cuts and spending increases, make a down payment on debt reduction, and establish a process for further reforms down the road. We propose a six-part framework:

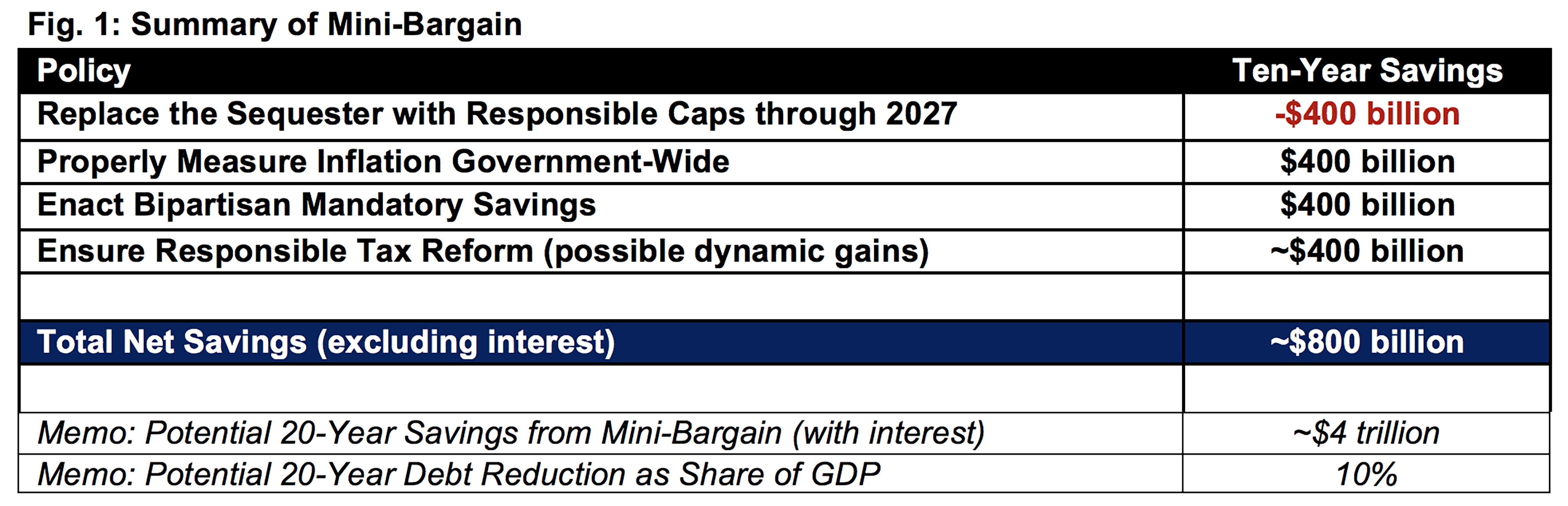

- Replace the sequester with realistic and responsible discretionary caps, fully offset with $400 billion of savings from measuring inflation properly.

- Strengthen Pay-As-You-Go (PAYGO) to facilitate responsible tax reform that is at least revenue-neutral on a conventional basis. Rather than cutting taxes, policymakers should enact tax reform, which could help grow the economy and generate $400 billion of deficit reduction.

- Enact bipartisan mandatory savings to save $400 billion over ten years with reforms to some of the largest drivers of the debt, including health care and retirement programs.

- Establish a Social Security commission tasked with averting the 23 percent across-the-board cuts looming in 2034 and ensuring sustainable solvency.

- Increase the debt ceiling to avoid a default on the national debt.

- Reform the budget process to increase efficiency, improve accountability, and include a long-term focus.

This plan will not fix the debt, but it could easily save $1.2 trillion over a decade.

One-third of these savings would be used to make important investments in education, infrastructure, research, national security, and other core government functions. The rest would help slow the growth of the national debt, improve Social Security solvency, and buy time for further reforms.

Over two decades, this package could save nearly $4 trillion in total.

Policymakers should seriously consider this mini-bargain as an important first step toward long-term sustainability and prosperity.

We cannot afford to continue on our current path.

Replace the Sequester with Realistic and Responsible Discretionary Caps

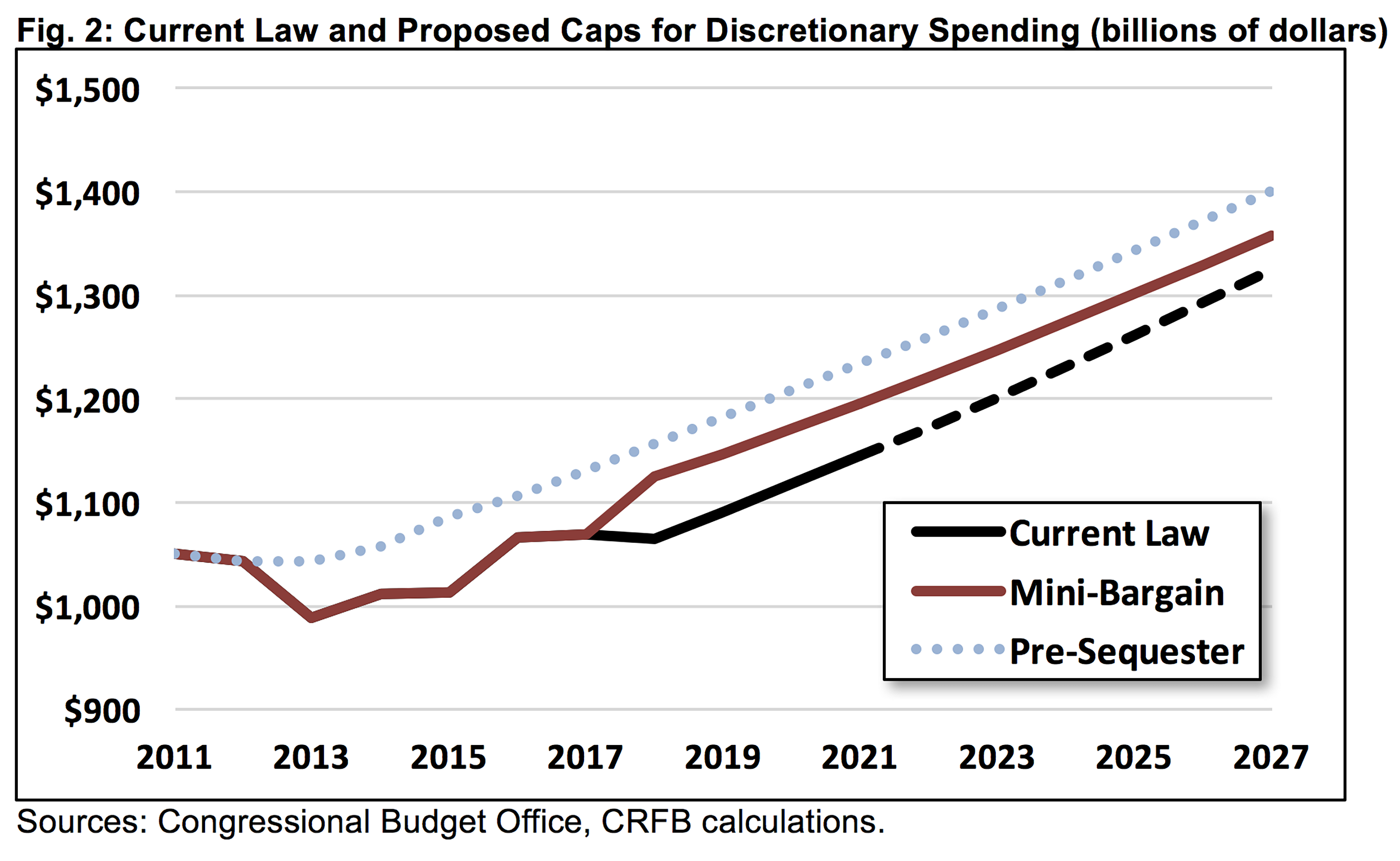

Sequester-level caps on defense and non-defense discretionary spending are set to return in full force in Fiscal Year (FY) 2018, lowering discretionary spending levels to about $90 billion below the originally agreed-upon Budget Control Act caps (this year, spending is about $61 billion below those levels, though this reduction is partly offset by excessive spending on overseas contingency operations). Under current law, these sequester-level caps will continue through 2021, after which discretionary spending will no longer be capped at all. A “mandatory sequester” also cuts certain mandatory spending programs by $10 billion to $15 billion per year through 2025.

Congress has never actually adhered to the sequester-level caps, and there is broad desire to lift the defense caps, the non-defense caps, or both. This is not surprising: the sequester was intended to be an enforcement measure to prompt policymakers to agree to smarter deficit reduction, not an actual policy to be followed. Rather than adjusting the caps a year or two at a time as lawmakers have done since 2013, a responsible budget deal could permanently replace the sequester with new sustainable caps that continue through the next decade.

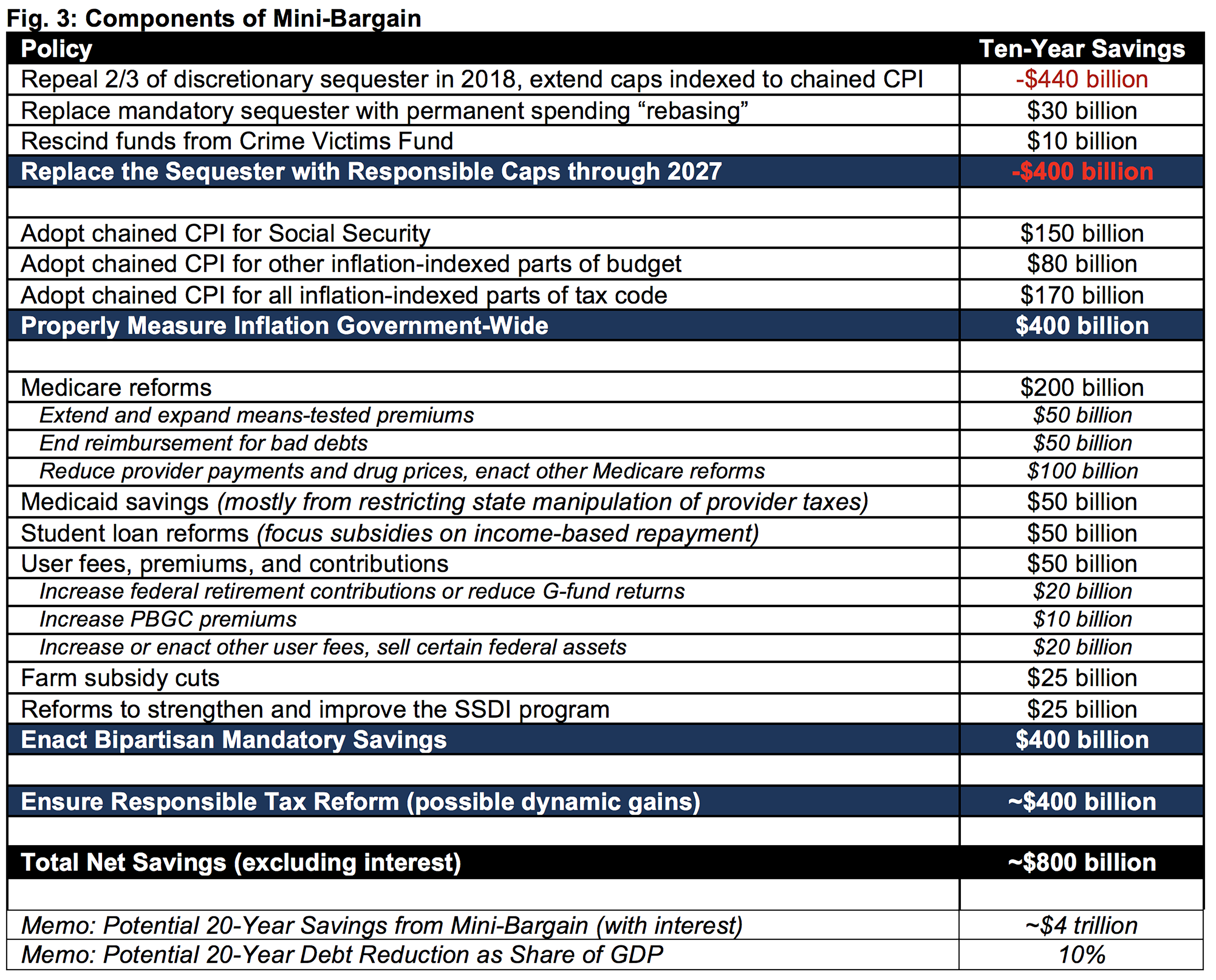

As part of the mini-bargain, we propose eliminating two-thirds of the sequester for FY 2018, setting total caps at $1.13 trillion instead of $1.06 trillion. We then propose indexing those caps with inflation – as measured by the chained Consumer Price Index (CPI) – through 2027. This would permanently replace the discretionary sequester and extend the caps well beyond their current 2021 expiration.

We also propose replacing the mandatory sequester with a permanent “rebasing” of Medicare and other payments that allows them to grow off of today’s levels. This would effectively continue reductions from the mandatory sequester but do so in a more transparent and predictable way. Spending levels would be set by legislation instead of annual calculations from the Office of Management and Budget.

Finally, we propose rescinding money from the Crime Victims Fund (CVF). On paper, this will generate $10 billion of savings, but much more importantly, it will prevent policymakers from repeatedly delaying spending of CVF funding in order to claim $10 billion per year of changes in mandatory programs (CHIMPs) to offset discretionary costs. In other words, this would remove a major budget gimmick.

Taken together, this sequester relief package would cost about $400 billion over a decade. That cost could be fully offset by adopting a more accurate measure of inflation throughout the budget and tax code.

A number of programs and tax provisions are currently indexed using the Consumer Price Index (CPI), even though economists across the spectrum agree this index overstates inflation. Correcting this overstatement by adopting the chained CPI instead would reduce projected spending by roughly $230 billion over a decade (including $150 billion from Social Security1) and increase revenue by about $170 billion. Policymakers could also add enhancements for low-income supports to offset the resulting effects of chained CPI on more vulnerable populations.

Though this sequester replacement would be budget-neutral in the first decade, we estimate it would reduce the debt by roughly $1 trillion (2.4 percent of Gross Domestic Product) after two decades.

Strengthen PAYGO to Facilitate Responsible Tax Reform

The federal tax code is in many ways broken and has not been seriously reformed in over 30 years. Currently, policymakers are in the process of negotiating reforms to the tax code. Designed properly, such a package could improve simplicity, fairness, efficiency, and overall economic growth. However, those goals would be undermined if the reform turned into a debt-financed tax cut.

As part of the mini-bargain, policymakers should therefore strengthen Pay-As-You-Go (PAYGO) rules to ensure that tax reform is not allowed to add to the debt.

Perhaps most importantly, the existing Senate PAYGO rule – which aims to prevent most legislation from adding to the debt – should be codified into law so that the Senate cannot reverse it in its budget resolution. Emergency exemptions should still be allowed, but they should require a 60- or 67-vote threshold in the Senate and a separate vote in the House. In addition, Congress should be prohibited – absent a super majority – from exempting costs from PAYGO in a budget resolution or tax and spending legislation and prohibited from wiping deficit increases from the PAYGO scorecard.

Second, policymakers should clarify that PAYGO will be measured using conventional scoring relative to the Congressional Budget Office’s (CBO) current law baseline. This would prevent policymakers from slipping a $460 billion “current policy” tax cut into a tax reform bill and would ensure that dynamic revenue gains from pro-growth tax reform would go towards debt reduction.

These changes would have no direct effect on the budget, but they could forestall hundreds of billions, or perhaps trillions, of dollars from being added to the deficit. At the same time, they could lead to pro-growth and fiscally responsible tax reform that ultimately would generate significant deficit reduction – perhaps in the range of $400 billion – as a result of faster economic growth. While actual revenue gains would vary, aiming for $400 billion is a reasonable goal. For example, the Joint Committee on Taxation estimated that the Tax Reform Act of 2014, which lowered rates and broadened the base in a revenue-neutral manner, would generate between $50 billion and $700 billion in additional dynamic revenue. The types of reforms currently under discussion could be even more pro-growth.

Enact Bipartisan Mandatory Savings

Just keeping the debt at today’s post-war record-high as a share of the economy over the next decade would require $3.2 trillion of spending cuts or tax increases. Putting debt on a downward path would require even greater savings.

While a mini-bargain will not include enough savings to fix the debt, it should at least make progress where areas of agreement already exist. Many proposals from either President Trump’s budget, former President Obama’s budgets, or other budget savings proposals have the potential for bipartisan support.

We therefore propose that, as part of this mini-bargain, policymakers pass at least $400 billion of savings over ten years. Congress and the President will need to negotiate the precise details of such a package, but it could be based on the following framework (with savings estimates over ten years):

Medicare Reforms ($200 billion). Medicare is the second-largest and second-fastest growing government program. Experts and policymakers from all ideological stripes agree there are ways to slow its cost growth without hurting access to or quality of care. A $200 billion package of savings could include: the expansion of various payment reforms, reductions in overpayments to providers (particularly for post-acute care), the elimination of reimbursements for bad debts, reforms to discourage the unnecessary use of brand-name and high-cost prescription drugs, and a modest expansion of existing means-tested premiums. Nearly all of these proposals, in some form, were included in President Obama’s final budget and should be acceptable to Republicans as well.

Medicaid Savings ($50 billion). Medicaid, a joint federal-state program, is one of the fastest growing parts of the federal budget. Although the program serves a vulnerable population, cost reductions are possible. We recommend policymakers pursue $50 billion of savings, totaling about 1 percent of program costs. To achieve this, the federal government should crack down on state efforts to manipulate their federal match through provider taxes and other gimmicks. Smaller additional savings could be generated by better accounting for lottery winnings in determining eligibility, modifying payments for administrative costs, and encouraging states to experiment with cost-saving initiatives.

Student Loan Reforms ($50 billion). The Federal Direct Student Loan Program, which issues loans for undergraduate and graduate studies, is another possible area for savings. Both President Trump and President Obama proposed moving toward a single, progressive, and streamlined income-based repayment program. Policymakers could either adopt an ambitious reform to repeal the ineffective and poorly targeted “in-school interest subsidy” and overhaul income-based repayment or a more modest reform to simply streamline income-based repayment and limit the in-school interest subsidy to one’s time as an undergraduate. Either option would save federal dollars while increasing simplicity and progressivity.

User Fees, Premiums, and Contributions ($50 billion). Both President Trump and President Obama proposed increasing non-tax government receipts through a variety of policy changes. A mini-bargain could incorporate many of these ideas, including: higher Pension Benefit Guaranty Corporation (PBGC) premiums; higher user fees for spectrum, inland waterways, food safety inspection, nuclear waste, customs, and border protection; and modest increases in federal employee retirement contributions or reductions in excessive returns paid through the government “G-Fund.” The deal could also include revenue-generating energy reforms, such as selling part of the Strategic Petroleum Reserve or negotiating new leasing agreements.

Farm Subsidy Cuts ($25 billion). The 2014 farm bill made modest changes that were projected to reduce the cost of farm subsidies but resulted in little or no actual savings. The United States spends $15 billion per year on farm subsidies, and plenty of options exist to pare back these costs. Both President Trump and President Obama supported reducing crop insurance premium subsidies, streamlining conservation programs, and reducing commodity payments. In particular, President Trump produced his largest agricultural savings by limiting the amount of and income eligibility for crop insurance subsidies.

Reforms to Strengthen and Improve the SSDI Program ($25 billion). The Social Security Disability Insurance (SSDI) trust fund is projected to exhaust its reserves by 2023, at which point a roughly one-sixth across-the-board cut would occur. Meanwhile, as we explained through our SSDI Solutions Initiative, significant improvements could be made to the SSDI program to better serve those with disabilities and taxpayers. Policymakers should include a package of SSDI reforms that improve the program, support work, and ensure or improve solvency. The President’s budget includes a useful starting point for negotiating such a package. It proposes a number of modest cost-saving reforms along with investments in pilot projects to encourage attachment to the labor force over receipt of benefits. This could be supplemented with other reforms and potentially other savings and revenue options to help achieve long-term solvency.

Establish a Social Security Commission

Social Security is the largest federal government program and is responsible for over half of non-interest spending growth as a share of GDP over the next two decades. Because of the aging population, the program’s costs already exceed its dedicated revenue, and insolvency is projected by 2034 or sooner. At that point, all beneficiaries regardless of age or income would see their benefits immediately slashed by 20 to 25 percent.

Elements of our mini-bargain, including better measuring inflation and making SSDI solvent, would extend the life of the (theoretically) combined Social Security trust funds until roughly 2037 and close one-quarter to one-third of the combined solvency gap. However, a large shortfall would remain.

Time is running out to enact sensible solutions to avoid Social Security insolvency without dramatic changes, so a mini-bargain should include a process to begin negotiations over Social Security reform. We recommend the appointment of a bipartisan Social Security commission tasked with ensuring 75-year sustainable solvency for the Social Security trust funds while also promoting economic growth and improving retirement security for vulnerable populations.

The commission could be modeled after bipartisan legislation introduced by Representatives Tom Cole (R-OK) and John Delaney (D-MD) in the last Congress. If successful, Social Security solvency would reduce roughly two-fifths of the fiscal gap over the next 75 years and would also ensure predictability and financial security for tens of millions of Americans.

Increase the Debt Ceiling

The United States cannot borrow beyond its statutory debt ceiling, even to pay for past obligations and expenses. Currently, both gross federal debt and the debt ceiling itself are at $19.8 trillion, which means that action must be taken soon (likely by September or October) to avoid a debt ceiling breach. Failing to raise or suspend the debt limit would be unacceptable and potentially disastrous, leading to a default on U.S. debt and/or other obligations.

Even threatening default by coming close to the deadline could have negative consequences.

Congress should raise or suspend the debt ceiling as soon as possible and might consider coupling an increase with other debt ceiling reforms – for example, indexing the debt ceiling to GDP growth. This increase could be part of a mini-bargain on the debt.

Budget Process Reform

There is a growing consensus that the budget process is broken. Deadlines are missed, controls are circumvented, gimmicks are employed, and the long-term outlook is ignored. Both incremental and structural improvements are necessary to increase transparency, improve accountability, and focus on the long term.

A mini-bargain on the budget should take some important first steps to improve the budget process. Policymakers should look to our Better Budget Process Initiative for a wide variety of options.

Conclusion

The current fiscal situation is unsustainable, and policymakers should address it sooner rather than later. Ultimately, the country needs a major budget deal to reduce spending, secure entitlement programs, raise new revenue, and promote economic growth. Without such efforts, debt will remain on its current harrowing trajectory.

Yet the perfect should not be the enemy of the good. A mini-bargain could help avoid fiscally irresponsible tax cuts and spending increases without offsets. It could also serve as an important down payment on debt reduction.

Assuming revenue-neutral but pro-growth tax reform, a package based on the mini-bargain framework outlined above would reduce deficits by $800 billion over the next decade and reduce the debt by $4 trillion, or 10 percentage points of GDP, after twenty years. It would also set in motion an important and necessary effort to make Social Security permanently solvent.

We propose a mini-bargain that would not go as far as is needed but that would take an important step forward and avoid several steps backward. Policymakers should at least go this far to start making the country’s fiscal future much brighter.

1 Savings from Social Security should be dedicated to the Social Security trust funds, where they would improve 75-year solvency by about one-fifth. To avoid “double-counting,” some savings from Part 3 of the mini-bargain would effectively be used to offset sequester relief. Our overall estimates rely on unified budget accounting relative to CBO’s baseline, but on a net basis we do not believe trust fund savings should be used to finance general spending.