CBO's Analysis of the President's FY 2020 Budget

The Congressional Budget Office (CBO) released its estimate of the President’s Fiscal Year (FY) 2020 budget using its own assumptions to evaluate the budget’s policies. CBO’s analysis shows that deficits and debt under the President’s budget will rise over the next decade, rather than fall as the White House claims.

Our key findings from CBO’s estimates include:

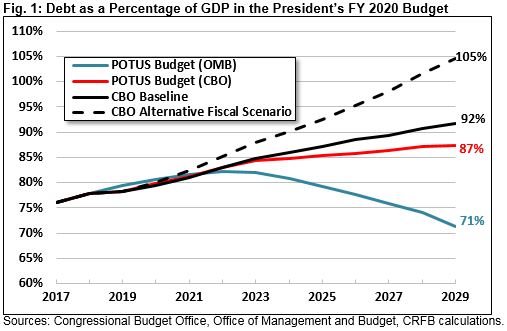

- Debt under the President’s budget would rise from 78 percent of Gross Domestic Product (GDP) today to 87 percent by 2029, rather than falling to 71 percent as the Office of Management and Budget (OMB) estimates.

- Under CBO’s estimate of the President’s budget, trillion-dollar deficits would emerge in 2022, disappear briefly, and re-emerge in 2027 and beyond.

- Deficits would total $9.9 trillion over the next decade under the President’s budget, $2.7 trillion higher than the Administration estimates.

- The President’s budget would reduce deficits by $1.5 trillion below current law over ten years, including $855 billion of policy savings. OMB estimated $2.8 trillion in total savings.

- The President’s budget would reduce revenue by nearly $900 billion and spending by $2.3 trillion relative to current law, with the largest spending cuts coming from health care and non-defense discretionary spending. Most revenue loss comes from extending parts of the 2017 tax law.

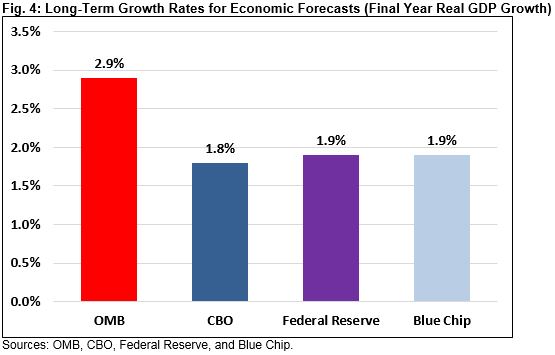

- The vast majority of the difference in debt estimates between CBO and the President is due to different economic assumptions. OMB assumes economic growth will average 2.9 percent over the next decade, whereas CBO estimates 1.8 percent. CBO’s estimates are within the mainstream of public and private estimates, whereas OMB’s are very optimistic and unlikely to materialize.

The President deserves credit for putting forward thoughtful deficit reduction in his budget, especially through changes to Medicare. Unfortunately, the budget relies too much on rosy economic assumptions and unspecified savings and uses a gimmick to circumvent the defense caps for the next two years.

Rather than counting on rapid economic growth and unspecified savings, policymakers need a specific and realistic plan to get discretionary spending under control, reform various tax breaks and spending programs, raise revenue, and put Social Security and Medicare on a sustainable long-term path.

Spending, Revenue, Deficits, and Debt under the President’s Budget

CBO estimates that debt would continue to rise over the next ten years under the President’s budget, from 78 percent of GDP today to 83 percent by 2022 and 87 percent by 2029. That is somewhat lower than the 92 percent of GDP projected under current law for 2029, but significantly higher than OMB’s own projection – which suggests debt would peak at 82 percent of GDP in 2022 before declining to 71 percent of GDP by 2029.

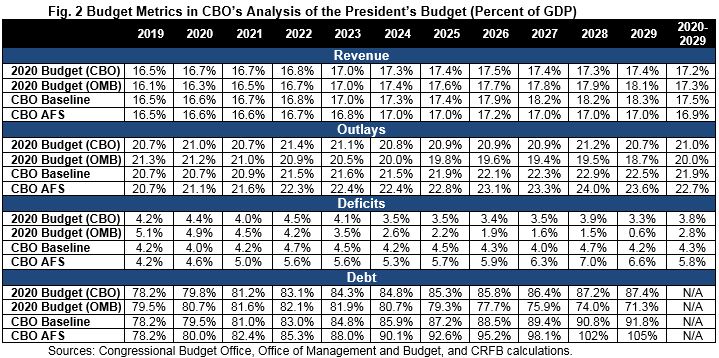

CBO finds deficits would total $9.9 trillion (3.8 percent of GDP) between 2020 and 2029, which is $1.5 trillion less than current law but $2.7 trillion higher than OMB’s estimate of the budget.

Annual deficits would rise from $779 billion in 2018 to $1.1 trillion by 2022 then remain around $1 trillion per year for the remainder of the decade. As a share of GDP, deficits would increase from 3.9 percent in 2018 to 4.5 percent in 2022 before declining to 3.3 percent by 2029. At $1.02 trillion, the deficit in 2029 would be somewhat below current law levels of $1.3 trillion (4.2 percent of GDP) but much higher than OMB’s $202 billion (0.6 percent of GDP) estimate.

Revenue under the President’s budget would rise gradually from 16.5 percent of GDP in 2018 and 2019 to 17.5 percent by 2026 and stabilize around that level, while spending would increase from 20.3 percent of GDP in 2018 to 21 percent by 2020 and would remain roughly at that level through 2029. Both spending and revenue would be significantly lower than current law, which projects revenue of 18.3 percent of GDP in 2029 and spending of 22.5 percent.

CBO estimates spending under the President’s budget would be much higher than OMB estimates as a percentage of the economy – 20.7 percent of GDP in 2029 as opposed to 18.7 percent. CBO projects that revenue would also be somewhat lower than OMB estimates – 17.4 percent of GDP in 2029 as opposed to 18.1 percent. A large share of the difference comes from OMB’s very rosy economic assumptions.

Policy Changes in the President’s Budget

The President’s budget proposes significant deficit reduction, including a number of thoughtful reforms. Unfortunately, the savings are too small to put debt on a downward path, particularly when combined with the additional tax cuts and spending in the budget.

A more complete breakdown and analysis of the proposals in the President’s FY 2020 budget can be found here.

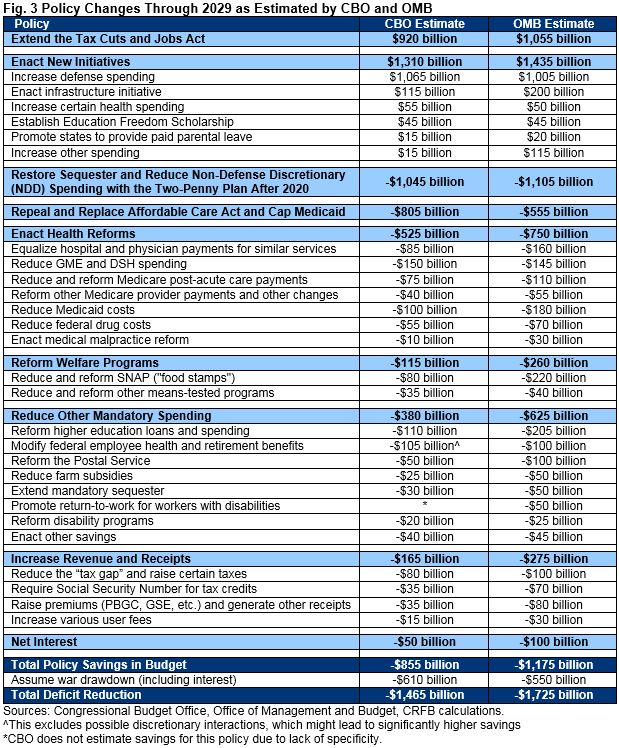

CBO estimates the budget would reduce deficits by $1.5 trillion relative to current law, including $855 billion in policy savings and $610 billion from drawing down war spending. That $855 billion is the net effect of $3 trillion of gross deficit reduction, $2.2 trillion in costs for new initiatives, and $50 billion of interest savings.

The new initiative costs come mostly from extending many expiring provisions in the 2017 tax law ($920 billion) and increasing defense spending, including $320 billion from shifting regular defense funding to Overseas Contingency Operations to get around the spending caps for 2020 and 2021. The budget also includes increased funding for infrastructure, funding and tax breaks for states to provide paid parental leave benefits, expanded Health Savings Accounts, and a new tax credit for individuals and corporations that grant scholarships.

The next largest category of savings – just over $800 billion after interactions – comes from repealing the Affordable Care Act and replacing it with state grants, while limiting the growth of Medicaid programs.

Remaining savings come from a variety of health care reforms focused on reducing excessive provider payments and drug costs ($515 billion), changes to the Supplemental Nutrition Assistance Program (SNAP) and other welfare benefits ($115 billion), reforms to the federal student loan program ($110 billion), reductions to the generosity of federal retirement benefits (at least $105 billion), improvements and reductions to disability programs, and a variety of other changes. The budget also includes a number of program integrity measures and about $165 billion in additional revenue from user fees, premiums, and taxes.

The $855 billion in policy savings is similar though somewhat smaller than OMB’s estimate of $1.2 trillion. Among deficit reduction policies – including unspecified NDD cuts – CBO’s savings estimates are somewhat lower than OMB’s estimates ($3 trillion versus $3.6 trillion).

Some of the discrepancy between CBO’s and OMB’s estimates is due to CBO disregarding unspecified savings from transforming SNAP benefits into a USDA “Harvest Box” and piloting remain-at-work and return-to-work initiatives for Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI). OMB estimated that these policies would save about $200 billion over ten years, but CBO does not score them due to lack of specificity.

In addition, CBO estimates lower savings from the Medicare provider payment changes ($120 billion less than OMB), student loan changes ($95 billion less than OMB), Government-Sponsored Enterprise (GSE) changes ($45 billion less than OMB), and farm subsidy changes ($25 billion less than OMB). On the other hand, it finds $135 billion lower costs for extending the 2017 tax law and $250 billion greater savings from the budget’s repeal and replacement of the Affordable Care Act.

Differences Between CBO and OMB Estimates

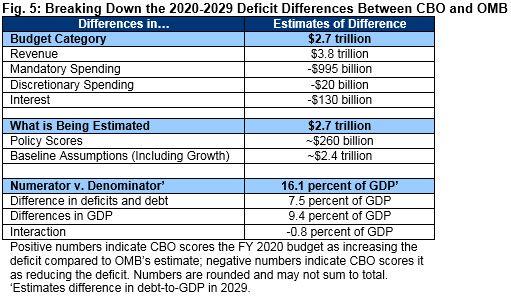

CBO’s estimates show much higher deficits and debt than OMB’s estimates. In total, CBO estimates $9.9 trillion of deficits for the President’s budget over the next decade, which is $2.7 trillion higher than OMB’s estimate. CBO estimates debt would reach 87 percent of GDP in 2029 – 16 percentage points higher than OMB’s estimate of 71 percent.

Most of the discrepancy arises from different economic assumptions. CBO projects real economic growth will average 1.8 percent over the next decade, which is in line with the projections of most public and private forecasters. Meanwhile, OMB projects that real GDP will grow by an average of 2.9 percent annually from 2020 to 2029, which is far outside of mainstream forecasts and unlikely to materialize on a sustained basis.

Because economic growth is higher under OMB’s estimates, revenues are estimated to be significantly higher; CBO estimates that revenues would be $3.8 trillion lower under its analysis of the President’s budget, which more than accounts for the $2.7 trillion difference in estimated deficits. Lower assumed spending – driven by a variety of factors – reduces the difference between OMB and CBO by $1.1 trillion.

Both on the revenue and spending side, the vast majority of the difference between CBO and OMB is due to their underlying baseline projections. While CBO believes the President’s policies will save about $260 billion less than OMB does, it also projects that baseline deficits will be $2.4 trillion higher.

It is also worth noting that focusing only on the $2.7 trillion difference in deficit projections understates the difference between CBO’s estimates and those of the Administration since it focuses on nominal deficits rather than the debt-to-GDP ratio. In total, debt-to-GDP is projected to be about 16 percentage points higher under CBO’s estimates relative to OMB’s estimates. Slightly less than half of that difference is attributable to higher projected debt, and slightly more than half is attributable to lower projected GDP growth.

Importantly, some of the difference between OMB and CBO may be due to the fact that OMB – by convention – incorporates the economic impact of the President’s budget into its estimates while CBO does not. However, based on past analyses, we find the dynamic feedback from the President’s budget to be relatively modest.

Conclusion

CBO’s analysis shows that with realistic economic assumptions, the President’s budget would not prevent the debt from rising as a share of the economy or avoid the return of trillion-dollar deficits.

To the President’s credit, his budget would result in a significant fiscal improvement relative to our current path, and his budget includes a number of thoughtful cuts and reforms. However, the budget relies too much on overly optimistic economic assumptions and unspecified spending cuts for non-defense discretionary programs as well as using a gimmick for near-term defense funding.

The spending cuts in the budget are a good starting point for deficit reduction. Lawmakers should go further than that by reforming the tax code to increase revenue, creating sustainable and gimmick-free discretionary spending caps, and including more savings from mandatory programs.