CBO's 2018 Long-Term Budget Outlook

The Congressional Budget Office (CBO) released its 2018 Long-Term Budget Outlook today, reiterating the budget’s unsustainable long-term trajectory. CBO projects debt held by the public will reach a new record as a share of the economy within 16 years, and will double its current levels within three decades.

If recent tax cuts and spending increases are extended rather than allowed to expire, we estimate debt would be double the size of the economy within three decades.

The report shows:

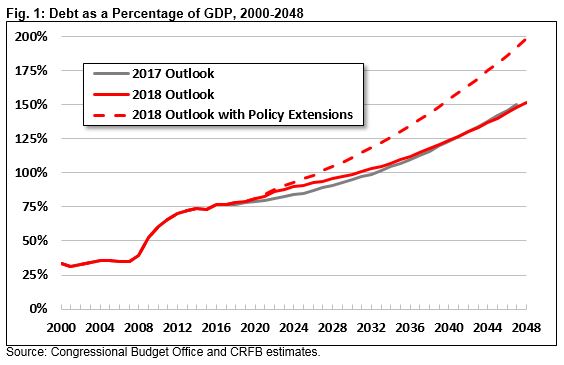

- Debt Is Rising Unsustainably. CBO projects debt held by the public will roughly double as a share of the economy under current law, from 78 percent of GDP at the end of 2018 to 152 percent of GDP in 2048 – an unprecedented level.

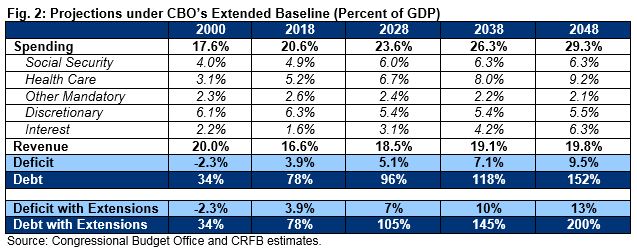

- Spending Is Growing Faster Than Revenue. CBO projects spending will grow rapidly, from less than 21 percent of GDP in 2018 to over 29 percent by 2048. Revenue will grow slowly, from less than 17 percent of GDP in 2018 to nearly 20 percent of GDP. As a result, annual deficits grow from 3.9 percent of GDP in 2018 to 9.5 percent by 2048, approaching the post-World War II record set in 2009.

- Recent Legislation Will Substantially Worsen the Long-Term Outlook if Extended. Because the unpaid-for 2017 tax law and 2018 spending deal were largely temporary, they have little effect on CBO’s long-term debt estimates under current law. We estimate debt would be about 50 percent of GDP higher in 2048 – roughly 200 percent of GDP – if temporary provisions were extended.

- High And Rising Debt Will Have Adverse and Potentially Dangerous Consequences. The fiscal situation will lead to slower economic growth, lower income, higher interest rates, ballooning interest payments, reduced fiscal space, weakened international leadership, and an increased likelihood of a fiscal crisis.

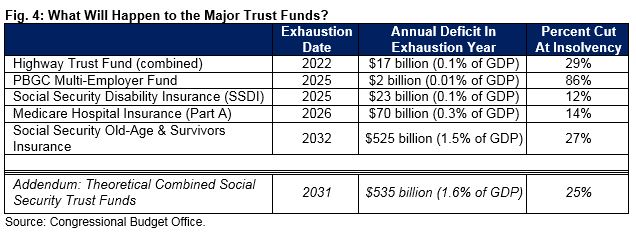

- Major Trust Funds Are Headed Toward Insolvency. CBO projects the Highway, PBGC Multi-Employer, Social Security Disability Insurance, Social Security Old-Age and Survivors Insurance, and Medicare Hospital Insurance trust funds will all be exhausted by 2032 without action to stabilize their finances.

- Fixing the Debt Will Get Harder the Longer Policymakers Wait. Delaying necessary deficit reduction will mean larger spending cuts and tax increases concentrated on fewer people. CBO estimates the size of the needed adjustment would grow by half if policymakers waited just ten years to take action.

Lawmakers need to work together to address this bleak fiscal picture now so problems do not compound any further.

Debt Is Rising Unsustainably

Debt held by the public will total 78 percent of the economy by the end of 2018 – a post-war record nearly twice as high as historic averages – and will grow rapidly from there with no end in sight.

Under current law, CBO projects debt will exceed the size of the economy by 2031, top its record high by 2034, and reach nearly double today’s level at 152 percent of GDP within three decades.

Annual deficits will also grow rapidly under CBO’s projections. Under current law, the deficit will double from 3.9 percent of GDP in 2018 to 7.8 percent by 2041 and reach 9.5 percent by 2048 – near the post-war record of 9.8 percent set at the height of the Great Recession.

These numbers assume recent tax cuts and spending increases expire as under current law. If they are extended, we estimate debt will exceed the size of the economy by 2027, hit a new record by 2029, and double the size of the economy by 2048.1

In 2048 under this scenario, debt will total 200 percent of GDP and deficits will exceed 13 percent of GDP. There is little precedent for this massive level of debt.

These debt projections are modestly higher than estimates from the Government Accountability Office (GAO) that debt will reach 138 to 194 percent of GDP by 2048.

Spending Is Growing Faster Than Revenue

Rising long-term deficits are driven by rapid growth in spending – particularly spending on health care, retirement, and interest on the debt – well in excess of the growth in revenue.

CBO projects revenue will rise from 16.6 percent of GDP in 2018 to 18.5 percent in 2028 and 19.8 percent in 2048. This compares to a 50-year historical average of 17.4 percent and record of 20.0 percent in 2000. Spending, meanwhile, will grow from 20.6 percent of GDP in 2018 to 29.3 percent by 2048 under current law. By comparison, spending has averaged 20.3 percent of GDP over the past 50 years, and peaked at 24.4 percent of GDP in 2009.

Much of the projected revenue growth is due to the expiration of many provisions in the Tax Cuts and Jobs Act, as well as the use of “chained CPI” for indexing the tax code and the scheduled implementation of the health care ”Cadillac Tax” in 2022.

CBO’s projections for spending, meanwhile, reflect the continued aging of the population, rising health care spending, and rising interest rates and debt. In fact, spending on Social Security, health care, and interest on the debt explain all future spending growth as a share of the economy; combined spending will rise by roughly 10 percent of GDP, from 11.7 percent of GDP in 2018 to 21.8 percent by 2048.

By 2041, spending on Social Security, health care, and interest will exceed all revenue. That essentially means every dollar Congress appropriates – whether for defense, education, or basic research – will be financed with borrowed money. By 2050, interest will be the single largest federal spending program, eclipsing Social Security, Medicare, and all discretionary spending.

If expiring tax cuts and recent spending increases were continued, revenue would be much lower and spending much higher. Roughly speaking, revenue would reach 18 percent of GDP and spending nearly 32 percent of GDP by 2048. In this scenario, spending on Social Security, health care, and interest will exceed all revenue by 2033 – eight years earlier than under current law – and interest would be the largest spending program by 2042.

Recent Legislation Will Substantially Worsen the Long-Term Outlook if Extended

Recent tax cuts and spending increases have significantly worsened the budget outlook over the next decade and would substantially worsen the longer-term outlook if extended.

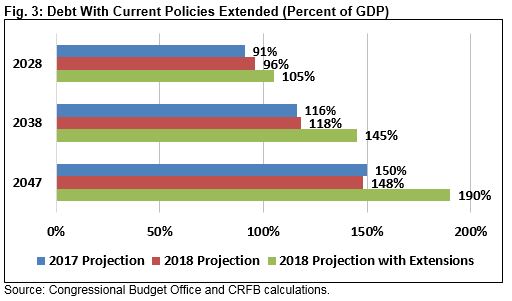

CBO currently projects that debt will reach 96 percent of GDP by 2028, which is 5 percentage points and $2.2 trillion higher than they projected last March. Nearly $2 trillion of this difference is the result of the deficit-financed Tax Cuts and Jobs Act (TCJA) and another half-trillion is due to the direct spending increase in the Bipartisan Budget Act (BBA) and other legislative changes.

Because large parts of the TCJA and BBA expire under current law and the permanent parts modestly reduce deficits, this year’s projections begin to converge with last year’s over time. Last year, CBO projected debt would reach 150 percent of GDP by 2047, compared to 148 percent this year. The 2047 deficit was 9.8 percent of GDP last year, compared to 9.3 percent this year.

We estimate that if expiring policies are continued, debt will be almost one-third worse than last year’s projections. Specifically, debt would rise to more than 190 percent of GDP by 2047 (nearly 200 percent by 2048), compared to last year’s current law projections of 150 percent of GDP in 2047. Deficits would rise to above 13 percent of GDP by 2047.

The rise in debt under this scenario is the result of both higher spending and lower revenue. Non-interest spending would total about 23.5 percent of GDP in 2047, compared to CBO’s previous projections of 23.2 percent. Revenue, meanwhile, would exceed 18 percent of GDP, compared to CBO’s previous projections of 19.6 percent. Interest would grow to nearly 8 percent of GDP, compared to 6.2 percent under last year’s projections.

In other words, recent legislation considerably increased the debt and would dramatically worsen the long-term budget outlook if policymakers extend them without offsets.

High and Rising Debt Will Have Adverse and Potentially Dangerous Consequences

The United States has never owed as much debt as it is projected to owe by the 2030s. CBO warns that such high and rising debt could have dramatic adverse consequences.

Rising debt is likely to substantially slow economic growth and reduce future incomes by leading savers and investors to purchase Treasury bonds in place of productive investments.

CBO’s projections of GNP per capita show that in three decades, currently projected rising debt will reduce average income by about 3 percent – roughly $3,000 per person. Assuming various tax cuts and spending hikes are extended and debt grows by an extra 50 percent of GDP, income could be as much 6 percent or $6,000 lower by our estimate (based on last year’s report).

Rising debt also causes interest rates to rise. CBO estimates average rates on federal debt will be 13 percent, or 50 basis points, higher as a result of rising debt. These higher rates will spill over into mortgages, car loans, student loans, business loans, and credit card debt.

As a result of higher interest rates and higher debt, government interest payments will grow. Under current law, interest payments will almost quadruple from 1.6 percent of GDP this year to 6.3 percent by 2048, exceeding the size of Medicaid in 2020, defense in 2023, and Medicare in 2046, Interest will become the largest spending program by exceeding Social Security after 2048. If Congress extended various expiring policies, we estimate that interest costs would more than quintuple to 8.1 percent of GDP by 2048, becoming the largest government program by 2042.

Growing interest payments and rising debt could weaken U.S. international leadership and mean less fiscal space to protect the country, make important investments, fund new priorities, or respond to the next recession, crisis, or emergency. CBO explains that “when outstanding debt is relatively small, the federal government is able to borrow money at lower rates to cover unexpected costs, such as those that arise from recessions, financial crises, natural disasters, or wars. By contrast, when outstanding debt is large, the government has less flexibility to address financial and economic crises.“

Finally, growing levels of debt increase the risk of fiscal crisis. As CBO warns, “dramatic increases in Treasury rates would reduce the market value of outstanding government securities, and the resulting losses—for mutual funds, pension funds, insurance companies, banks, and other holders of government debt—could be large enough to cause some financial institutions to fail.” Such a crisis would cause substantial damage to the U.S. and global economy and leave policymakers with “limited—and unappealing—options.”

While growing debt would damage the economy, declining debt can improve it. In previous reports, CBO showed that a $4 trillion deficit reduction package would boost average incomes by $5,000 per person and lower interest rates by three-quarters of a percentage point over the long term.

All of the Major Trust Funds Are Headed Toward Insolvency

A number of important federal programs are financed through trust funds. Within the next 14 years, CBO projects five major trust funds will exhaust their reserves and become insolvent.

Specifically, CBO projects the Highway Trust Fund will be depleted by 2022, the Pension Benefit Guaranty Corporation (PBGC) multi-employer fund and Social Security Disability Insurance (SSDI) Trust Fund by 2025, the Medicare Hospital Insurance (HI) Trust Fund by 2026, and the Social Security Old-Age and Survivors Insurance Trust Fund by 2032. On a combined basis, the Social Security trust funds will run out of reserves in 2031.

At the time of insolvency, the law requires spending be reduced to available revenue in these programs. CBO estimates Social Security benefits, for example, would be abruptly cut by 25 percent for all beneficiaries regardless of age or income. Medicare’s cut would likely total about 14 percent.

Importantly, CBO’s debt projections assume that these programs (other than PBGC) will continue to spend even after trust funds are exhausted. If policymakers wish to maintain the internally-funded nature of these programs, however, substantial adjustments will be needed.

CBO estimates Social Security’s shortfall will total 1.5 percent of GDP over 75 years and 1.9 percent of GDP in the 75th year. Making the program solvent would require the equivalent of a 35 percent (4.4 percentage point) increase in the payroll tax rate or a 25 percent cut in benefits. Maintaining sustainable solvency beyond 75 years would require the equivalent of an ultimate 38 percent (6 percentage point) increase in the payroll tax rate or a 30 percent cut in benefits.

A Social Security solvency package could reduce projected debt by between 30 and 50 percentage points by 2048, depending on the plan’s design. If the shortfalls in other trust funds were also addressed, debt could be stabilized well below 100 percent of GDP and perhaps at today’s levels. In addition, solvency plans would ensure these programs could continue to provide benefits and payments to those who rely on them.

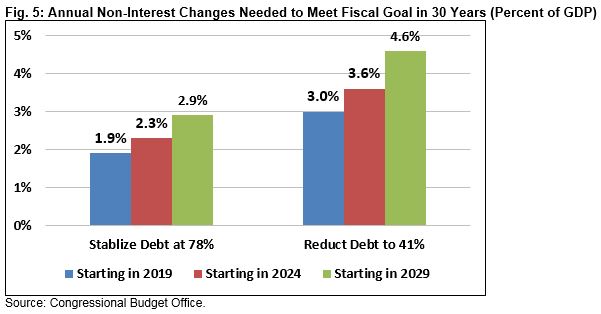

Fixing the Debt Will Get Harder the Longer We Wait

Policymakers will need to make tough decisions on changes to spending and revenue in order to put the debt on a downward path. But more importantly, they need to do them soon; the longer they wait, the harder and costlier the necessary adjustments will be.

CBO projects that maintaining today’s high debt as a share of the economy for the next 30 years will require annual tax or spending adjustments (excluding interest) of 1.9 percent of GDP if they start in 2019 – the equivalent of $4.8 trillion over a decade. Waiting another ten years would make this even more expensive, to the tune of 2.9 percent of GDP, the equivalent of $7.3 trillion over the same decade.2 In other words, the cost would increase by half.

Thought of another way, policymakers could raise revenue 11 percent or cut non-interest spending 10 percent to stabilize the debt if they begin today – but would have to raise revenue by 17 percent or cut non-interest spending by 15 percent if they wait just a decade to begin acting. Putting the debt on a downward path would require even larger savings. Reducing debt to its 50-year historical average of 41 percent of GDP would require adjustments of 3.0 percent of GDP today ($7.6 trillion) or 4.6 percent of GDP ($11.6 trillion) if they waited another decade to enact these changes.

Delaying actions to fix the debt also allows less time to carefully phase in changes and allow households and businesses to prepare for them. In addition, waiting requires concentrating any spending cuts or tax hikes on fewer people and reduces the ability of policymakers to make smart targeted reforms that protect more vulnerable beneficiaries and taxpayers. At some point, needed changes may become so drastic that policymakers are unwilling to act, absent a crisis.

Conclusion

CBO continues to remind us what we’ve known for a while and seem to be ignoring: the federal budget is on an unsustainable course, particularly over the long term. If policymakers make the tough decisions now – rather than wait until there’s a crisis point for action – the solutions will be fairer and less painful.

With debt on course to double its current levels and quadruple its historic average, lawmakers need to stop making it worse. That means making affordable and paying for any extensions to the recent tax cuts and spending increases to prevent debt from rising to twice the size of the economy within three decades. We cannot afford to make these temporary policies permanent without making choices to pay for them and enact actual deficit reduction.

CBO’s projections of the budget and economy reiterate the fundamental challenges we face: the population is aging – which means rising costs of Social Security and Medicare as well as slower economic growth.

There is no magic bullet to fix these problems. Ignoring CBO’s impartial projections, which are consistent with nearly every other estimator, will not make the problem go away. Indeed, it will make the problem worse as a result of the high cost of delay.

The gap between spending and revenue is only getting larger, the burden of our debt is growing rapidly, and major trust funds – including for Social Security and Medicare – are headed toward insolvency.

Smart deficit reduction enacted today can accelerate economic growth, stem the rise in interest rates, increase future incomes, secure the solvency of Social Security and other trust funds, improve generational fairness, create fiscal space, and prevent a potential fiscal crisis.

Action needs to start yesterday.

1 This projection extends CBO’s April Alternative Fiscal Scenario, which assumes lawmakers extend the BBA cap adjustments, normalize disaster spending, continue expensing of equipment, extend expiring invividual and estate tax provisions from the TCJA, and continue various other tax provisions.

2 These numbers are calculated based on the 2019-2028 window for a direct comparison, even though cuts would not actually begin until 2029.

What's Next

-

-

Image

-

Image