Analysis of the 2017 Social Security Trustees Report

The Social Security and Medicare Trustees today released their annual reports on the financial status of the two programs. The projections show that both programs continue to face large funding gaps that will only grow over time. This year’s report on Social Security shows that:

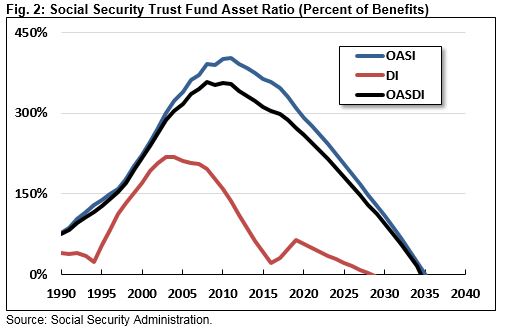

- Social Security is Heading Toward Insolvency. On a theoretical combined basis, the Old-Age, Survivors, and Disability Insurance (OASDI) trust funds face a 75-year shortfall of 2.83 percent of taxable payroll (1.01 percent of Gross Domestic Product) and are projected to be insolvent by 2034 (2028 for Disability Insurance; 2035 for Old-Age and Survivors Insurance).

- Social Security’s Deficits are Large and Growing. Social Security will pay out $27 billion more in benefits than it will generate in tax revenue this year, and cash-flow deficits over the next decade will total $1.4 trillion. Annual deficits will grow to 3.77 percent of payroll (1.36 percent of GDP) by 2037 and 4.48 percent of payroll (1.54 percent of GDP) by 2091.

- Action is Still Needed on SSDI. Despite a temporary “reallocation” of payroll tax revenue, the Trustees project the Disability Insurance (SSDI) trust fund will run out of reserves by 2028. A number of smart reform options are available to both avert SSDI insolvency and improve the program for current and potential beneficiaries.

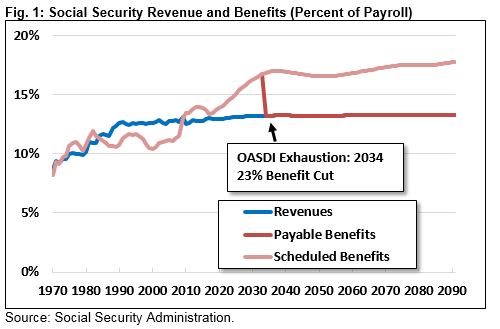

- Failure to Act Will Lead to Large, Abrupt Benefit Cuts. Assuming continued reallocations, all Social Security beneficiaries – regardless of age or income – are projected to face a 23 percent benefit cut in 2034, when today’s 50-year-olds reach the normal retirement age and today’s youngest retirees turn 79. Cuts would grow over time, reaching 27 percent by 2091.

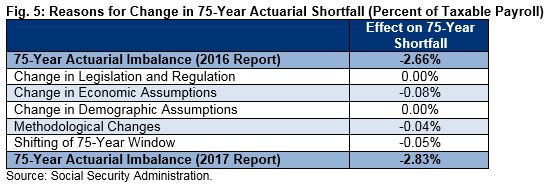

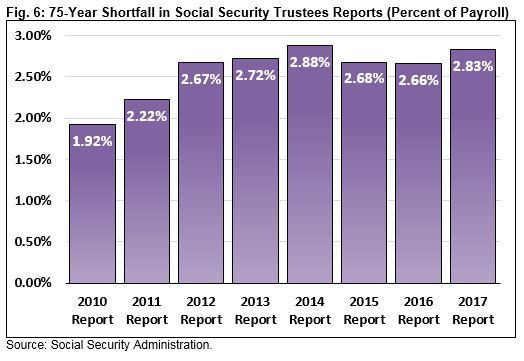

- The Trustees Project a Larger Shortfall. Overall, this year’s report represents a slight deterioration over last year’s, which showed the same combined trust fund exhaustion date of 2034 but a 75-year actuarial imbalance of 2.66 percent of payroll (0.17 percentage points lower than this year). The current shortfall is now roughly 47 percent larger than the 1.92 percent shortfall estimated in 2010.

With many baby boomers already in retirement and only 17 years until insolvency, time is running out to make thoughtful reforms to the program. Policymakers should act soon and put all options on the table to make Social Security solvent.

Social Security Projections

The Social Security Trustees continue to warn that the program is financially unsound. They project the combined Old-Age and Survivors Insurance (OASI) and Disability Insurance (SSDI) programs to run cash-flow deficits for the foreseeable future. This year, those deficits total about $27 billion, which is 0.4 percent of taxable payroll and 0.1 percent of GDP. They are projected to reach 2.5 percent of payroll (0.9 percent of GDP) by 2027, 3.7 percent of payroll (1.3 percent of GDP) by 2040, and 4.5 percent of payroll (1.5 percent of GDP) by 2091.

Over the next ten years (2018-2027), Social Security will run deficits totaling $1.4 trillion, according to the Trustees. In the following decade, deficits will total $4.9 trillion.

Over the next 75 years, Social Security’s actuarial imbalance – the present value of the program’s 75-year trust fund shortfall – is estimated to equal 2.83 percent of payroll (1.01 percent of GDP). On a present value basis, the program’s 75-year unfunded obligation totals $12.5 trillion.

The program’s funding shortfall is the result of a growing gap between Social Security’s benefit costs and its dedicated tax revenues. As the number of Social Security beneficiaries continues to increase, outlays have already risen from 10.4 percent of payroll (4.0 percent of GDP) in 2000 to 13.4 percent of payroll (4.9 percent of GDP) today. The Trustees project they will continue to grow to 17 percent of payroll (6.1 percent of GDP) by 2040, dip slightly, and then grow to 17.8 percent of payroll (6.1 percent of GDP) by 2091.

Meanwhile, revenues will fail to keep up – growing slightly as a percent of payroll from 13 percent today to 13.3 percent in 2091, while actually falling slightly as a percent of GDP after the 2020s from 4.8 percent in 2030 to 4.6 percent by 2091.

As benefit costs continue to exceed dedicated revenue, the Social Security trust funds are projected to run out of reserves. The Trustees project the OASI trust fund to be exhausted in 2035, and the SSDI trust fund is expected to deplete its reserves in 2028. On a combined basis, the OASDI trust fund would run out of reserves by 2034, when today’s 50-year-olds reach the normal retirement age and today’s youngest retirees turn 79.

The Cost of Waiting

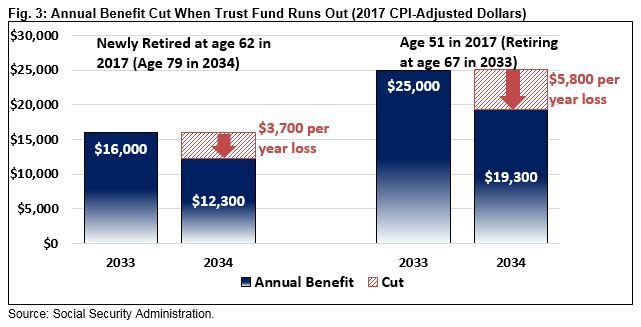

When the OASDI trust fund is exhausted, beneficiaries will face an across-the-board 23 percent benefit cut, the equivalent of about $5,800 per year in today’s dollars for a typical beneficiary reaching the full retirement age in 2033. This cut would be immediate and would affect all beneficiaries regardless of age, income, health or wellbeing. The size of the cut would also grow over time, reaching 27 percent by 2091.

Avoiding these abrupt cuts and making Social Security solvent would require the equivalent of immediately raising the Social Security payroll taxes by 22 percent, from 12.4 to about 15.2 percent of payroll; reducing benefits for all current and future beneficiaries by about 17 percent; reducing benefits for all new beneficiaries by 20 percent; or some combination of the three.

The necessary benefit cuts or tax increases only become larger the longer that policymakers delay action. If policymakers wait until 2034 to make any changes, they will have to increase the payroll tax by 32 percent (to 16.4 percent) or cut benefits for all new and existing beneficiaries by 23 percent to attain solvency, and even eliminating benefits for new beneficiaries would not be enough to avoid insolvency. A much smarter course of action would begin changes much earlier so they can be spread among more generations and phased in more gradually with more warning to affected beneficiaries.

Importantly, even with an immediate payroll tax increase large enough to make the program solvent, cash-flow deficits would return by 2029 – meaning further changes would be necessary to make the program sustainable over the long term. That is why policymakers should look beyond simply keeping the program solvent for 75 years and pursue “sustainable solvency,” which ensures the program raises about as much as it pays out over the long run.

Social Security Disability Insurance Projections

While the projected depletion of the combined OASDI program highlights the need for action to reform Social Security sooner rather than later, the Social Security Disability Insurance (SSDI) program faces an even more immediate problem. The Trustees project the insolvency of this fund by 2028, only 11 years from today.

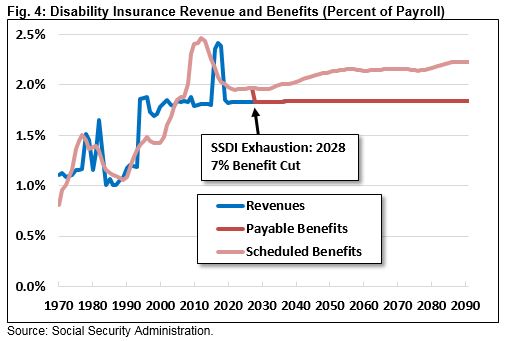

Spending on SSDI has increased significantly in recent years, from less than 1.1 percent of payroll in 1990 to 2.08 percent today. The Trustees project SSDI costs will subside in the coming years due to recent low levels of benefit awards and the aging of the baby boom generation on to the larger OASI program but will rise again after 2032 and reach 2.23 percent of payroll by 2091.

Generally, the SSDI program is financed with a 1.8 percent payroll tax that is insufficient to cover its costs. In 2015, Congress temporarily reallocated funds from the old-age trust fund, effectively increasing the SSDI payroll tax from 1.8 percent to 2.37 percent (and reducing the OASI payroll tax from 10.6 to 10.03). However, this reallocation will end in 2019, after which cash deficits will return to SSDI. In fact, the Trustees estimate SSDI will face cash deficits of $13 billion in 2020 and $91 billion over the next decade.

By 2028, the Trustees project these deficits will exhaust the SSDI trust fund, and without legislative action all disability beneficiaries would face an immediate 7 percent across-the-board cut. By 2091, the cut would grow to 18 percent.

Policymakers should take action promptly to rescue the SSDI program from insolvency, and they should also use the opportunity to make thoughtful improvements to the program – improvements that can benefit the program’s current and potential beneficiaries, those who contribute to the program, and society at large.

The Bipartisan Budget Act of 2015 took some important first steps by strengthening anti-fraud protections, improving the consistency of the determination process, and allowing for new return-to-work pilots; however, much more needs to be done. The determination process should be improved to shorten processing times, reduce the large hearings backlog, and increase uniformity in decision-making. Certain eligibility rules could also be revisited, including the medical-vocational guidelines that inform eligibility decisions. Those guidelines have not been significantly updated since they were introduced almost 40 years ago. Much more can be done to promote early intervention and help potential SSDI beneficiaries remain in the workforce.

While policymakers could delay SSDI’s impending insolvency through another reallocation from the old-age fund, further delaying substantive reforms would represent a missed opportunity.

Instead, Congress and the President should use the next 11 years to identify, develop, and implement policies that both strengthen the solvency of SSDI and improve its effectiveness in supporting workers with disabling health conditions. For example, President Trump’s budget proposes several reforms to improve SSDI’s solvency as well as a number of demonstration projects aimed at keeping SSDI beneficiaries in the labor force, including several proposals put forward by the McCrery-Pomeroy SSDI Solutions Initiative.

Changes in Projections

The Social Security Trustees project a slightly more pessimistic outlook relative to last year’s report. Specifically, the Trustees project no change in the theoretical combined trust fund exhaustion date of 2034 but larger deficits throughout the projection window and a 75-year actuarial shortfall of 2.83 percent of payroll (1.01 percent of GDP) as opposed to 2.66 percent of payroll (0.95 percent of GDP) last year.

The largest contributor to these changes comes from more pessimistic economic assumptions. Specifically, the Trustees now expect slower real wage growth in both the short and long terms due to faster growth in health insurance premiums, meaning employees will receive a larger share of compensation in the form of health insurance rather than taxable wages. In addition, this year’s report assumes a weaker recovery from the recent recession and as a result a permanently lower level of labor productivity.

Methodological changes also contribute to the larger shortfall projection. These include improvements in the Trustees’ method for estimating the number of workers insured for Social Security, the age at which older workers claim retirement benefits as life expectancy improves, and the effects of benefit offsets for individuals with pensions from jobs that are not covered by Social Security.

Changes in demographic assumptions roughly offset each other. The Trustees now assume the currently low levels of SSDI applications and awards will continue in the near term, improving the program’s finances. As a result, SSDI’s exhaustion date is pushed back 5 years from 2023 in last year’s report to 2028. However, these and other improvements are offset by other more pessimistic projections of fertility rates and immigration.

As a result of these changes, the Trustees now project a shortfall that is the largest since the 2014 report and is about 47 percent larger than the one projected in 2010.

Conclusion

The Social Security Trustees continue to underscore the need to address Social Security’s financing shortfall soon. Failure to act would result in all beneficiaries receiving a 23 percent across-the-board benefit cut when the combined trust fund exhausts in just 17 years, when today’s 50-year-olds reach the normal retirement age. The SSDI program faces an even more immediate deadline and will deplete its trust fund in 2028.

Policymakers can still address Social Security’s financial problem without making drastic tax or benefit changes, but the window for responsible action is closing. If policymakers are willing to act soon, they can create a plan that strengthens the program’s finances while phasing in changes gradually to give workers time to plan, improving retirement security for vulnerable beneficiaries and promoting long-term economic growth. However, the cost of delay is substantial, and waiting to address the problem limits policymakers’ ability to enact more gradual and targeted reforms. As the Trustees explain:

If actions are deferred for several years, the changes necessary to maintain Social Security become concentrated on fewer years and fewer generations…

The Trustees recommend that lawmakers address the projected trust fund shortfalls in a timely way in order to phase in necessary changes gradually and give workers and beneficiaries time to adjust to them. Implementing changes sooner rather than later would allow more generations to share in the needed revenue increases or reductions in scheduled benefits and could preserve more trust fund reserves to help finance future benefits.

Policymakers must act quickly to put Social Security on a path toward sustainable solvency. As time goes on, it will be more difficult to secure the Social Security programs for current and future generations with thoughtful changes instead of abrupt benefit cuts or tax increases.