Analysis of the 2016 Social Security Trustees Report

Today, the Social Security and Medicare Trustees released their annual reports on the financial status of each program. The projections show that both programs are in dangerous fiscal positions and prompt action is necessary to secure these programs.

This analysis focuses specifically on the Social Security Trustees report. Based on that report, this analysis finds:

- Social Security is Heading Toward Insolvency. On a theoretical combined basis, the Social Security trust funds face a 75-year gap of 2.66 percent of payroll (0.95 percent of GDP) and are projected to be insolvent by 2034 (2023 for Disability Insurance, 2035 for Old Age and Survivors’ Insurance). The 75-year present value of the shortfall is $11.4 trillion.

- Social Security’s Deficits are Large and Growing. Social Security’s shortfall will total $1.4 trillion over the next decade, which is 1.55 percent of payroll or 0.56 percent of GDP. The gap will grow to 3.36 percent of payroll (1.21 percent of GDP) by 2040 and 4.35 percent of payroll (1.51 percent of GDP) by 2090.

- The Shortfall is the Same as Last Year, Despite a Short-Term SSDI Fix. Security Security’s 75-year shortfall 0.02 percent of payroll smaller than last year’s estimate, an improvement of less than 1 percent. However, lawmakers did delay the insolvency of the disability program from 2016 to 2023 by reallocating revenue from the old-age program last year.

- Failure to Act Will Lead to Large, Abrupt Benefit Cuts. In 2034 – when today’s 49 year-olds reach the normal retirement age and today’s youngest retirees turn 80 – all beneficiaries are projected to face a 21 percent across-the-board benefit cut. For a typical newly-retired couple in 2033, that would mean a $10,300 immediate cut in annual benefits the following year.

- The Latest Projections Highlight the Need to Focus on Solvency First. Fixing Social Security will likely require both slowing the growth of benefits and increasing revenue. Proposals to expand benefits for all seniors move in the wrong direction. Just a $100 increase in average monthly benefits would cost $1.2 trillion over a decade and worsen the program’s shortfall by 50 percent.

Social Security is Heading Toward Insolvency

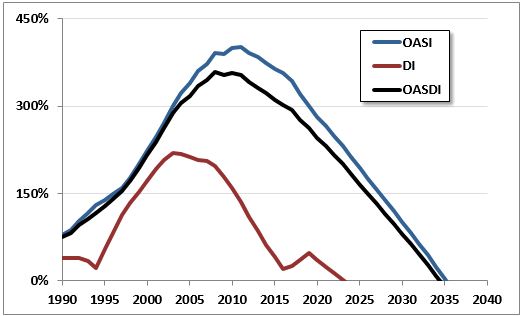

The Social Security program is running large deficits that are quickly depleting its trust funds. According to the Trustees, the Social Security Disability Insurance (SSDI) trust fund will run out of reserves by 2023, while the Old Age and Survivors’ Insurance (OASI) trust fund will run dry by 2035. On a theoretical combined basis, Social Security will be insolvent by 2034.

When the Social Security trust funds are exhausted in 2034, beneficiaries will face an immediate across-the-board 21 percent benefit cut. The size of the cut will grow over time, to 26 percent by 2090.

Fig. 1: Social Security Trust Fund Asset Ratio (Percent of Annual Benefits)

Source: Social Security Administration

Avoiding insolvency will require significant changes in benefits, revenue, or both.

Over 75 years, the Trustees project an actuarial imbalance of 2.66 percent of payroll (0.95 percent of GDP) – the equivalent of $11.4 trillion on a present-value basis. Closing this shortfall would therefore require increasing payroll taxes by 21 percent (increasing the rate from 12.4 to 15 percent), reducing benefits for all current and future beneficiaries by about 16 percent, reducing benefits for only new beneficiaries by 19 percent, or some combination.

To keep the program sustainably solvent over the long-run would eventually require even larger adjustments. In 2090, the shortfall is projected to total 4.35 percent of payroll (1.51 percent of GDP), meaning eventual adjustments will need to total a 35 percent increase in taxes (increasing the payroll tax from 12.4 to 16.8), a 26 percent reduction in benefits, or some combination of tax increases and benefit reductions.

Social Security's Deficits Are Large and Growing

Social Security will pay out $73 billion more in benefits than it will generate in revenue this year, and $1.4 trillion more over a decade, according to the Trustees. This shortfall will grow dramatically as the baby boomers continue to retire and life expectancy rises.

As a percent of payroll, the Trustees project Social Security’s deficit to grow from 1.1 percent today to 2.34 percent in a decade, 3.36 percent by 2040, and 4.35 percent by 2090. As a share of GDP, it will grow from 0.4 percent this year to 1.5 percent by 2090. This 2090 shortfall is the equivalent of nearly $4 trillion over the next decade.

These growing deficits result from the divergence between Social Security benefits and revenues. As the number of beneficiaries in the program continues to grow, outlays have already increased from 10.4 percent of payroll (4.0 percent of GDP) in 2000 to 14.1 percent of payroll (5.0 percent of GDP) in 2016. The Trustees project they will continue to grow to 16.6 percent of payroll (6.0 percent of GDP) by 2040, dip slightly over the subsequent decade, then resume growing to 17.7 percent of payroll (6.1 percent of GDP) by 2090.

Meanwhile, revenues will fail to keep up – growing only a small amount as a percent of payroll from 12.9 percent in 2016 to 13.3 percent in 2090, while actually falling slightly as a percent of GDP after the 2020s from 4.8 percent in 2030 to 4.6 percent by 2090.

Fig. 2: Social Security Revenue and Benefits (Percent of Payroll)

Source: Social Security Administration

The Shortfall is the Same as Last Year, Despite a Short-Term SSDI Fix

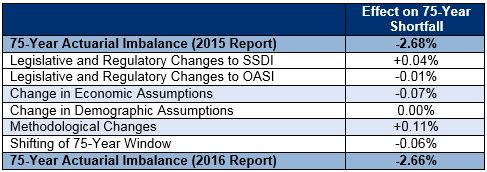

The Social Security Trustees project a 75-year shortfall that is essentially unchanged from last year’s report. Specifically, they estimate a 75-year shortfall that is less than 1 percent smaller (2.66 versus 2.68 percent of payroll) and a 75th year shortfall that is 6 percent smaller (4.35 versus 4.65 percent). The projected exhaustion date remains 2034.

The largest contributors to the improvement in the 75-year shortfall are methodological changes, particularly improvements in the Trustees’ methods used to project immigration. Legislative changes, almost entirely from the Bipartisan Budget Act of 2015 (BBA) – which temporarily avoided insolvency of the SSDI program and included other small changes to Social Security – also improved the outlook by 0.03 percent of payroll. These improvements are partially offset by updated assumptions for inflation, real wage growth, and interest rates, and by shifting the 75-year window.

Fig. 3: Reasons for Change in 75-Year Actuarial Shortfall (Percent of Taxable Payroll)

Source: Social Security Administration

The new report includes an improved outlook for the disability program (a 75-year shortfall of 0.26 instead of 0.31 percent) and a worsened outlook for the old-age program (a 75-year shortfall of 2.39 instead of 2.37 percent). Last year’s BBA improved the financial condition of the retirement program by 0.02 percent of payroll and the disability program by 0.01 percent of payroll through reforms, while also reallocating 0.03 percent of payroll in revenue from the old-age program to the disability program (increasing the old-age program’s shortfall while reducing the disability program’s shortfall).

As a result of this reallocation from the old-age program, the BBA extended the insolvency date of the SSDI program from 2016 to 2023, giving lawmakers a 7-year reprieve to develop and identify improvements both to the SSDI program’s financial status but also its effectiveness in serving disabled workers. The McCrery-Pomeroy SSDI Solutions Initiative has published SSDI Solutions: Ideas to Strengthen the Social Security Disability Insurance Program, a book with numerous innovative proposals to reform the SSDI system and extend its solvency. These ideas and others should be discussed well ahead of the 2023 deadline so that they can make a difference in improving the SSDI program.

Failure to Act Will Lead to Large, Abrupt Benefit Cuts

The most popular approach to Social Security reform in Washington currently appears to be the “do nothing plan.” Continuing this approach could have severe consequences.

Social Security’s trust funds are projected to run out of money in 2034, when today’s 49 year-olds reach the full retirement age and today’s newest retirees turn 80. Delaying action until we near that deadline will make the problem bigger and harder to solve. For example, earlier this year we estimated 75-year solvency could be achieved by raising taxes or cutting new benefits by about-one fifth, but delaying just ten years would increase the necessary tax increase to 27 percent and the necessary cut in new benefits to 33 percent.

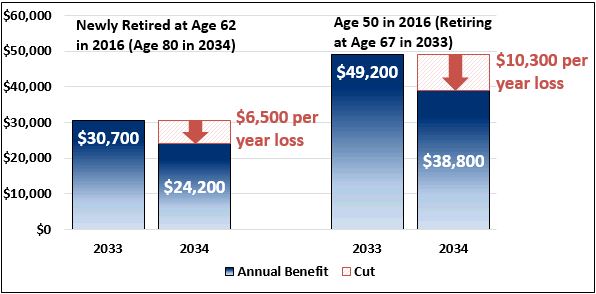

Failing to act at all would be even worse than delay. Without a solvency package, the exhaustion of the combined trust funds in 2034 will lead to the equivalent of a 21 percent immediate across-the-board benefit cut for all beneficiaries.

For a typical 50-year-old couple today who retires at the full retirement age, annual benefits would fall from $49,200 in 2033 (in 2016 CPI-adjusted dollars) to $38,800 in 2034 – a cut of more than $10,000 per year. Similarly, a typical newly-retired couple today who turns 80 in 2034 will have their annual benefit fall by $6,500, from $30,700 to $24,200.

Fig. 4: Annual Benefit Cut When Trust Fund Runs Out (2016 CPI-Adjusted Dollars)

Source: Social Security Administration, CRFB calculations

Cuts of this magnitude would be devastating for many seniors. If they were allowed to occur, the percent of senior beneficiaries in poverty would nearly double over a single year from 4.8 percent in 2033 to 9 percent when the trust fund runs out in 2034.

The Latest Projections Highlight the Need to Focus on Solvency First

Virtually every major bipartisan group that has studied the Social Security program has concluded that policymakers will need to both slow the growth of benefits and bring new revenue into the system. Given Social Security’s weak financial state, even price-indexing instead of wage-indexing benefits for all beneficiaries would barely delay insolvency, and even eliminating the cap on taxable and creditable earnings would close less than three-quarters of the 75-year shortfall and just over one-third of the 75th year deficit.

Recently, however, some politicians and advocates have called for abandoning the balanced bipartisan approach to fixing Social Security in favor of calls for across-the-board benefit increases. Larger benefits for some populations should be considered; but only in the context of a sustainably solvent system. Policymakers must put solvency first to avoid jeopardizing the retirement security of current and future generations.

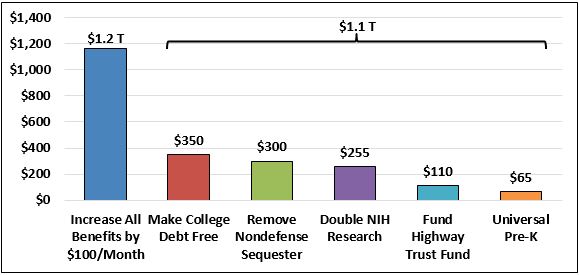

We’ve written before about why broad benefit increases for all seniors – including the rich -- would be wrongheaded and unnecessary to improve retirement security and reduce senior poverty. Given the large number of beneficiaries, even seemingly modest Social Security benefit increases would be hugely expensive. For example, increasing benefits for all seniors by an average of $100 dollars per month today would cost $1.2 trillion over the next decade and worsen Social Security’s 75-year shortfall by almost 50 percent.

Fig. 5: Ten-Year Cost of Broad Benefit Expansion and Other Priorities (Billions of Dollars)

Source: CBO, SSA, HHS, CRFB calculations

Simply paying for this benefit expansion would consume two-thirds of the savings from fully eliminating the cap on income subject to the payroll tax (and crediting benefits on new income) over 75 years, and eventually consumer nearly all the savings, leaving fewer options available to close the program’s existing structural gap.

Conclusion

The Social Security Trustees once again show the need to reform Social Security to make it solvent for future generations. The combined Social Security trust fund will run out of money within 18 years – when today’s 49-year-olds are just reaching the normal retirement age. Failure to make any changes would result in a 21 percent across-the-board benefit cut, a cut that would grow over time.

Fortunately, Social Security’s finances can still be fixed without making drastic tax or benefit changes. If policymakers are willing to act soon, they can develop and pass a plan that strengthens the program’s finances while phasing in changes gradually to give workers time to prepare, improving benefits for vulnerable beneficiaries, and promoting long-term economic growth. However the cost of delay is substantial and would take away the opportunity to act more gradually and thoughtfully. The Trustees make this case in their report:

If substantial actions are deferred for several years, the changes necessary to maintain Social Security solvency would be concentrated on fewer years and fewer generations…

The Trustees recommend that lawmakers address the projected trust fund shortfalls in a timely way in order to phase in necessary changes gradually and give workers and beneficiaries time to adjust to them. Implementing changes sooner rather than later would allow more generations to share in the needed revenue increases or reductions in scheduled benefits and could preserve more trust fund reserves to help finance future benefits.

Lawmakers should put in place the necessary policy changes and reforms well in advance of the insolvency date. Otherwise, they will be forced to rely on blunt and abrupt changes to ensure Social Security’s ability to pay full benefits.