Separating "Current Law" from A "Do Nothing" Baseline

CBO’s baseline budget projections are often referred to as “current law” since they generally assume Congress continues the laws as they are written (even when that is not the most realistic scenario). However, CBO’s baseline deviates in several important ways from what would happen under a strict interpretation of current law -- that is, if Congress were to pass no new laws.

For context, the CBO baseline is based on specifications laid out in the Congressional Budget Act of 1974 and the Gramm-Rudman-Hollings Act of 1985. Lawmakers wanted the baseline to be a useful benchmark against which to measure legislative changes, so they modified the baseline's assumptions from "pure" current law to better accomplish that goal. These deviations ensure that lawmakers will get relevant information about the magnitude of policy changes rather than having them obscured by technicalities. CBO is instructed to modify the strict interpretation of current law in cases when not doing so would be clearly unreasonable and thus devalue the baseline's function.

CBO's baseline differs from a strict current law baseline in four main ways.

It assumes:

- Certain trust fund spending is able to continue at levels scheduled under current law, even if the trust fund is insufficient to finance these costs and the trust fund is legally prohibited from making expenditures in excess of available revenues

- Certain spending programs and dedicated taxes whose authorizations are scheduled to expire are assumed to be permanent

- Discretionary budget authority, which is set by annual appropriations, will continue to grow with the rate of inflation unless it is limited by statutory spending caps

- Spending is assumed to continue at levels provided under current law even if the statutory debt ceiling is reached and Treasury is legally prevented from spending beyond incoming revenues

With these deviations, it might be more appropriate to describe CBO’s baseline as meeting the commitments of current law, rather than assuming no new legislation at all.

Each of these deviations is intended to provide a more accurate picture of the fiscal outlook and make the baseline a more useful benchmark in scoring the costs of new legislation. For example, if CBO assumed that no new appropriations were made after this fiscal year, changing the caps on future discretionary spending would be scored as having no effect, since technically no appropriations were made.

Likewise, if CBO assumed that expenditures were limited to incoming revenues when a trust fund was depleted, legislation providing new spending commitments that technically could not be funded because of trust fund depletion would be scored as having no cost. The same would be true of legislation providing for additional spending after the government was projected to reach the debt limit.

Under budget scoring rules, legislation creating or extending mandatory programs generally assumes the programs continue after the expiration date in the legislation and are scored accordingly. If those costs were not included in the baseline, legislation extending those programs would result in the same costs being scored twice.

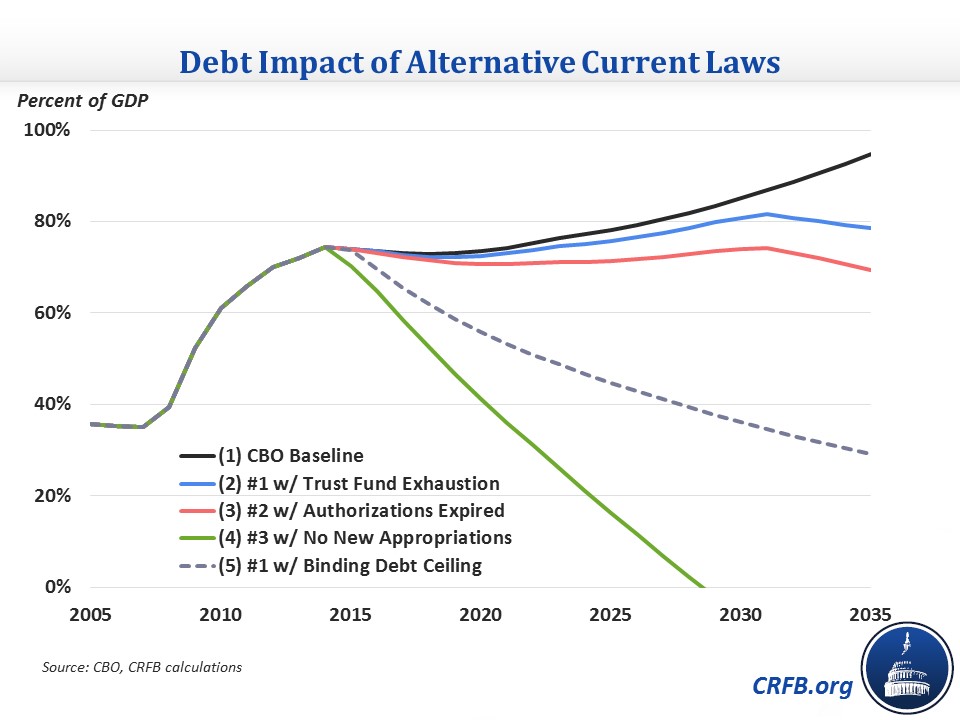

What if CBO did make baselines on a stricter adherence to current law? Under CBO's current baseline, debt is on an upward path as a percent of GDP every year after 2018, and we estimate it would reach 85 percent by 2030 and 95 percent by 2035.

The new "do nothing" baseline would incorporate a number of potentially unrealistic assumptions.

First, it would assume automatic spending cuts to bring outlays in line with revenue streams when trust funds were exhausted. This would result in a 27 percent cut to highway spending in 2015, a 20 percent cut to Disability Insurance beneficiaries in FY 2017, a 15 percent cut to Medicare Hospital Insurance spending in 2030, and a 25 percent cut to Old Age and Survivors' Insurance payments in 2032. Under this trust fund exhaustion scenario, debt would rise to 81 percent of GDP by 2030 before declining to 79 percent by 2035.

Second, because the new baseline would assume mandatory programs stopped when they expired, debt would lower to 74 percent in 2030 and 70 percent in 2035. These programs would include the Supplemental Nutrition Assistance Program (commonly called food stamps) and the Childrens' Health Insurance Program (CHIP) and dedicated taxes, such as the majority of the gas tax.

Finally, the biggest difference in the "do nothing" baseline would be assuming that no new appropriations are made after October 1 of this year (when the current appropriations bill expires). CBO's baseline has lawmakers providing $12.2 trillion of discretionary budget authority over the next ten years. If discretionary spending instead dropped to zero in future years, it would bring the budget into surplus starting in 2015 and result in the debt being fully paid off by the late 2020s.

Alternatively, if the "do nothing" baseline were similar to CBO's baseline but bound by the debt ceiling – which we estimate would be about $18.2 trillion when it's reinstated in mid-March – it would essentially assume a balanced budget. Debt would be on a continuously declining path to about 35 percent of GDP by 2030 and 30 percent by 2035. This total assumes that the Treasury Department will use $175 billion from suspending investments to the "G-Fund" to create a little additional headroom as well.

None of these numbers account for the economic effects, which would be substantial in some cases.

Obviously, none of these "do nothing" scenarios is likely. Lawmakers will not let long-standing programs and revenue sources simply lapse, and they won't eliminate departments and agencies wholesale by allowing appropriations to drop to zero. For these reasons, the CBO "current law" baseline is a much more useful benchmark than a literal do-nothing scenario.