Omnibus Package Includes $135 Billion of Unrelated Tax Breaks

The omnibus package includes government funding for the rest of fiscal year 2021 and significant COVID relief, but it also contains $135 billion over ten years of tax breaks not related to either of those priorities. This cost comes from an extension of many tax extenders that have been around for several years and several poorly targeted CARES Act provisions, as well as a number of new tax breaks that are either poorly targeted stimulus or not related to the COVID crisis.

The omnibus package includes $920 billion of COVID relief, such as $600 per-person checks for most households, extended and increased unemployment benefits through mid-March, another round of Paycheck Protection Program funding, and funding for vaccines, testing, and contact tracing. These items represent a legitimate response to the COVID crisis.

However, the package also includes $135 billion of tax breaks that are either unrelated to COVID or are very poorly targeted relief. The bulk of these measures, over $100 billion, comes from tax extenders, routinely extended temporary tax breaks that are mostly due to expire at the end of the year. Other policies are either extensions of poorly-targeted CARES Act policies or new ones that don't legitimately respond to the crisis.

A few of the tax extenders are made permanent, including expanding the medical expense deduction so taxpayers do not need as many medical expenses to qualify (setting the floor at 7.5 percent of adjusted gross income instead of 10 percent), at a cost of $32 billion cost over ten years, lower taxes on alcohol ($9 billion), and a tax credit for railroad maintenance ($2 billion). All of these policies predate the current crisis, and making them permanent is an obvious indication that their extensions are not related to the pandemic response.

Other policies are extended through 2025, coinciding with the expiration of major provisions of the 2017 tax law. These tax breaks include the work opportunity tax credit ($16 billion), the new markets tax credit ($6 billion), a paid leave credit ($4 billion), an exclusion for employer payments for student loans ($3 billion), an exclusion for mortgage debt forgiveness ($3 billion), special expensing rules for entertainment productions ($1 billion), and faster depreciation for motorsports venues ($224 million). Other than the student loan exclusion, all of these policies predate the current crisis, and the student loan provision is very poorly targeted.

Finally, other extenders are given a one-year extension through 2021. Most of these provisions are clean energy tax breaks ($13 billion), but a few other small provisions include allowing mortgage insurance premiums to be deducted ($207 million) and allowing expenses related to racehorses to be deducted more quickly.

| Policy | 2021-2030 Cost |

|---|---|

| Tax Provisions Made Permanent | $51 billion |

| 7.5% of income floor instead of 10% for medical expense deduction | $33 billion |

| Reduced excise taxes on beer, wine, & distilled spirits | $9 billion |

| Larger Lifetime Learning Credit in place of the deduction for qualified tuition & related expenses | $6 billion |

| Other provisions | $3 billion |

| Tax Provisions Extended Through 2025 | $40 billion |

| Work Opportunity Tax Credit | $16 billion |

| New Markets Tax Credit | $6 billion |

| Rule allowing American companies to transfer money tax-free between foreign subsidiaries | $4 billion |

| Tax credit for employers to offer paid family and medical leave | $4 billion |

| Exclusion for certain employer payments of student loans | $4 billion |

| Allow mortgages to be forgiven tax-free | $3 billion |

| Other provisions | $3 billion |

| Tax Provisions Extended Through 2021 | $7 billion |

| Extend and expand charitable deduction for non-itemizers & increase the maximum deduction in a single year | $4 billion |

| Other provisions | $3 billion |

| Other Temporary Tax Provisions | $39 billion |

| Eliminate 10% floor on claiming disaster property losses | $8 billion |

| Extend Energy Investment Tax Credit through 2023 | $7 billion |

| Temporary allow full business meals deduction through 2022 | $6 billion |

| Increase low-income housing tax credit rate | $6 billion |

| Extend and expand credit for buying residential energy-efficient property through 2023 | $4 billion |

| Depreciation of residential rental property over 30 years | $3 billion |

| Reduce interest rates used for life insurance contracts | $3 billion |

| Other provisions | $2 billion |

Source: Joint Committee on Taxation.

Besides the extenders, the package includes over $30 billion of other extraneous tax breaks. A few provisions are supposedly related to the crisis but very poorly targeted, including allowing business meals to be fully deductible instead of half-deductible for two years ($6 billion) and continuing the expansions the CARES Act made to the charitable deduction for a year ($4 billion). Other tax breaks aren't even related, such as a handful of disaster relief tax breaks ($10 billion), an increase in the minimum low-income housing credit ($6 billion), and faster depreciation for rental property ($3 billion).

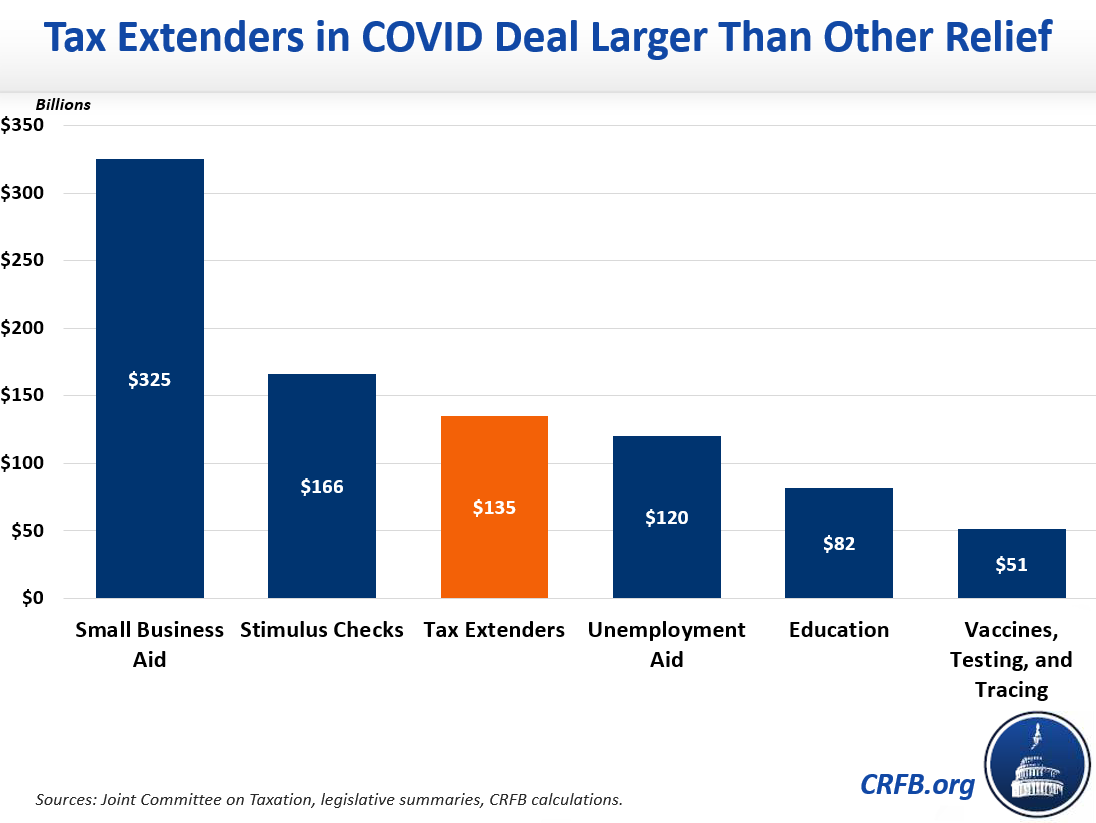

These extraneous tax breaks dwarf several legitimate COVID response items in size. They are $15 billion larger than the unemployment benefit extensions ($120 billion), significantly larger than funding for schools and students ($82 billion), and more than double the funding for testing, vaccines, and contact tracing ($51 billion). They are nearly as large as the $165 billion cost of the $600-per-person checks.

For the cost of these tax breaks, Congress could have increased the economic impact payments from $600 per person to $1,100, or offered expanded unemployment benefits for the first half of 2021 instead of for 11 weeks.

Continuing these temporary policies would also undermine sound tax policy. Many of the provisions made permanent or extended through 2025 are ones that lawmakers explicitly agreed to end after the 2015 extenders deal and let expire for nearly two years after 2017, before bringing them back as "zombie extenders" last year. Now, they are either permanent fixtures in the tax code or part of a huge tax cliff that is now set up at the end of 2025. In addition, the package extends permanently or for five years three policies – the medical expense deduction change, lower alcohol taxes, and the paid leave credit – that were explicitly temporary in the 2017 tax law. It also undermines an offset in the 2017 law by expanding the business meals deduction when it had just been restricted.

These tax breaks will add $135 billion to the debt without doing anything to address the COVID crisis. Unlike other parts of the bill that are legitimately an emergency, these giveaways should be offset.

Note: This blog was updated on 4/12/21 to move the 100 percent business meals deduction, energy investment tax credit, and the expanded and extended credit for buying residential energy-efficient property to the "other temporary tax provisions" table subsection.