Is Life Expectancy Really Falling?

During the fifth GOP presidential primary debate, Florida Governor Ron DeSantis argued against raising the Social Security retirement age because “life expectancy is collapsing in this country.”

Although Governor DeSantis has suspended his campaign for President, the claim that life expectancy is falling has been used by many to argue against adjustments to the Social Security retirement age.

Yet this claim obscures the reality. While a measure known as “average period life expectancy” did fall in 2020 and 2021 because of the COVID-19 pandemic, it has since been rising. It also offers little information about how long current Americans are expected to live. Experts and official sources all expect people to continue to live longer over time, thanks in large part to rising incomes and medical advances.

It is also important to note that many proposals to raise the retirement age ultimately index it to growth in life expectancy – meaning that the age would not go up in the unlikely case that life expectancy did remain stagnant.

| US Budget Watch 2024 is a project of the nonpartisan Committee for a Responsible Federal Budget designed to educate the public on the fiscal impact of presidential candidates’ proposals and platforms. Through the election, we will issue policy explainers, fact checks, budget scores, and other analyses. We do not support or oppose any candidate for public office. |

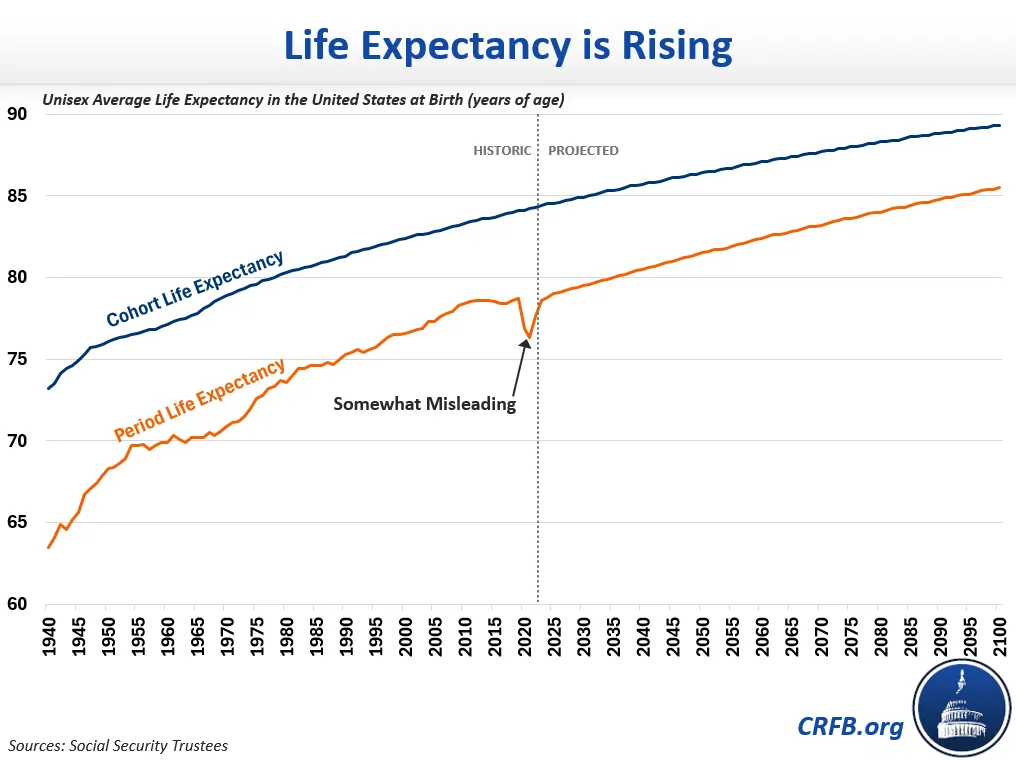

Life Expectancy is Rising, Not Falling

Americans today live far longer than they did decades ago and are likely to live far longer decades from now than they do today. There are technically two different measures of life expectancy, and both are currently rising.

Although life expectancy growth has slowed some in recent years due to opioid use and other factors, claims that life expectancy is falling are – to quote CRFB board member Gene Steuerle – “downright misleading.” These claims are based on a measure that doesn’t show how long people will actually live and was measured during the height of the recent pandemic, when COVID-19 took over 1 million American lives.

Estimates of how long people are likely to live are generated through a measure known as “cohort life expectancy,” which projects the average age of death for someone born or turning 65 in a given year. People born in 1940 had a cohort life expectancy of 73, while people born today have a cohort life expectancy of about 85, and people born in 2100 are projected to have a cohort life expectancy of 89. That means the average person born today is likely to live to be 85 and the average person in 2100 is likely to live to be 89 years old.1 Life expectancy is even higher for those who make it to age 65.

An alternative measure known as “period” life expectancy looks at the share of people who died at each age group in a given year and then uses those outcomes to measure the age the average person would die based on today’s death rates. As Steuerle explains, “Period life expectancy reflects population-wide mortality rates for given years…not remaining longevity for real people.”

Period life expectancy can be a helpful measure in that it is based on actual deaths that have occurred rather than projections of the future. But because medical technology and other factors improve over time, period life expectancy has always been (and likely will always be) well below actual expectations of longevity. It is also much more volatile than cohort life expectancy, as it reflects mortality that may come from anomalous events like wars or pandemics.

For this reason, period life expectancy did fall in 2020 and 2021. But that was a temporary phenomenon due to the COVID-19 pandemic. It has rebounded almost completely, and is clearly growing.

In contrast, the much more accurate and useful cohort life expectancy has continued to increase over time, growing roughly 10 months over the past decade and projected to grow 4 to 5 years by the end of the century.

Indexing the Social Security Age Would Address Life Expectancy Concerns

While life expectancy is not currently declining, proposals to index the retirement age to longevity would halt any increase in the age in the unlikely case that life expectancy did decline. That’s because the age would be linked to life expectancy itself and would only go up based on life expectancy growth. Differentials in life expectancy or ability to remain in the workforce could be addressed with an age-62 poverty-protection benefit or other types of adjustments and reforms.

The fact that the retirement age has not been linked to life expectancy thus far means that the Social Security trust fund will finance an additional 5 to 10 years in retirement today compared to 1940 and will fund an another 4 years by 2100.2

Boosting the retirement age would also lead many workers to delay retirement, which according to a growing body of research, leads to lower mortality. In other words, raising the retirement age may actually increase life expectancy. Increasing the retirement age would also improve Social Security solvency, boost income and economic growth, increase personal wealth and retirement income, improve physical and mental health, and strengthen social networks, among other benefits.

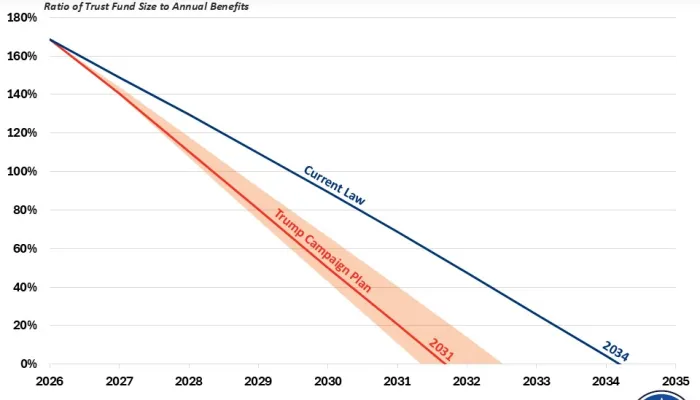

Without changes to Social Security’s retirement age, benefit formula, and/or revenue collection, beneficiaries will face a 23 percent across-the-board benefit cut in just 9 years – regardless of life expectancy. That’s a $17,400 cut in annual retirement benefits for a typical couple retiring in 2033.

*****

Throughout the 2024 presidential election cycle, US Budget Watch 2024 will bring information and accountability to the campaign by analyzing candidates’ proposals, fact-checking their claims, and scoring the fiscal cost of their agendas.

By injecting an impartial, fact-based approach into the national conversation, US Budget Watch 2024 will help voters better understand the nuances of the candidates’ policy proposals and what they would mean for the country’s economic and fiscal future.

You can find more US Budget Watch 2024 content here.

1 These estimates are from the 2023 Social Security Trustees report. Other projections may differ.

2 Cohort life expectancy at 65 increased from 14 to 21 years between 1940 and 2023, while Social Security’s earliest eligibility age declined from 65 to 62 and the normal retirement age increased from 65 to 67. Life expectancy is projected to continue to grow, but no further increase in the retirement age is currently scheduled.

What's Next

-

Image

-

Image

-

Image