JCT Confirms: Dynamic Scoring Doesn't Make Extenders Look Much Better

Lawmakers have so far been reluctant to pay for the group of temporary tax cuts known as the "tax extenders," instead generally just adding the cost of extending them to the debt in recent years. And often, they reach for excuses not to pay for extensions, sometimes even claiming that the positive economic effects of the extenders would generate enough revenue to pay for themselves (or at least a significant part of the cost). However, the Joint Committee on Taxation (JCT) in a new estimate now shows that dynamic scoring would only signal a slightly smaller cost for the tax extenders than a conventional score would.

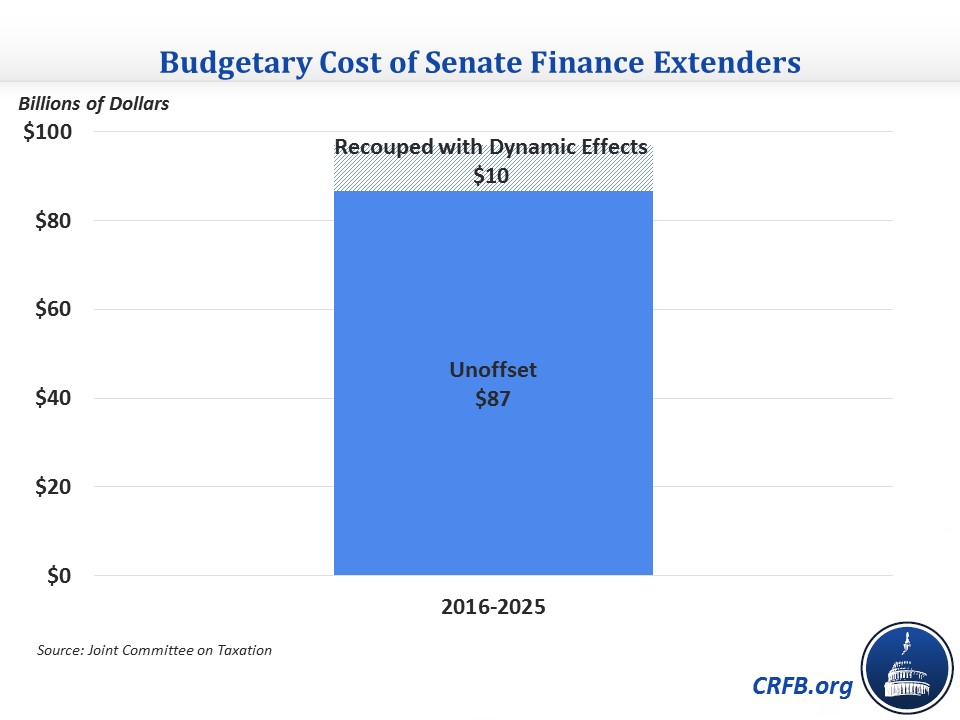

The JCT estimate looks at the Senate Finance Committee extenders package, which revives the extenders for 2015 and extends them through 2016 at a cost of $97 billion (the previous $95 billion cost included $2 billion of revenue-raisers that were used in the highway/veterans' law). JCT finds that the business provisions, in particular bonus depreciation, would increase business capital by 0.3 percent in the first five years and would increase output by 0.1 percent. Later in the ten-year period, the effects would fade and in the second and third decades would turn negative as a result of the increased debt caused by enactment.

The economic effects would generate $17.2 billion of higher revenue but also $6.8 billion of higher spending for a total effect of $10.4 billion, meaning the dynamic effects would only recover 11 percent of the initial revenue loss. The effects peak at $1.4 billion in 2022 and decline to $1.1 billion by 2025.

There has also been talk of making certain extenders permanent, as the House Ways and Means Committee has done, but that could fare even worse. JCT previously looked at a permanent extension of bonus depreciation and found that the ten-year dynamic effects would be small -- and could be negative -- while the cost of a permanent extension would be much larger than the two-year extension ($224 billion versus $3 billion). If extenders were used as a catalyst for tax reform, we estimated that even using the most generous model -- one that JCT did not use for its Senate Finance score -- tax reform would produce dynamic effects to offset only 55 percent of the cost of making the extenders permanent.

Simply put, lawmakers are not going to be able to hand-wave away the cost of tax extenders legislation, nor should they. Our PREP Plan showed that it is quite possible to pay for a two-year extenders package. The tax extenders need not add to the $180 billion of deficit increases that lawmakers have already enacted this year.