Elmendorf Explains Dismal Fiscal Picture to Economists

UPDATE: Read Elmendorf's take on his talk.

Today, several of us at the CRFB staff attended a National Economists Club lunch with Congressional Budget Office Director Doug Elmendorf. Although Elmendorf discussed a number of topics ranging from health care to the economy (see his slides here), his focus was on the nation's medium term budget outlook.

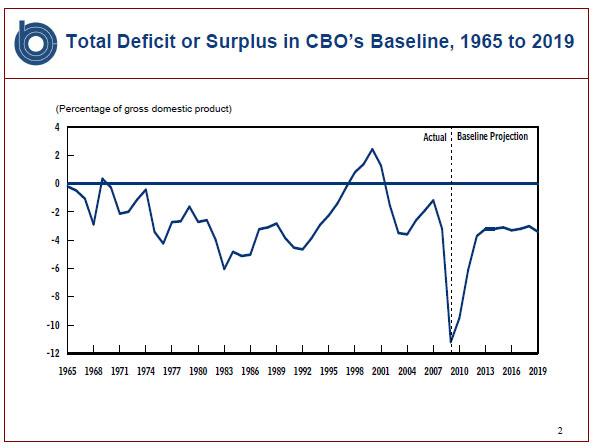

Elmendorf opened by pointing out that after the economy recovers, CBO projects deficits to settle in at around 3 percent of GDP. And while this is troubling, Elmendorf explained, it is not unprecedented and has historically been manageable. He then went on to explain why this time is different, and why the actual situation is much worse than it appears.

Elmendorf showed us that, through the 1980s, the nation ran deficits averaging 3 percent of GDP -- and seemed to come out of it just fine. But three things, in particular, are different this time:

- Our debt is much higher;

- There is a large disconnect between current law and current policy;

- The fiscal consequences of population aging and health care cost growth are now imminent.

National Debt

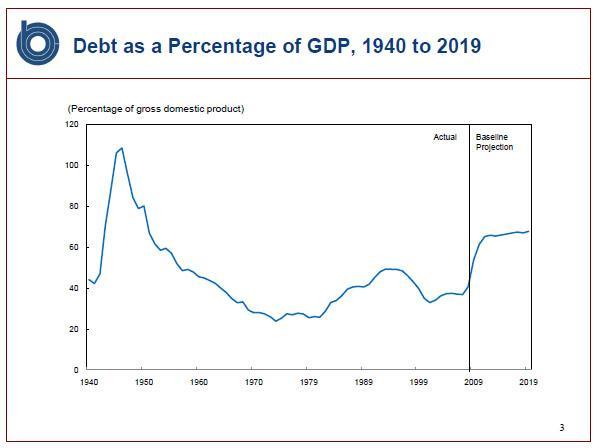

In the 1980s, Elmendorf showed, public debt barely ever eclipsed 40 percent of GDP. In fact, when Reagan took office, it stood at only 25 percent. Today, conversely, debt is heading toward 60 percent of GDP. Higher levels of debt make large deficits both more expensive and potentially more damaging. At some point, debt can reach levels so high that creditors are no longer willing to invest in government bonds;

Current Law

More importantly, Elmendorf explained, there is a big disconnect between what CBO projects under its "current law" baseline, and what is actually expects policy makers to do. We've made this point before -- more thoroughly in The Cost of “Current Policy”. As we explained there (and Elmendorf articulated in his talk), several provisions scheduled to expire under current law -- the Bush tax cuts, the AMT path, and the Medicare physician payment patch -- are unlikely to actually expire. And if history is any indication, discretionary spending will grow much faster than under the CBO baseline. We estimate that, if these assumptions were incorporated into the baseline, the ten year deficit would be at least $5 trillion higher than under CBO's baseline. As Elmendorf argued, by 2019 "instead of a deficit of 3.5 percent of GDP we could be looking at a deficit of 8.5 percent".

Aging and Health Care Cost Growth

But that isn't even the worst of it. Even if policy makers allowed all the Bush tax cuts to expire, stopped patching the AMT, allowed a 21 percent cut in Medicare physician payments, and held discretionary spending growth to inflation, they would still have a problem. Over the next decade, the large baby boom generation will begin to retire en masse. As they exit the labor force, they will no longer be a source of tax revenue, and instead begin to draw, from the Social Security system, more than it can afford. More significantly, this population will begin drawing from Medicare. And the compounding effects of population aging and health care cost growth (the latter of which is more significant over the longer-run) threaten to balloon the costs of Medicare and Medicaid.

Given all this, we can't help but concur with Director Elmendorf's assertion that things could get "very very bad, very very quickly."

This is why we've called for a medium-term fiscal consolidation plan. We still worry about the long-term, of course; but doing so is no longer sufficient. As the economy recovers, rising debt could very quickly become a serious economic problem. Under CBO's alternative fiscal scenario, it will eclipse 100 percent of GDP by the early 2020s -- and our creditors may not stand for that.

Detractors will argue that serious deficit reduction is politically difficult and economically dangerous. But as we've shown in "Deficit Reduction: Lessons from Around the World," many other free and prosperous countries have found it is to be both achieveable and economically beneficial. Of course we don't want to enact contractionary fiscal policy before the economy has stabilized. But if we don't get our debt under control soon, any economic stability we achieve will be fleeting, and we'll be wishing we had acted on our own terms, when we had the chance.