Economic Projections in CBO's Budget Update

Since economic assumptions have such a big effect on fiscal projections, we have compared their new assumptions in the Updated Budget and Economic Projections to their previous assumptions and to OMB's projections in the Mid-Session Review (click here for an analysis of the MSR).

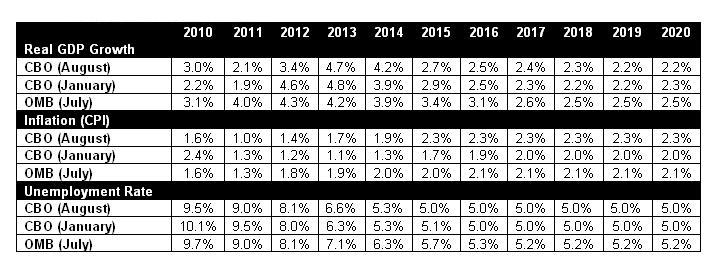

In light of more recent economic data, CBO is now projecting slightly higher growth this year and next year compared to its previous projections. Growth is now expected to reach 3.0 percent this year and 2.1 percent next year, above the 2.2 and 1.9 percents, respectively, projected earlier. CBO and OMB projections diverge significantly next year, where CBO sees growth slipping and OMB assumes growth of 4.0 percent. In order to explain some of the variation between CBO’s and OMB’s economic projections, it should be noted that CBO incorporates different assumptions. As CBO explains:

“Differences between the projections of CBO and those of other forecasters probably stem primarily from a difference in assumptions about fiscal policy. Most forecasters appear to assume that the Congress will extend at least some of the tax cuts enacted in 2001 and 2003 as well as some relief from the AMT. In contrast, CBO’s forecast is predicated on the assumption that current law is maintained.”

This highly important factor must be taken very seriously as we agree with CBO that it is highly unlikely that there will be no extension of the 2001/2003 tax cut or the annual AMT fix. Thus, larger potential deficits from extensions of “current policies” would also yield different economic outcomes going forward. CBO states that under an alternative fiscal path, growth would be higher in the short-term but lower by the end of the decade as larger deficits would hamper growth. This is an important trade-off to take note of.

CBO also projects an improved unemployment rate from its earlier estimates. Unemployment is now expected to average 9.5 percent this year, down from CBO’s previous 10.1 percent. CBO’s unemployment estimates are now more in line with those from OMB. A lower unemployment rate will put less pressure on safety-net spending and increase tax receipts as the number of people in the workforce and wages rise, helping to reduce future deficits and debt. CBO has also lowered its inflation estimates in the near-term, but raised them in the long-term, citing the expectation that the Federal Reserve will “attempt to maintain an inflation rate for consumer prices near the top end of the central tendency of the long-range forecasts for inflation.”

CRFB believes that policymakers should begin work now on developing a fiscal plan. But when they do so, we also believe that they should pursue the best possible mix of policies to encourage growth – as a stronger economy will reduce future deficits and our borrowing needs via imrpvoed automatic stabilizers (such as lower unemployment benefits and higher government revenues). A stronger economy would also increase the denominator in debt-to-GDP calculations, making a return to sustainable fiscal paths much easier.