Can Donald Trump Eliminate the Debt?

In discussing another potential term in office, last month, former President Donald Trump declared, "we’re going to pay off our debt.” President Trump similarly promised to pay off the national debt within eight years during his 2016 presidential campaign.1

Although it is impossible to know the future, this claim is almost certainly false. Absent massive revenue increases – which President Trump has never mentioned – it would be literally impossible to pay off the national debt over the four years of the next presidential term, and practically impossible to pay it off over the ten-year budget window.

Over four years, even eliminating all spending would not be enough to pay off the debt, nor would doubling revenue collection. Over ten years, paying off the debt would require cutting all federal spending by about 60 percent or boosting revenue by two-thirds. Assuming Social Security, Medicare, and defense spending are exempt from cuts – consistent with President Trump’s rhetoric – even eliminating all remaining spending would not pay off the debt without trillions of additional revenues.

| US Budget Watch 2024 is a project of the nonpartisan Committee for a Responsible Federal Budget designed to educate the public on the fiscal impact of presidential candidates’ proposals and platforms. Through the election, we will issue policy explainers, fact checks, budget scores, and other analyses. We do not support or oppose any candidate for public office. |

How Much Savings Would be Needed to Pay Off the Debt?

At the beginning of the next presidential term, debt held by the public is likely to total around $28.5 trillion. It is projected to grow by an additional $7 trillion over the next presidential term and by $22.5 trillion through the end of Fiscal Year (FY) 2035.

This means paying off the debt over four years would require generating about $35.5 trillion of budget and interest savings – covering the $28.5 trillion of initial debt and preventing the accumulation of $7 trillion of further debt. To achieve this, policymakers would need to turn $1.7 trillion average annual deficits into $7.1 trillion annual surpluses.

Over the ten-year budget window starting in the next presidential term, spanning from FY 2026 through FY 2035, policymakers would need to achieve $51 trillion of budget and interest savings – enough to cover the $28.5 trillion of initial debt and prevent $22.5 trillion in debt accumulation. This would mean turning $2.1 trillion average annual deficits into $3 trillion annual surpluses.

Can the Debt be Paid Off Within the Next Presidential Term?

It would be literally impossible to pay off the debt by the end of the next presidential term without large accompanying tax increases, and likely impossible with them. While the needed savings would equal $35.5 trillion, total spending is projected to be $29 trillion over that four-year period – of which $4 trillion is interest and cannot be cut directly. We estimate it would require the equivalent of cutting all non-interest spending by about 130 percent, which is of course impossible. (Even under a rosy scenario that assumes much faster economic growth and substantial new tariff revenue, cuts would be nearly as large).

It is also likely impossible to achieve these savings on the tax side. With total revenue expected to come in at $22 trillion over the next presidential term, revenue collection would have to be nearly 250 percent of current projections to pay off the national debt. It’s not clear that this level of revenue collection is even possible without being above revenue-maximizing tax rates, and it is certainly not consistent with President Trump’s calls to lower taxes.

Can the Debt be Paid Off Over Ten Years?

Although it would require less in annual savings to pay off the national debt over ten years relative to four years, it would still be nearly impossible as a practical matter.

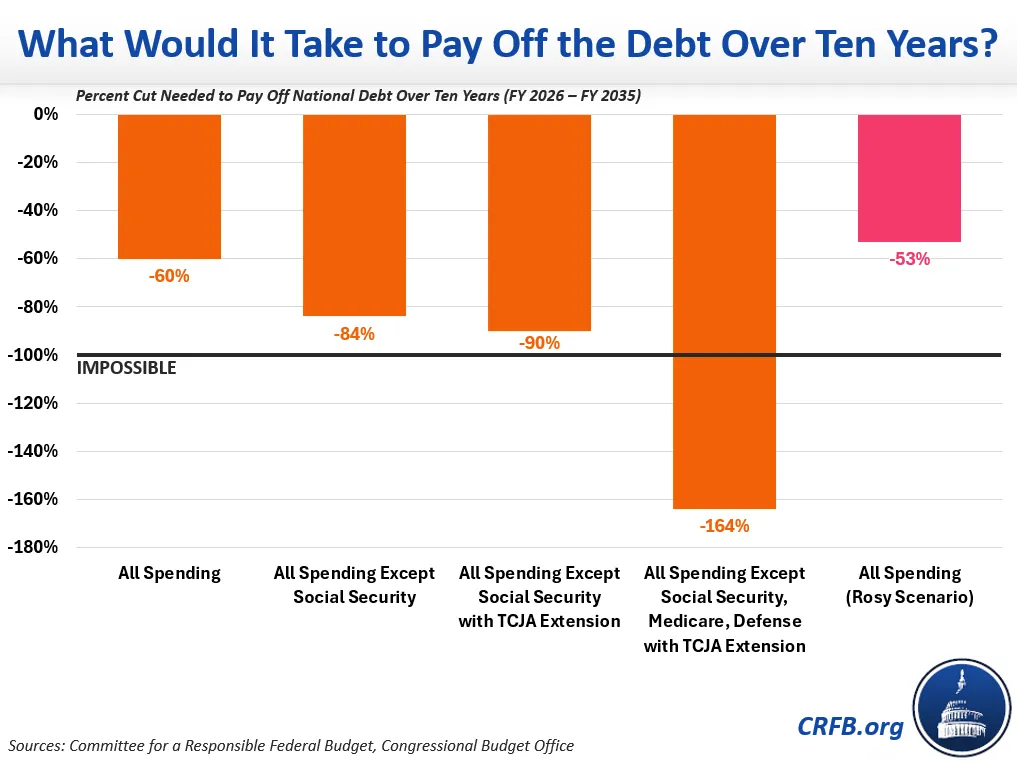

We estimate that paying off the debt over the ten-year budget window between FY 2026 and FY 2035 would require cutting spending by about 60 percent – which would lead to $44 trillion of primary spending cuts and an additional $7 trillion of resulting interest savings. This would be the equivalent of eliminating Social Security, Medicare, Medicaid, and food stamps or eliminating all spending besides defense and Social Security.

The task becomes even harder when one considers the parts of the budget President Trump has taken off the table, as well as his call to extend the Tax Cuts and Jobs Act (TCJA). For example, President Trump has committed not to touch Social Security, which means all other spending would have to be cut by nearly 85 percent to fully eliminate the national debt by the end of FY 2035.

Assuming lower revenue from full extension of the TCJA, needed cuts would grow to 90 percent. If Medicare and defense spending were also exempted – as President Trump has sometimes called for – spending would have to be cut by nearly 165 percent, which would obviously be impossible.

In other words, spending cuts alone would not be sufficient to pay off the national debt. Massive increases in revenue – which President Trump has generally opposed – would also be needed. The two ways in which President Trump has been willing to consider increasing revenue are from higher tariffs and from assumed (but unlikely to materialize) increases in economic growth. A rosy scenario that incorporates both of these doesn’t make paying off the debt much easier.

Specifically, President Trump has called for a Universal Baseline Tariff that we estimate could raise $2.5 trillion over a decade. He has also claimed that he would boost annual real economic growth from about 2 percent per year to 3 percent, which could generate an additional $3.5 trillion of revenue over ten years. Assuming both materialize – a rosy scenario – President Trump would still need to cut all spending by more than 50 percent, or all non-Social Security spending by nearly 75 percent, in order to eliminate the national debt by the end of FY 2035.

Importantly, it is highly unlikely that this revenue would materialize. As we’ve written before, achieving sustained 3 percent economic growth would be incredibly challenging on its own. Since tariffs generally slow economic growth, achieving these two in tandem would be even less likely.

Will President Trump Pay Off the Debt?

While no one can know the future with certainty, the cuts necessary to pay off the debt over even ten years (let alone four years) are not even close to realistic. The two largest spending cut bills enacted over the past two decades – the Budget Control Act (BCA) of 2011 and the Fiscal Responsibility Act (FRA) of 2023 – reduced spending by 5 percent and 2 percent, respectively. Even these estimates overstate their effects, since much of the BCA’s sequester cuts were ultimately reversed and policymakers are currently working to avoid some of the cuts called for under the FRA. There is no reasonable path for policymakers to enact savings that are orders of magnitude larger than in these bills.

Percent Spending Cut Needed to Eliminate the National Debt

| Four Years (next presidential term) |

Ten Years (FY 2026 - FY 2035) |

|

|---|---|---|

| All Spending | 129% | 60% |

| All Spending Except Social Security | 178% | 84% |

| All Spending Except Social Security with TCJA Extension | 184% | 90% |

| All Spending Except Social Security, Medicare, and Defense with TCJA Extension |

323% | 164% |

| All Spending (Rosy Scenario) | 123% | 53% |

Sources: Committee for a Responsible Federal Budget, Congressional Budget Office

Nor does President Trump’s term in office offer any evidence that such massive cuts could be achieved. In his four years as President, President Trump did not sign into law a single piece of legislation that reduced deficits, and only signed one bill that meaningfully reduced spending (by about 0.4 percent). On net, President Trump increased spending quite significantly – by about 3 percent, excluding one-time COVID relief. In total, he approved about $8.4 trillion of new borrowing over ten years.

During President Trump’s term in office, federal debt held by the public grew by $7.2 trillion – from $14.4 to $21.6 trillion. This includes a $3 trillion increase through February of 2020, before the COVID-19 pandemic hit the United States. And even by its own, very rosy estimates, President Trump’s final budget proposal – introduced in February of 2020 – would have allowed debt to rise in each of the subsequent ten years, from $17.9 trillion at the end of FY 2020 to $23.9 trillion by the end of FY 2030.

So, while reducing debt is an admirable goal and all candidates should put forward plans to reduce debt as a share of GDP, there is no realistic way that President Trump or any other candidate will pay off the debt any time soon.

Our Ruling: Almost Certainly False

*****

Throughout the 2024 presidential election cycle, US Budget Watch 2024 will bring information and accountability to the campaign by analyzing candidates’ proposals, fact-checking their claims, and scoring the fiscal cost of their agendas.

By injecting an impartial, fact-based approach into the national conversation, US Budget Watch 2024 will help voters better understand the nuances of the candidates’ policy proposals and what they would mean for the country’s economic and fiscal future.

You can find more US Budget Watch 2024 content here.

1 During the 2016 campaign, we noted that “no plausible set of policies could pay off the debt in eight years.” With an additional $13.3 trillion added to the debt in the interim, this is even more true today.

What's Next

-

Image

-

Image

-

Image