Reconciliation 101

Note: We have updated this paper, please see our Updated Reconciliation 101.

What is reconciliation?

Reconciliation is a special legislative process created as part of the Budget Act of 1974. It is intended to help lawmakers make the tax and mandatory spending changes necessary to meet the levels proposed in the congressional budget resolution.

Reconciliation instructions are put forward as part of a concurrent budget resolution that passes both chambers of Congress. These instructions set cost or savings targets for the congressional committees, with instructions covering mandatory spending, revenue, or debt limit changes. Following these instructions, committees of jurisdiction identify specific policies to meet these goals in the form of a reconciliation bill, which can be enacted on a fast-track basis.

Reconciliation bills are privileged in a number of ways, including with a 20-hour limit on debate in the Senate, a non-debatable motion to proceed to the bill, and a strict germaneness test for amendments. In the Senate, the limit on debate time and non-debatable motion to proceed means a reconciliation bill cannot be filibustered – allowing the Senate to pass a reconciliation bill by a simple majority rather than needing 60 votes to end debate.

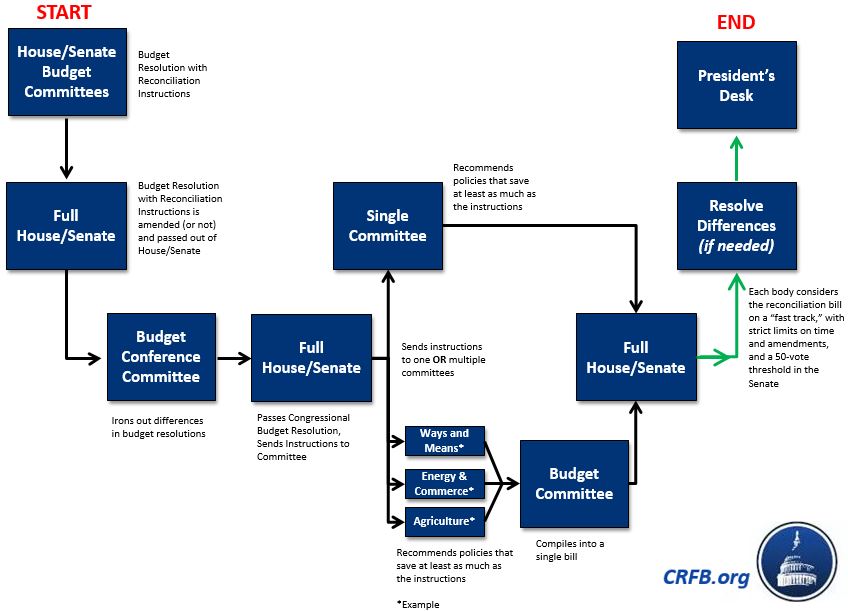

How do reconciliation instructions work?

The budget reconciliation process begins with the passage of a concurrent budget resolution in both chambers of Congress that includes reconciliation instructions. The reconciliation instructions identify the authorizing committee(s) tasked with reconciliation, the dollar amount of budgetary changes that must be achieved over designated time frames (usually the first year of the budget and the five- or ten-year period covered by the budget resolution) that the committee(s) must achieve, and the date by which the committee(s) must report reconciliation legislation.

Reconciliation instructions may also direct the House Ways and Means Committee and the Senate Finance Committee to report legislation to change the limit on the public debt in accordance with the spending levels in the budget resolution.

While budget resolutions often assume and even suggest that committees include specific policies, these suggestions are not binding or enforceable. The budget resolution sets dollar targets, but the committees decide how these targets are met, substantively limited only by their jurisdiction.

If only one committee has reconciliation instructions, the reconciliation legislation reported by that committee goes directly to the House or Senate floor for consideration. Often, instructions will span across multiple committees. In this case, each committee reports their bill to the budget committee, which in turn combines the individual bills into an omnibus measure to send to the floor for a vote.

Can a reconciliation bill add to the budget deficit?

Although reconciliation is often used for deficit reduction, it is technically allowed to either decrease or increase the deficit over the time period covered by the budget resolution. It is also possible for a reconciliation bill to contain provisions with costs as well as savings, so long as the net effect complies with the reconciliation instructions.

In 2007, the Senate adopted the “Conrad rule,” which prohibited reconciliation from increasing deficits. However, the Conrad rule was repealed in the 2015 budget resolution (over CRFB’s objections). Even without the Conrad rule, reconciliation legislation must comply with the spending and revenue levels in the budget resolution. There would also be a 60-vote point of order if the bill increased the deficit over the first five or first ten years, per the Senate “Pay as you go” (PAYGO) rule, unless the budget resolution repealed the Senate PAYGO rule or established an exception to it.

Deficit increases under reconciliation are also subject to the statutory PAYGO law, which does not allow net increases in the deficit over the course of a year. An exclusion from the Senate PAYGO rule and statutory PAYGO would be subject to a 60-vote point of order.

Finally, provisions in a reconciliation bill that increase the deficit beyond the period covered by the budget resolution are subject to a 60-vote point of order under the “Byrd rule” unless the costs are offset by savings from other provisions in the bill.

What is the “Byrd Rule”?

Although reconciliations bills are granted many privileges that are not available to most other legislation, they remain bound by several conditions. Some of these restrictions championed by former Senator Robert Byrd (D-WV) and established in Section 313 of the Budget Act are jointly referred to as the “Byrd Rule.” The Byrd rule disallows “extraneous matter” from a reconciliation bill, including through three major restrictions on reconciliation legislation.

First, reconciliation legislation must only involve budget-related changes and cannot include policies that have no fiscal impact, that have “merely incidental” fiscal impacts, or that increase the deficit if the committee did not follow its reconciliation instructions. Second, reconciliation bills cannot change Social Security spending or dedicated revenue, which are considered “off-budget.” And finally, provisions in a reconciliation bill cannot increase the deficit in any fiscal year after the window of the reconciliation bill unless the costs outside the budget window are offset by other savings in the bill.

The Byrd rule provides a “surgical“ point of order that strikes any provisions in violation without blocking the entire bill. However, the Byrd rule can also be waived by 60 votes. Even though this point of order only exists in the Senate, it de facto governs the House too, given that it can be applied to any conference report.

What are other restrictions on reconciliation?

The Senate parliamentarian has ruled that a budget resolution can only provide for one reconciliation bill each of revenues, spending, and debt limit. If a reconciliation bill has both spending and revenue provisions, no other reconciliation bill affecting spending or revenues is allowed. Reconciliation bills cannot change the budget process either, such as by establishing or modifying discretionary spending limits, because the changes must directly affect spending or revenues. The Senate parliamentarian has also ruled that a reconciliation bill cannot create or amend any type of fast-track procedure for legislation limiting debate time in the Senate.

How has budget reconciliation been used in the past?

In total, 20 bills have become law through reconciliation, including the 1990 Omnibus Budget Reconciliation Act, the Balanced Budget Act of 1997, the 2001 and 2003 tax cuts, and portions of the Affordable Care Act. Some of these efforts, such as the 1990 and 1993 Omnibus Budget Reconciliation Acts, have produced significant deficit reduction (each saved nearly $500 billion over five years) while others, such as the 2001 and 2003 tax cuts, have increased deficits. We have a published a full comparison of past reconciliation bills here.

In addition to the 20 enacted reconciliation bills, 4 reconciliation bills have passed both chambers of Congress but were subsequently vetoed by the president. Most recently, President Obama vetoed legislation passed in 2015 that would have repealed large parts of the Affordable Care Act.

Can reconciliation be used to repeal and replace “Obamacare”?

Reconciliation could be used to repeal and replace some parts of the Affordable Care Act (ACA or “Obamacare”) but could not be used to fully repeal the law and could only be used for replacement policies affecting spending and revenues.

Full repeal would violate numerous parts of the Byrd rule. First, full repeal would cost roughly $500 billion over a decade since the legislation’s Medicare cuts and tax increases exceed the ACA’s new spending, and those costs would grow over time. Second, the provisions increasing costs outside of the budget window would violate the Byrd rule. Further, parts of the ACA contain non-budgetary items that would be subject to the Byrd rule if repealed in a reconciliation bill.

To comply with the Byrd rule, the reconciliation bill passed in 2015 to repeal the ACA largely left in place the legislation’s Medicare reductions. The reconciliation bill also initially delayed but did not repeal the so-called “Cadillac tax” on high-cost insurance plans to avoid revenue loss outside the budget window, but an amendment repealing it was adopted by an overwhelming bipartisan vote and no Byrd rule challenge was raised despite its deficit impact.

Additionally, the legislation left in place a large number of legal requirements in the ACA, including the essential benefits package requirements, the prohibition on insurers denying or charging more for coverage for those pre-existing conditions, the limits on “medical loss ratios,” and other changes that do not have a direct budgetary effect. It also technically retained the legislation’s individual mandates (though it reduced the penalties to $0) and left in place the Independent Payment Advisory Board, which can make Medicare savings recommendations subject to congressional disapproval on a fast-tracked basis.

Importantly, reconciliation legislation can include provisions with costs, such as tax credits for health insurance or other tax and spending policies replacing Obamacare, as long as the net effect of the bill complies with the reconciliation instructions and does not increase the deficit beyond the budget window. The budget resolution that provides reconciliation instructions would need to include the costs and savings of both the repeal and the replacement. If replacement legislation were considered as part of a separate reconciliation process, then the replacement plan (assuming a net cost) would likely need to sunset to avoid increasing the deficit beyond the budget window, unless the reconciliation legislation contained other savings to offset the net cost of replacement. Any changes in requirements for insurance companies, which are likely to be an important element of any replacement legislation, could not likely be passed under reconciliation without 60 votes to waive the Byrd rule.

Can reconciliation be used for tax reform?

Most of tax reform has a direct revenue impact and probably could be enacted through reconciliation, but it would either need to be revenue-positive over the long run or else rely on gimmicks, such as sun-setting rate reductions or other revenue-reducing provisions, to avoid increasing the long-term debt.

Importantly, tax reform legislation would need to comply with both the reconciliation instructions and the revenue floor set by the budget resolution. This means that any net tax cut over the ten-year period not explicitly called for by the budget resolution would be subject to a budget point of order that would require 60 votes to override. The last concurrent budget resolution passed by House and Senate Republicans held revenue to current law levels. In order to allow tax reform legislation that reduces revenues through reconciliation, the budget resolution would have to set a revenue level below current law and give the Ways and Means Committee instructions to reduce revenues. Alternatively, the budget resolution could set revenues at current law levels with reconciliation instructions for a nominal change in revenues to require revenue-neutral tax reform.

Compliance with reconciliation instructions and the revenue floor in the budget resolution is determined based on estimates supplied by the Chairman of the Budget Committee, which could potentially rely on dynamic scoring.

There will also be many special rules and other technical provisions to make tax reform work properly that may not survive Byrd rule scrutiny. If that is the case, then follow-up legislation to make tax reform stick may be required, and would be subject to traditional floor proceedings. Reforms of the Internal Revenue Service, which have often been included in tax reform legislation, would also violate the Byrd rule.

Can reconciliation legislation include budget process changes?

The Byrd rule restriction against provisions that do not directly affect spending or revenues would prohibit most changes to the budget process and budget enforcement rules. Most budget process and budget enforcement provisions do not by themselves change spending or revenues but rather apply to subsequent legislation affecting spending and revenues.

As a result, provisions adjusting or extending discretionary spending limits could not be considered because the actual increase or decrease in spending would not occur until subsequent action on appropriations bills subject to the limits. The Byrd rule also prohibits provisions that exempt the budgetary effects of reconciliation legislation from budget enforcement rules.

How may reconciliation be used in the new Congress?

Both tax reform and “repeal and replace” appear to be high priorities for the incoming White House and Congress, but because both have tax and spending components they could not be passed through reconciliation instructions from one budget resolution unless they were part of the same legislation.

As an alternative, House Republicans have floated the possibility of adopting a Fiscal Year (FY) 2017 budget resolution early next year (since Congress failed to adopt a FY 2017 budget resolution last year) to include reconciliation instructions for repealing (and possibly replacing) much of the ACA, while adopting a FY 2018 budget resolution later next year that includes reconciliation instructions for tax reform (and possibly some mandatory spending changes, perhaps from Medicare reform, other mandatory savings assumed in the budget resolution, and/or some ACA replacement).

Where should we go from here?

Budget reconciliation can be a powerful tool to enact reforms of mandatory spending and revenues for deficit reduction. Recent budget resolutions have assumed significant mandatory savings to achieve balance on paper, but failed to use reconciliation as a tool to actually achieve the savings assumed in the resolution. CRFB has suggested requiring budget resolutions to include reconciliation instructions to achieve any deficit reduction from revenues or mandatory spending assumed in the budget resolution.

Congress should utilize reconciliation to enact responsible deficit reduction such as revenue-raising tax reform or entitlement reforms that slow long-term spending growth. Given our high and rising debt, Congress should use reconciliation to reduce deficits, not to make our unsustainable fiscal situation even worse.