Principles for Responsible Tax Reform

The United States tax code has not been overhauled in over three decades, and it is in desperate need of reform. The current federal income tax is in many ways anti-growth, overly complex, uncompetitive internationally, and unfair. It is also littered with nearly $1.6 trillion in annual tax preferences that keep both tax rates and deficits higher than they would otherwise need to be.

Individual and business tax reform both belong near the top of an economic growth agenda for any President or Congress, so we are encouraged by the recent focus on pursuing a fix to the tax code.

However, with the debt a higher share of the economy than any time outside of the World War II era, getting the nation’s fiscal house in order must also top any agenda to promote economic growth. Tax reform should contribute to this goal or at least not conflict with it.

Fiscally responsible tax reform could improve incentives to work and invest, reduce compliance costs, improve fairness and efficiency, make America more competitive internationally, create certainty and predictability, and accelerate economic growth. Irresponsible reform, on the other hand, threatens to undermine many of these potential benefits.

In Five Reasons to Pay For Tax Reform, we make the case for a fiscally responsible approach to tax reform. Here, we set five guiding principles for what such reform should look like.

Specifically, fiscally responsible tax reform should:

- Promote Economic Growth and Dedicate the Gains to Deficit Reduction

- Maintain or Reduce Current Law Deficits

- Set Permanent Tax Policy

- Avoid Unjustified Timing Shifts, Double Counting, or Other Gimmicks

- Rely on Reasonable Economic Assumptions

By following these principles, tax reform could be an incredibly successful venture for both the economic and fiscal health of the nation.

Promote Economic Growth and Dedicate the Gains to Deficit Reduction

First, tax reform should be designed to promote economic growth. And revenue gains that result from such growth should be used to help address our post-WWII era record-high debt.

The current tax code in many ways discourages work, savings, and investment while also promoting decision-making based on tax planning rather than economic value. Our corporate tax code puts American businesses at a disadvantage relative to international competitors.

By lowering tax rates, broadening the tax base, and pursuing other changes, tax reform can help to unlock some of the nation’s growth potential. Based on estimates from the Joint Committee on Taxation (JCT) and Treasury Department, comprehensive reform can increase the growth rate over the next decade by 0.05 to 0.25 percentage points per year – a 3 to 14 percent improvement from current law projections.

There are myriad benefits of economic growth, including higher wages, expanded wealth, more jobs, and enhanced economic security. Faster growth also means more taxable income and thus tax revenue generated without increasing taxes. Given the gap between spending and revenue under current law, this revenue should go toward reducing projected budget deficits.

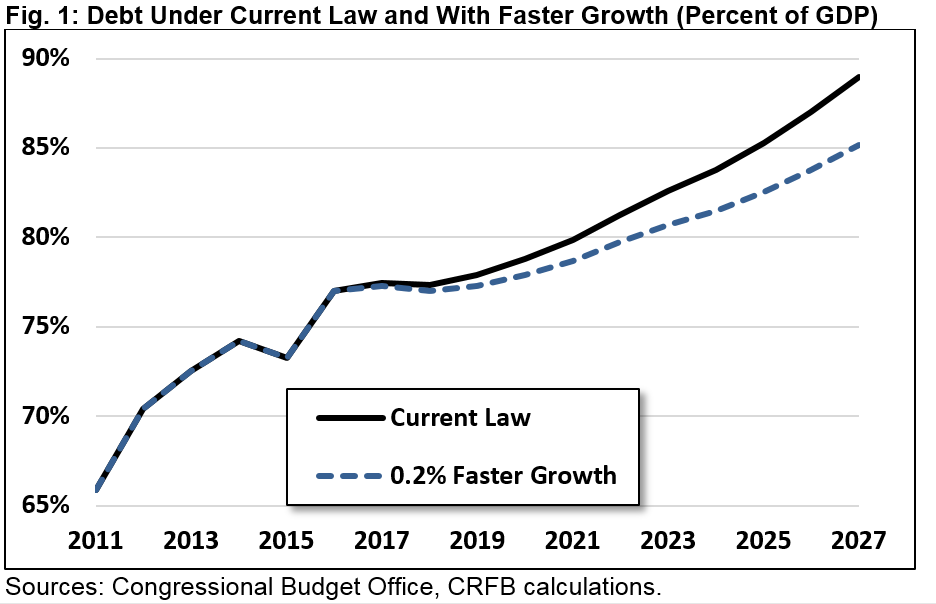

A 0.2 percentage point increase in the growth rate, for example, would reduce deficits by about $550 billion over a decade and reduce debt in 2027 by about 4 percent of Gross Domestic Product (GDP). This is not nearly enough to fix the fiscal situation but it would certainly help.

Importantly, if the gains from growth are used to finance further tax rate cuts, they cannot also be used to help address our mounting debt. The same funds cannot be used twice.

Maintain or Reduce Current Law Deficits

Tax reform should not add to the national debt. The national debt is higher than any time in history outside of the World War II era, and it is growing unsustainably. Outside of a true emergency, no legislation should make the debt situation even worse, regardless of the merits.

Ultimately, our fiscal challenges are unlikely to be solved without reducing spending, reforming entitlements, and increasing revenue. Therefore, tax reform should preferably be designed to reduce deficits and contribute to fiscal improvements along with other needed reforms. At a bare minimum, however, tax reform should be fully paid for so that it does not add to the national debt over the scoring window or beyond relative to a current law baseline.

Since deficit neutrality is a minimum fiscal goal, it should be measured using a strict and conservative standard. That means tax reform should not add to the debt under conventional or dynamic scoring, this decade or in future decades, or under any reasonable baseline.

Our current unsustainable debt projections assume the expiration of many tax provisions that Congress agreed not to continue permanently in late 2015. The use of a “current policy” baseline that assumes these provisions are permanent would obscure $450 billion or more in tax cuts and would not change the reality that reform under that baseline would worsen the debt.

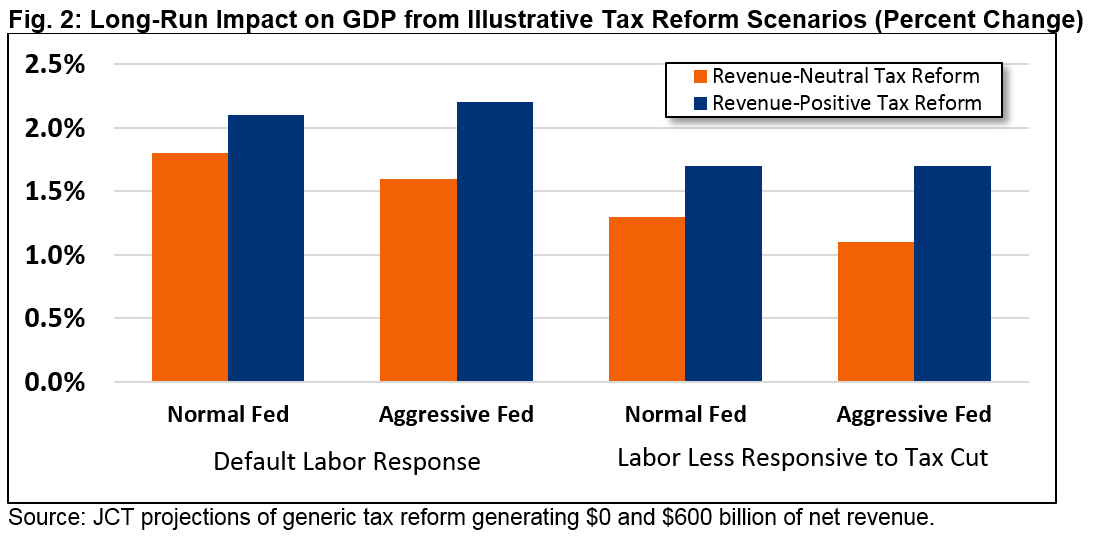

In Five Reasons to Pay For Tax Reform, we explain why tax reform should be paid for. One key reason is that fiscally responsible tax reform is more pro-growth than unpaid-for reform. When JCT modeled two nearly identical reforms with different revenue targets, it found the more fiscally responsible reform grew the economy about a half of a percent more over the long term.

In addition, once the hard deficit neutrality constraint is lifted on tax reform, it makes it easier for policymakers to abandon thoughtful reforms and pursue costly new tax cuts and spending increases that are low-value.

Policymakers must not fall into the trap of trading debt-financed tax cuts for debt-financed spending increases. Instead, they should use tax reform as a jumping off point for further deficit reduction to ultimately put our country’s fiscal house in order.

Set Permanent Tax Policy

Uncertainty has been a defining feature of the past two decades of tax policy. The constantly expiring “tax extenders,” temporary Alternative Minimum Tax patches, sun-setting schedule of tax rates, and a fiscal cliff left businesses and individuals unable to plan for the future. The temporary nature of these policies also allowed policymakers to obscure their debt impact by passing them only one or a few years at a time rather than all at once.

Legislation in 2013 and 2015 added significant permanency to the code, offering much more stability (albeit at great fiscal cost). Tax reform should build on, rather than undermine, this stability. It should do so without adding to the debt.

While the “Byrd Rule” in the Senate disallows the use of the special filibuster-proof reconciliation for legislation that adds to the long-term debt, policymakers should not circumvent that restriction by proposing tax cuts that expire before the decade is over. Doing so would be bad fiscal policy, bad tax policy, and bad economic policy.

Except where there is a true policy justification for temporary provisions, tax reform should propose permanent changes to the tax code that can only be adjusted by a new change in law. It should also deal with remaining temporary “tax extenders” once and for all by repealing, extending, or reforming each of them.

To be sure, there may be a good case for temporary transition rules as a part of tax reform. These rules should be clearly defined and use a path that implies the law will be allowed to take effect rather than including an unrealistic cliff that will prompt another round of extensions.

Avoid Unjustified Timing Shifts, Double Counting, or Other Gimmicks

As with any fiscally responsible piece of legislation, tax reform should not include budget gimmicks that mask its true costs. Allowing tax policy to expire when it is intended to be permanent (as described in the section above) is one example, but other serious timing shifts, double counting, or other games could also obscure the true effects of tax reform.

In the past, timing shifts have been used to make tax legislation appear less costly over a decade even if the revenue losses grow in the long term. These shifts effectively use temporary offsets to finance permanent tax cuts. Some tax changes that would raise more or lose less money up front than in the long term include:

- Converting tax-deferred retirement accounts to Roth-style accounts where taxes are paid up front and withdrawals are tax-free (this would lose revenue in the long term)

- Enacting a one-time “deemed repatriation” on current business income held abroad (this would have little effect on revenue in the long term)

- Lengthening business depreciation schedules to match economic depreciation (this would raise less revenue in the long run than the near term)

- Gradually reducing tax rates rather than cutting them immediately (this would lose more revenue in the long run than the near term)

- Transitioning away from “last-in first-out” (LIFO) accounting for inventory (this would raise less revenue in the long run than the near term)

On the other hand, many policies currently under consideration – including moving to “full expensing” of business investment and disallowing the deductibility of interest on new loans – would raise more or lose less in the long term than in the near term.

In determining whether a timing shift is a “gimmick” or a credible part of tax reform, two questions should be asked. First, is there a tax policy rationale for the change? Second, does the full tax plan maintain or reduce debt levels in the long run? If the answer to either question is no, the policy should not be a part of tax reform.

Of course, other gimmicks also abound. Double counting, for example, should be avoided. If policymakers dedicate some portion of tax reform revenue to the Highway Trust Fund, they cannot use that same revenue to finance tax cuts. The same dollar cannot be used twice.

Similarly, if tax reform raises revenue from the payroll tax to improve the financial state of Social Security, those funds should be used solely for that purpose, not to justify further reductions in the income tax.

Rely on Reasonable Economic Assumptions

Tax reform should be scored and evaluated by JCT and the Congressional Budget Office (CBO) based on their economic growth assumptions. Estimates from the Office of Management and Budget, Treasury, or outside organizations should rely on reasonable economic assumptions in line with CBO and other forecasters. Assuming unachievable growth numbers might make tax reform look easier, but it will make achieving any improvement in the economy harder.

Under CBO’s baseline assumptions, the economy will grow on average by 1.8 percent per year (in inflation-adjusted terms) over the next decade. Though this is significantly slower than historical growth rates, it is consistent with most other public and private forecasts.

Driving slower growth rates is the aging of the population, which tax reform cannot change to any significant degree. Therefore, while it is reasonable to expect tax reform to improve growth somewhat, it is not reasonable to assume it could achieve 3 or 4 percent growth annually. Based on estimates from JCT and Treasury, tax reform is more likely to increase the growth rate to 2 percent annually, if that.

Policymakers may be tempted to assume faster growth because it makes tax reform look easier. With 3 percent growth, policymakers could justify enacting a $3 trillion tax cut without paying for it; with 4 percent growth, they could justify a $5 or $6 trillion tax cut.

These tax cuts, of course, would not pay for themselves. As we’ve explained before, there is little evidence to suggest any major tax cut could pay for itself with economic growth alone. In fact, by adding to the debt in the near term, a tax cut could ultimately cost more than its initial score as higher debt raised interest rates and slowed economic growth. Just a 1-percentage point increase in interest rates would cost $1.6 trillion over a decade. If higher debt led to a reduction in wage growth, further revenue losses would follow.

To be sure, fiscally responsible tax reform can certainly promote economic growth. However, its impact will likely be measured in basis points or decimal points, not percentage points. In any case, gains from growth should go to deficit reduction, not further rate reduction.

Conclusion

Fiscally responsible tax reform is an important part of any comprehensive growth strategy. However, not all tax reform is the same. Policymakers must be willing to at least honestly pay for tax reform and do so while also pursuing entitlement reform. Otherwise, rising levels of debt will stunt economic growth, raise interest rates, and ultimately undermine many of the benefits tax reform provides in the first place.