CBO’s Alternative Long-Term Budget Scenarios

The Congressional Budget Office (CBO) released alternative scenarios to its Long-Term Budget Outlook today. These scenarios show that if the recent tax cuts and spending increases are extended, debt would rise to record levels by 2029 and be more than double the size of the economy by 2048. The report also illustrates how further increasing the deficit would slow long-term economic growth.

CBO’s report shows:

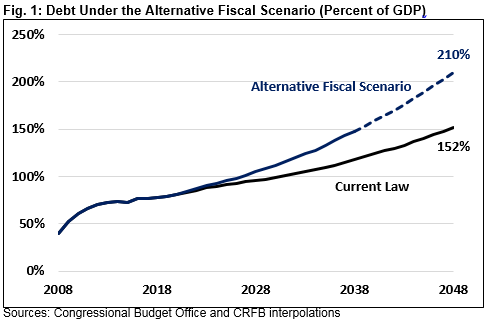

- If lawmakers continue temporary tax cuts and spending increases without offsets, debt would increase from 78 percent of GDP in 2018 to around 210 percent by 2048, compared to 152 percent under current law.

- If these temporary policies are extended permanently, the deficit in 2038 would be 10.5 percent of GDP instead of 7.1 percent under current law. That deficit would be the highest in recent history outside of World War II.

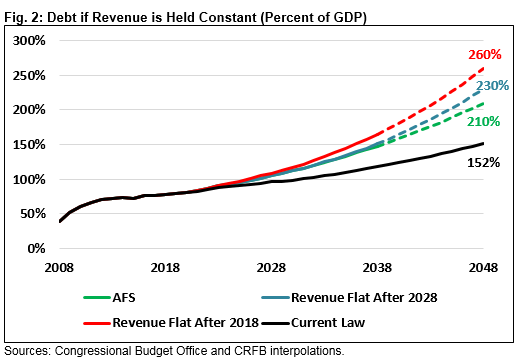

- Debt could even be worse than this scenario. If further tax cuts are enacted to hold revenue flat at its historical average after 2028, debt would reach 230 percent of GDP by 2048. If revenue remains flat at 2018 levels, debt would reach 260 percent by 2048.

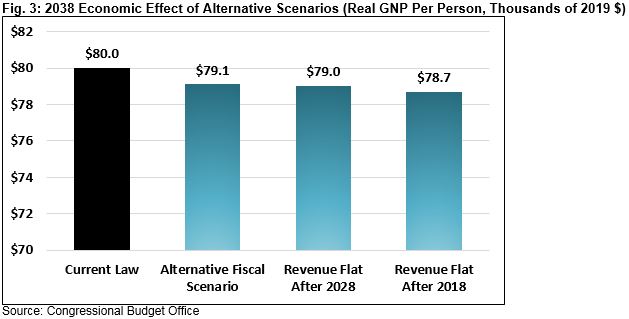

- If lawmakers extend current policies without offsets, the economic drag of debt would shrink real GNP per person by 1.2 percent in 2038, from $80,000 to $79,100.

Lawmakers should not accept ever-growing federal debt as a share of the economy, nor make it worse by continuing deficit-increasing policies. They should take steps to slow and reverse its growth.

Debt in CBO’s Alternative Scenarios

Under CBO’s Long-Term Budget Outlook released in June, debt held by the public will rise from 78 percent of GDP at the end of 2018 to 152 percent of GDP in 2048, an unprecedented level. Today’s report adds an Alternative Fiscal Scenario (AFS), which portrays different policy assumptions than CBO’s current law baseline. Most notably, the AFS assumes the continuation of the deficit-financed tax cuts and spending increases enacted in the last year.

Under the AFS, debt would rise to 210 percent of GDP by 2048, rather than 152 percent.

The AFS contains multiple assumptions different than current law, most of which increase deficits. In addition to extending the individual tax cuts in the 2017 tax law after 2025 and growing discretionary spending with inflation after 2018, the AFS extends other expired and expiring tax breaks and permanently repeals certain health care taxes in the Affordable Care Act that have been temporarily delayed. It also assumes disaster spending is reduced from high levels enacted in response to the 2017 hurricanes, rather than continuing to grow with inflation.

Because recent laws contained so many significant expiring policies, the AFS may represent a picture closer to the status quo than current law.

Both the policy and long-term assumptions significantly increase debt over the long term. Under the AFS, debt exceeds its all-time record of 106 percent of GDP by 2029, reaching 148 percent of GDP by 2038 (instead of 118 percent under current law), and reaching 210 percent by 2048 (instead of 152 percent). This estimate includes the negative effects of high debt on the economy.

CBO also shows what would happen if lawmakers also continue enacting tax cuts to hold revenue constant as a share of GDP. Tax revenues would otherwise grow as a share of the economy because incomes generally grow faster than inflation, pushing taxpayers into higher tax brackets over time.

If lawmakers held revenue at its historical average after 2028, spending would continue to rise steadily, resulting in an even larger gap between the two. This imbalance would result in debt increasing to 151 percent of GDP by 2038 and 230 percent by 2048. If lawmakers held revenue constant at 2018 levels of 16.6 percent of GDP, debt would increase to 165 percent by 2038 and 260 percent by 2048.

The Economic Effect of the Alternative Scenarios

CBO also estimates how each alternative scenario would affect the economy. In short, higher debt dampens long-term economic growth more than the positive effect of lower tax rates boosts it.

Under the AFS, with debt 30 percentage points higher than current law in 2038, real Gross National Product (GNP) per person would be $79,100 that year instead of $80,000 under current law, a 1.2 percent reduction. The reduction would be even greater by 2048, but CBO says its current models are not suited to model debt levels so far outside the nation's historical experience.

The two scenarios with lower revenue would further harm the economy despite reductions in marginal tax rates. Holding revenue flat as a share of GDP after 2028 would reduce real GNP per person by 1.3 percent in 2038 compared to current law, while holding if flat after 2018 would reduce real GNP by 1.7 percent. In dollar terms, real GNP per person would be $1,000 and $1,300 lower under each scenario, respectively.

CBO’s economic analysis takes into account lower marginal tax rates on labor and capital, which encourage work, savings, and investment, boosting the size of the economy. However, federal debt would also be higher, crowding out investment and reducing output. The drag of debt outweighs the positive effects, and the net effect on growth is negative under all three alternative scenarios.

In addition to lower real GNP per person, higher debt would increase interest rates, which CBO estimates would range from 0.2 to 0.4 percentage points higher on ten-year Treasury notes in the three scenarios.

Even these numbers may be too optimistic, since CBO notes the unprecedented future level of the debt represents uncharted territory for its model, which is based on historical experience with federal borrowing. CBO notes the effects of higher debt are “probably understated,” and interest rates and costs would probably be higher than CBO’s models show.

CBO also warns that high and rising debt would lead to “increasing pressure on the noninterest portions of the budget, limiting lawmakers’ ability to respond to unforeseen events, and increasing the likelihood of a fiscal crisis.” In CBO’s estimation, “such a situation would ultimately be unsustainable.”

Conclusion

CBO’s alternative long-term scenarios show the dire path caused by continuing the deficit increases enacted in the past year. If lawmakers act irresponsibly and extend several temporary policies, debt will exceed record levels by 2029.

Lawmakers need to enact a plan that puts debt as a share of the economy on a downward trajectory to ensure fiscal sustainability. Doing so will prevent the scenarios spelled out by CBO from becoming reality.

Appendix: Assumptions Used in Current Law and the Alternative Fiscal Scenario