Analysis of CBO’s Updated Budget and Economic Outlook (June 2017)

The Congressional Budget Office (CBO) released updated budget and economic projections today, continuing to show an unsustainable picture of debt over the next ten years and beyond. CBO found the following:

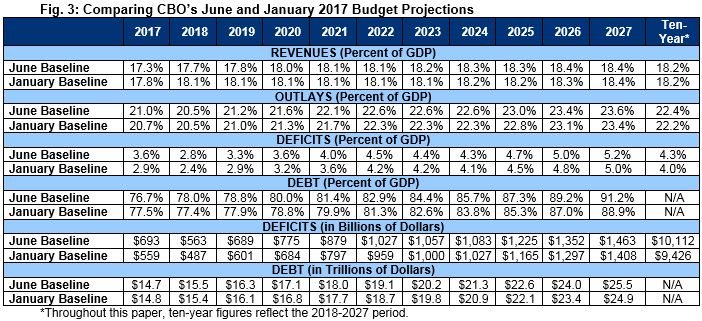

- In 2017, the budget deficit will total $693 billion or 3.6 percent of Gross Domestic Product (GDP). That’s $134 billion above prior projections and the highest since 2012.

- Deficits will grow dramatically over the next decade, with trillion-dollar deficits returning in 2022 and the nominal deficit reaching an all-time high of $1.5 trillion in 2027. Relative to the economy, the deficit will rise from 3.6 to 5.2 percent of GDP.

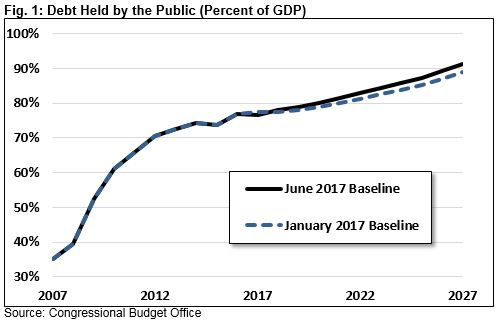

- Debt held by the public will grow by $11.2 trillion between now and 2027, from $14.3 trillion today to $25.5 trillion by 2027. As a share of GDP, debt will rise from its post–World War II era high of 77 percent in 2017 to 91 percent by 2027.

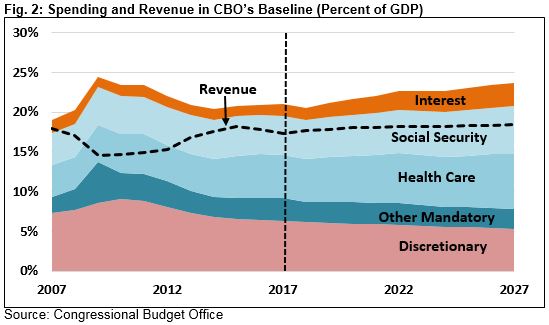

- Spending will grow from 20.9 percent of GDP in 2016 to 23.6 percent in 2027, while revenues will rise from 17.8 percent in 2016 to 18.4 percent by 2027.

- Of the $2.6 trillion of nominal spending growth between 2017 and 2027, 83 percent will come from Social Security, health care, and interest on the debt. Those three budgetary categories will rise in cost from $2.2 trillion (11.8 percent of GDP) in 2017 to $4.4 trillion (15.8 percent of GDP) in 2027.

- CBO’s projections are slightly worse than in January – they project debt to reach 91.2 percent of GDP by 2027, compared to 88.9 percent previously.

- Debt could be far worse than CBO projects. If Congress simply extends various expiring tax cuts and eliminates the sequester, debt would reach 97 percent of GDP by 2027.

CBO’s latest projections continue to show deficits and debt rising over the next decade. This course needs to be corrected, or lawmakers risk harming economic growth, crowding out other spending priorities, and eventually increasing the chance of a fiscal crisis. The projections should serve as a warning shot to those who want to increase debt through tax reform or other initiatives. Rather than add to the debt, we need lawmakers to come together to enact the significant entitlement reforms, spending cuts, and revenue increases necessary to put debt on a sustainable path.

Budget Projections

Under current law, CBO expects debt held by the public to rise continuously over the next decade from today’s post–World War II era record levels. In its projection, debt would rise from nearly 77 percent of GDP in 2017 to 83 percent in 2022 and 91 percent by 2027. In dollar terms, debt will rise from $14.7 trillion at the end of 2017 to $19.1 trillion at the end of 2022 and $25.5 trillion by the end of 2027.

Deficits are projected to widen as well. They will shrink slightly from $693 billion in 2017 to $563 billion in 2018 but then grow to over $1 trillion by 2022 and $1.5 trillion by 2027. As a share of GDP, CBO projects deficits will fluctuate around 3 percent of GDP through 2019 and then rise significantly to 5.2 percent by 2027. The 2027 deficit will be the highest ever in nominal dollars and the sixth-highest deficit as a share of GDP since World War II.

Rising deficits are driven by spending growth that CBO projects will significantly exceed growth in revenue. Spending will rise from 21 percent of GDP in 2017 to 23.6 percent in 2027. Meanwhile, revenue will rise from 17.3 percent of GDP in 2017 to 18.4 percent by 2027.

The vast majority of spending growth over the next decade is the result of rising costs for health care, Social Security, and interest on the debt. These three categories are responsible for 83 percent of nominal spending growth over the next decade and 150 percent of spending growth as a share of GDP (with other budget categories shrinking). CBO projects Social Security will grow from 4.9 percent of GDP in 2017 to 6 percent by 2027, federal health spending will grow from 5.4 percent to 6.9 percent, and interest will grow from 1.4 percent to 2.9 percent.

On the revenue side, individual income taxes will increase from 8.2 percent in 2017 to 9.7 percent by 2027. However, payroll tax, corporate tax, and other revenue collection – particularly from the Federal Reserve – will decline from 9.1 to 8.7 percent of GDP, partially offsetting these gains.

It is worth noting that policymakers could make these numbers worse if they enact policies that differ from the assumptions in CBO’s baseline. For example, if Congress extends tax provisions that expired at the end of last year or will expire in the future and enacts an unpaid-for repeal of the automatic spending reductions known as the sequester, ten-year deficits would increase by $1.7 trillion (from $10.1 trillion to $11.8 trillion) and result in debt in 2027 reaching 97 percent of GDP (instead of 91 percent).

Changes in Budget Outlook

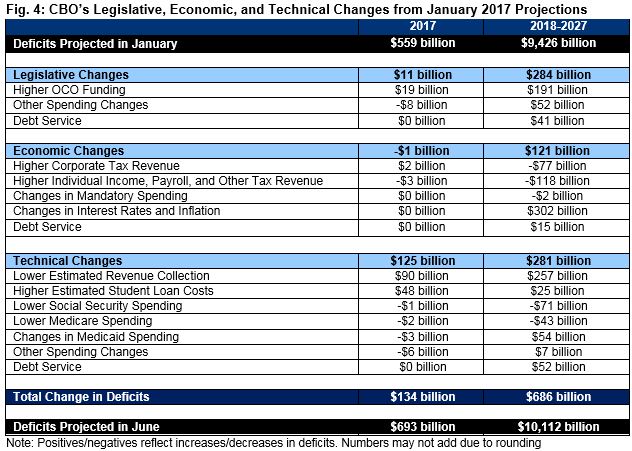

CBO’s budget and economic projections are updates to the agency’s January projections. Compared to January, the latest projections show higher debt and deficits over the next ten years.

More specifically, CBO currently projects debt will be 91.2 percent of GDP in 2027 compared to 88.9 percent projected in January. It also projects ten-year deficits of 4.3 percent of GDP ($10.1 trillion) compared to the previous projection of 4 percent of GDP ($9.4 trillion).

The higher debt level in 2027 is the result of $134 billion in higher deficits in 2017 and $686 billion in higher deficits over the 2018-2027 period.

In 2017, deficits are now projected to total $693 billion, compared to $559 billion in January. This increase of nearly one-quarter is largely attributable to unexpectedly weak tax collections in recent months, recent appropriations legislation, and higher estimates of the cost of past student loans. Overall, revenues in 2017 will be $89 billion lower than projected in January while spending will be $45 billion higher.

Over the next decade, changes in economic projections are one contributor to this deteriorated fiscal outlook. While CBO projects higher projections for wages and taxable corporate profits will boost revenues by about $195 billion over the next decade, it also expects changes in interest rates and inflation will increase spending by $302 billion over the same period. Along with other smaller economic changes, the net result is $121 billion in more debt by 2027.

Technical changes, meanwhile, are responsible for $281 billion in additional borrowing over the next decade. Most significantly, CBO believes recent weak revenue collections will continue for several years before gradually declining. CBO now also projects higher spending on government loan programs, Medicaid, and other programs, offset slightly by lower spending on Social Security and Medicare.

Finally, legislative changes since January will add $284 billion to the debt over the next ten years. Most of this increase is the result of an extra $19 billion appropriated toward overseas contingency operations (OCO) in 2017. CBO assumes Congress will continue to appropriate similar amounts, adjusted for inflation, in future years.

Economic Projections

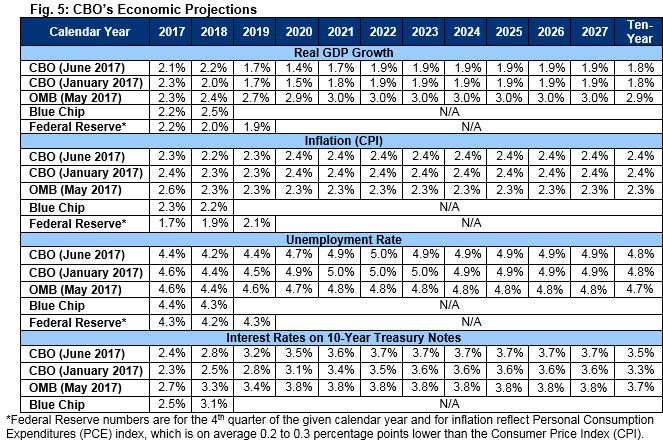

CBO’s newest baseline includes an update of its economic projections, which were last made in January. Overall, economic growth projections are quite similar, particularly over the long term.

CBO projects real GDP growth of 2.1 percent this year and 1.8 percent over the long term. The 2017 estimate is slightly lower than the 2.3 percent growth expected in January, but the long-term estimate has changed only slightly. CBO’s growth projections are in line with the Blue Chip and Federal Reserve forecasts.

Notably, CBO’s projected long-term growth rate of 1.9 percent – though similar to most outside forecasters – is significantly lower than the 3 percent assumed by the Office of Management Budget (OMB). CBO explains that long-term growth is constrained by relatively slow labor force growth because of the ongoing retirement of the baby boomers. OMB’s 3 percent projections do not appear justified by economic evidence and are far outside the mainstream.

In terms of unemployment, CBO has revised down its near-term projections. In January, they projected 4.6 percent unemployment this year and 4.4 percent next year. In this report, CBO projects an unemployment rate of 4.4 and 4.2 percent, respectively. Over the long run, CBO projects unemployment to be just above its natural rate at about 5 percent.

The biggest change in CBO’s economic projections is related to interest rates. Interest rate projections are now higher in both the short term (as the Fed is expected to raise interest rates faster than CBO expected in January) and over the long term, reflecting an increase in the demand for long-term bonds.

Some private-sector forecasters are predicting larger increases in long-term interest rates. However, CBO estimates much of that increase is due to expectations about future changes in law. If policymakers added substantially to debt, interest rates would increase. Since CBO’s baseline is based on current law, CBO does not include in its projections higher interest rates as a result of Congress possibly adding to debt.

Conclusion

CBO’s newest baseline shows a worse picture than its previous projections, with deficits and debt rising over the next decade even faster than previously predicted. Coupled with the long-term outlook released in March, the agency shows a dramatic rise in debt as a share of the economy in the coming decades. This increase will be driven by increasing costs for Social Security, health care, and interest on the debt combined with insufficient revenue.

The publication of these projections comes at a time when lawmakers in Congress are debating whether tax cuts and some spending increases should be added to the debt rather than paid for. Today’s projections should put an end to this discussion. Trillion-dollar deficits are projected to return by 2022, and the debt is projected to reach 91 percent of GDP by 2027. Even borrowing to pay for “current policies” would bring the debt to 97 percent of GDP. This would be unacceptable.

Instead of adding to debt, policymakers should work on the necessary entitlement and tax reforms to put debt on a sustainable path. That would ensure a much brighter fiscal and economic future than allowing debt to rise to unprecedented levels.