Analysis of the 2018 Social Security Trustees’ Report

The Trustees for Social Security released their annual report today. As they have for many years, their projections show that the Social Security program faces a large and growing funding imbalance that must be addressed promptly to prevent across-the-board benefit cuts or abrupt changes in tax or benefit levels. This year’s report shows:

- Social Security Will Run Permanent Deficits. For the first time since 1982, the program will spend more than it raises in revenue and collects in interest. The gap will total $900 billion over a decade. On a cash-flow basis, Social Security will run a deficit of $85 billion this year and $1.7 trillion over the next decade.

- Social Security Faces Large Long-Term Imbalances. The Trustees estimate Social Security faces a 75-year shortfall of 2.84 percent of payroll (1.0 percent of GDP), growing to 4.32 percent of payroll (1.5 percent of GDP) by 2092. That means payroll taxes will need to be increased by 22 percent or scheduled benefits cut by a sixth (or some combination) to ensure 75-year solvency; ultimately, taxes will need to be increased by a third or benefits reduced by 26 percent.

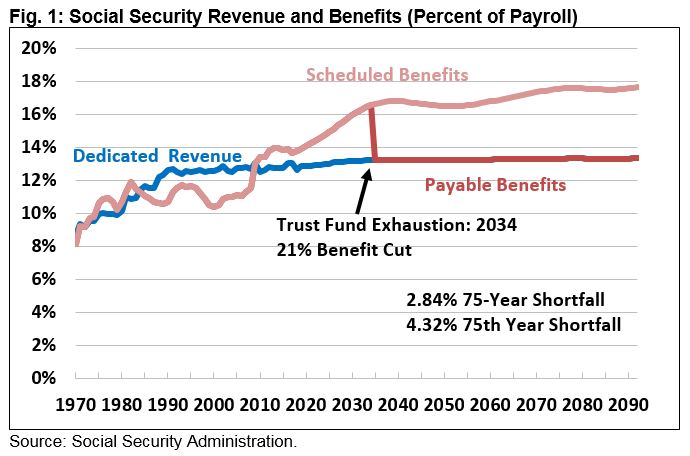

- Social Security Will Be Insolvent by 2034. The Trustees project depletion of the Disability Insurance trust fund by 2032 and the Old-Age & Survivors Insurance trust fund by 2034. On a theoretical combined basis, the trust funds will run out by 2034 – the same as last year’s projections. At the time of insolvency, all beneficiaries will face a 21 percent across-the-board benefit cut.

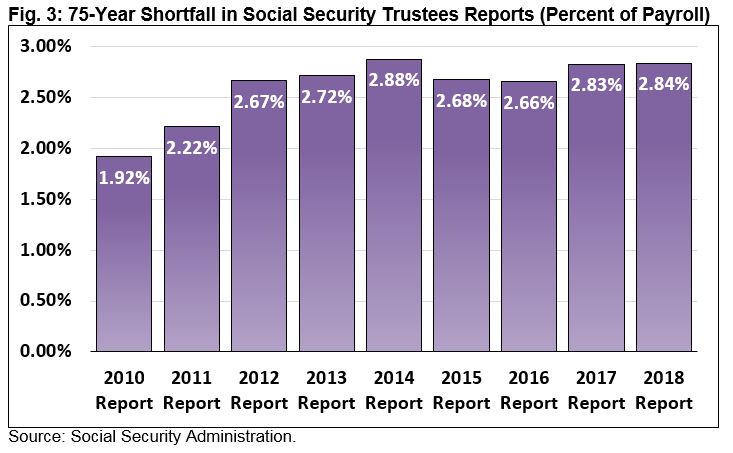

- The Problem Is Similar To Last Year, But Has Deteriorated This Decade. Social Security’s 75-year shortfall rose from 1.92 percent of payroll in 2010 to 2.83 percent last year and 2.84 percent this year. The 2034 insolvency date is the same as projected last year, but three years earlier than projected in 2010.

- Lawmakers Should Start Making Changes Now. Social Security insolvency is not that far away – when today’s 51-year-olds reach the normal retirement age and today’s youngest retirees turn 78. Waiting 16 years to act would mean any tax hikes or benefit cuts have to be 35 to 40 percent larger.

Protecting Social Security’s solvency is vitally important for the country’s overall fiscal outlook and the 86 million beneficiaries who will be on the program when the trust funds are exhausted in 2034. Swift action is needed to prevent seniors, surviving dependents, and people with disabilities from facing abrupt cuts in just a few years.

Social Security Faces a Large and Growing Shortfall

The Social Security Trustees project the program will run permanent deficits until the trust fund is exhausted. Including interest, spending will exceed income for the first time since 1982 this year, and deficits will total about $900 billion over the next decade. On a cash-flow basis, deficits will total $85 billion this year and $1.7 trillion over the next decade.

Over the longer term, the Trustees project Social Security’s cash shortfall (assuming full benefits are paid) will grow from 1.2 percent of payroll (0.4 percent of GDP) this year to 2.8 percent of payroll (1.0 percent of GDP) by 2030, 3.6 percent of payroll (1.3 percent of GDP) by 2040, and 4.3 percent of payroll (1.5 percent of GDP) by 2092.

This rising shortfall is the result of continued benefit growth – due to the aging of the population – but also a lack of equally robust revenue growth. The program’s costs have risen from 10.4 percent of payroll in 2000 to 13.8 percent of payroll today and are projected to rise further to 16.0 percent of payroll by 2030 and 17.7 percent of payroll by 2092. Revenue will rise only slightly, from 12.6 percent of payroll this year to 13.4 percent of payroll by 2092.

Generally, the Trustees measure Social Security's financial imbalance over 75 years. They find the program faces an actuarial shortfall of 2.84 percent of payroll (slightly over 1 percent of GDP). This means 75-year solvency would require the equivalent of immediately raising the payroll tax by just over one-fifth – from 12.4 to 15.2 percent. Alternatively, solvency could be achieved by reducing benefits by one-sixth – effectively cutting the average annual benefit from $20,660 to $17,000 for an individual retiring this year at the normal age. Maintaining sustainable solvency in the 75th year requires raising the payroll tax by one-third (from 12.4 to nearly 17 percent) or cutting benefits by 26 percent (average benefit reduced from $52,000 to $38,500 in 2092).

Social Security Is Headed Toward Insolvency

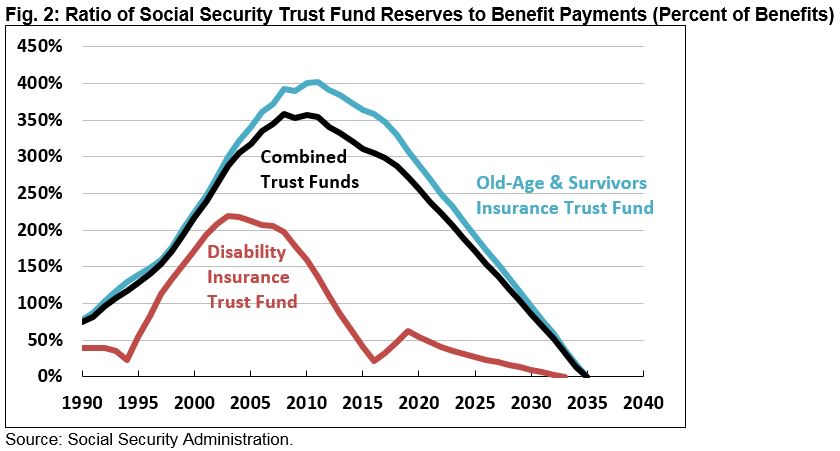

As Social Security’s deficits grow, it will increasingly fund benefits out of its reserves. Ultimately, those reserves will be depleted, and all beneficiaries will face a large across-the-board benefit cut.

The Social Security Disability Insurance (SSDI) trust fund is projected to be exhausted by 2032, while the Old-Age & Survivors Insurance trust fund is projected to deplete its reserves by 2034. On a theoretical combined basis – assuming revenue is reallocated between the funds in the few years between SSDI and OASI insolvency – Social Security will become insolvent by 2034.

2034 is not that far away. Under the Trustees’ projections, the trust funds would run out of reserves when today’s 51-year-olds reach the normal retirement age and today’s youngest retirees turn 78. At that point, every beneficiary regardless of age or income would face an across-the-board 21 percent benefit cut. That reduction will grow to 26 percent by the end of the 75-year projection window.

Based on our interactive tool How Old Will You Be When Social Security’s Funds Run Out?, the across-the-board cut would mean lifetime benefits will be $110,000 lower for an average 50-year-old and $190,000 for a typical 20-year-old.

Social Security’s Finances Have Deteriorated Since 2010

Social Security’s finances have gotten significantly worse since the beginning of the decade. In 2010, the Trustees estimated the trust funds would be exhausted by 2037 and the program faced a 75-year shortfall of 1.92 percent of payroll. That shortfall rose to 2.22 percent in 2011, mostly stabilized at about 2.7 percent between 2012 and 2016, and now totals 2.84 percent. Meanwhile, the projected exhaustion date has been accelerated to 2034, meaning the trust funds are more than a decade closer to insolvency than back in 2010.

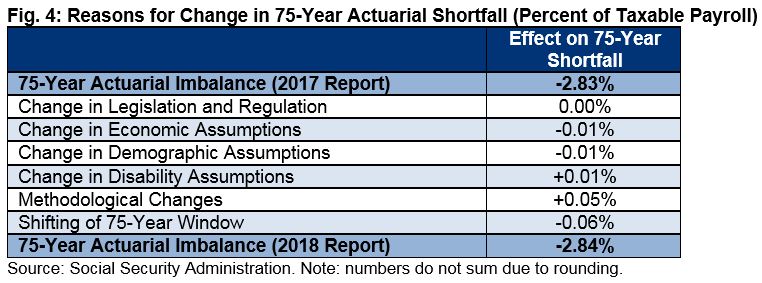

While the program’s finances have worsened since 2010, they have changed very little compared to last year. The Trustees project no change in the theoretical combined trust fund exhaustion date of 2034, similar aggregate deficits, and a 75-year actuarial shortfall of 2.84 percent of payroll as opposed to 2.83 percent of payroll last year.

This small increase in the 75-year shortfall is entirely due to the shifting of the projection window, which adds 2092 to the projection period. This shift adds 0.06 percent of payroll to the 75-year deficit. Other changes slightly reduce the shortfall.

The largest change is a 0.05 percent reduction in the shortfall due to methodological improvements. These include changes to projections for mortality rates, labor force participation among women in their 40s and 50s, projections of female old-age enrollees, initial benefits, taxation of benefits, and retroactive benefits for disabled workers.

The long-term assumptions for economics, demography, and disability are unchanged from last year’s report, though each have near-term changes based on updated data.

Changes in economic assumptions add 0.01 percent to the actuarial shortfall. These changes include a 1 percent reduction in potential GDP throughout the projection period, a near-term reduction in interest rates, and a near-term reduction in the ratio of taxable payroll and labor compensation to GDP.

Changes in demographic assumptions add another 0.01 percent to the 75-year shortfall. Changes include a lower fertility rate, higher mortality rates, and changes to immigration and population projections as a result of new data.

Changes in disability assumptions reduce the 75-year shortfall by just 0.01 percent of payroll but have a more significant near-term effect in moving the SSDI insolvency date back four years –from 2028 to 2032. These changes are due to lower near-term disability incidence rates and lower average benefits based on recent data.

Though recent legislation had a significant effect on the federal budget overall, it had little effect on Social Security’s finances specifically. The Trustees note that the Trump Administration’s rollback of the Deferred Action for Childhood Arrivals (DACA) program will cause a negligible increase in the actuarial deficit. In addition, the 2017 tax law will cause a negligible decrease since repeal of the individual mandate and the temporary reduction in individual tax rates will have offsetting effects, increasing taxable payroll but temporarily reducing taxation of benefits.

Delaying Fixes to Social Security is Costly

With insolvency only 16 years away, prompt action is needed to make Social Security solvent – not just for today’s children and workers, but for many of today’s retirees.

Delaying necessary solvency improvements not only puts beneficiaries at risk, but it limits the ability of policymakers to phase in changes gradually and gives today’s workers less time to plan for any changes in taxes or benefits. Delaying reforms also places an unfair and disproportionate burden on younger and future generations.

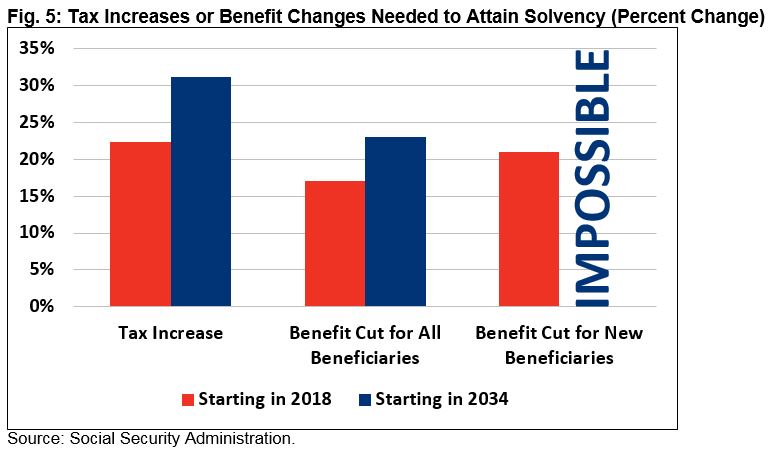

Perhaps most troubling, delaying reform actually increases the magnitude of necessary changes. To achieve 75-year solvency today, for example, lawmakers could immediately raise the Social Security payroll taxes by 22 percent, or 2.8 percentage points. If lawmakers wait until 2034, they would have to increase the payroll taxes by 31 percent, or 3.9 percentage points.

Similarly, Social Security solvency could be achieved with a 17 percent across-the-board benefit cut today, which would rise to 23 percent if they wait until 2034. If benefit reductions applied only to new beneficiaries, cuts would need to be 21 percent today; even eliminating benefits for new beneficiaries in 2034 would not be enough to avoid insolvency.

Importantly, even with an immediate payroll tax increase or benefit cut large enough to make the program solvent, cash-flow deficits could return and the program could quickly fall out of balance (for example, with a 2.8 percentage point payroll tax increase deficits would return by about 2030). This is why policymakers should look beyond simply keeping the program solvent for 75 years and pursue “sustainable solvency” to bring the program into ultimate cash balance.

Conclusion

This year’s report serves as a reminder: Social Security’s shortfall needs to be addressed soon. Failure to act would result in all beneficiaries receiving a 21 percent across-the-board benefit cut when the combined trust fund exhausts in just 16 years, when today’s 51-year-olds reach the normal retirement age.

Most of the options to fix Social Security’s finances are well-known and could be easily enacted and implemented with political will. Our Social Security Reformer tool allows anyone to design their own comprehensive reform package.

Any reforms to Social Security should achieve sustainable solvency so that the program is financially sound for 75 years and beyond. But solvency shouldn’t be the sole goal of reform. A thoughtful Social Security plan should be designed to improve retirement security, improve fairness, meet desired distributional goals, make improvements for workers with disabilities, and promote long-term economic growth.

Encouragingly, policymakers are starting to test some of the changes for Disability Insurance that we published in the McCrery-Pomeroy SSDI Solutions Initiative’s book SSDI Solutions. Specifically, the Department of Labor recently requested proposals for the RETAIN project, which will test strategies to help people with disabilities return to work based on Washington state’s experience. Other reforms, like those proposed in the President’s budget, should also be explored.

These reforms, along with others to the old-age program, can strengthen Social Security and promote economic growth at the same time. Increasing labor force attachment, promoting delayed or more flexible retirement, encouraging more retirement savings, and shrinking the gap between dedicated revenue and benefit outlays could all help boost the economy – which is likely to experience slow growth as a result of the aging population.

Thoughtful reforms enacted today can still promote growth, assure solvency, protect or enhance benefits for those who need them, and give workers and taxpayers time to plan and adjust. But it is already too late to fix Social Security through easy incremental changes. Waiting another fifteen, ten, or even five years to act will continue to limit available options and put Social Security at risk. As the Trustees said, “with informed discussion, creative thinking, and timely legislative action, Social Security can continue to protect future generations.”

Tags

What's Next

-

Image

-

Image

-

Image