Primer: Understanding the Tax Gap

Note: This is an update of our Tax Gap Primer using the latest available data from the IRS.

One of the most fair and efficient ways for policymakers to raise revenue would be to close some portion of the “tax gap.” The tax gap is the difference between taxes paid and taxes owed by law. In this primer, we answer the following questions:

- How Big is the Tax Gap?

- Why Is There a Tax Gap?

- Which Unpaid Taxes Contribute to the Tax Gap?

- Who Contributes to the Tax Gap?

Reducing the tax gap could raise additional revenue without increasing taxes and should be a key legislative priority for both parties. In future pieces, we will discuss ideas and options for how to close it.

How Big is the Tax Gap?

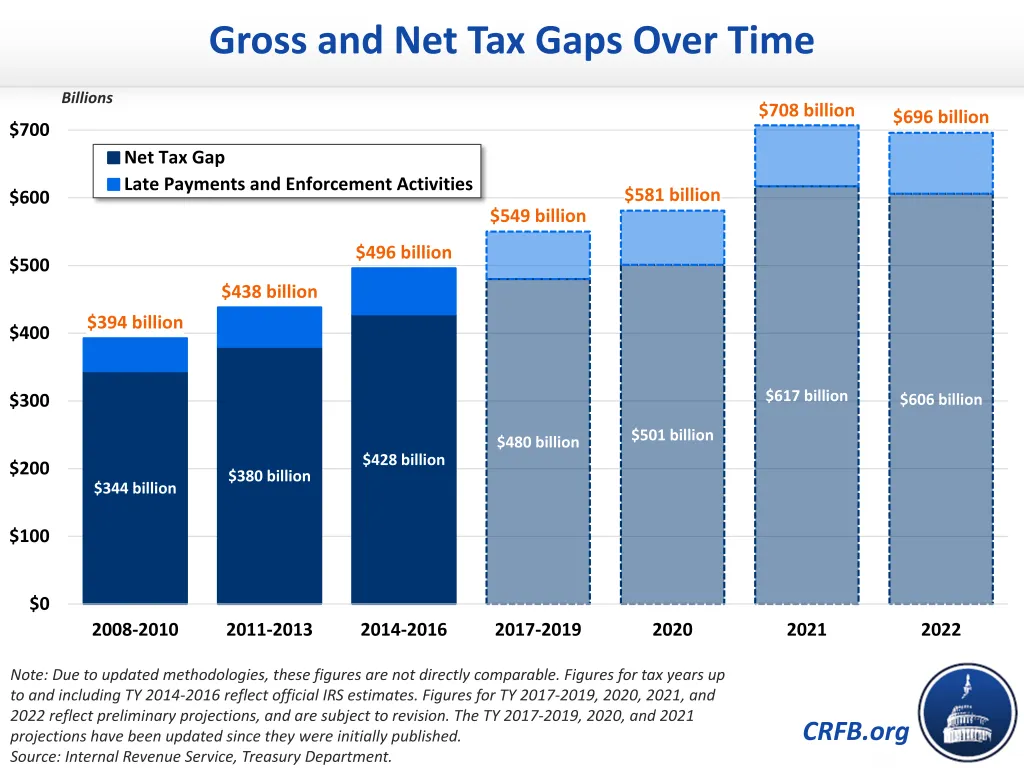

The Internal Revenue Service (IRS) recently projected a "gross tax gap" of $696 billion in tax year 2022, with over $4.6 trillion of taxes owed but only about $3.9 trillion paid voluntarily and on time. After accounting for $90 billion of additional revenue from IRS enforcement activities and late payments, they estimate the “net tax gap” totaled $606 billion in 2022, which is 2.3 percent of 2022 Gross Domestic Product (GDP), or 13.1 percent of total tax revenue owed.

The detailed analysis published by the IRS includes data for tax years 2014 through 2022. Over that period, the gross tax gap averaged $569 billion per year (15 percent of total taxes owed), while the net tax gap averaged $494 billion (13.1 percent of total taxes owed). The data for tax years 2014-2016 reflect an official, data-based “estimate” of the tax gap, whereas the data for tax year 2017 and onwards are “projections”, meaning they have temporary assumptions built into their modeling and are more likely to be adjusted in the coming years (the analysis includes revised projections for tax years 2017 through 2021).

However, none of these estimates include non-filing of corporate income taxes, which the IRS has never been able to accurately estimate. Furthermore, these estimates still may not accurately account for contributions to the tax gap from non-standard sources of income that have emerged in the past decade, such as work and transactions in the gig economy or cryptocurrency trading.

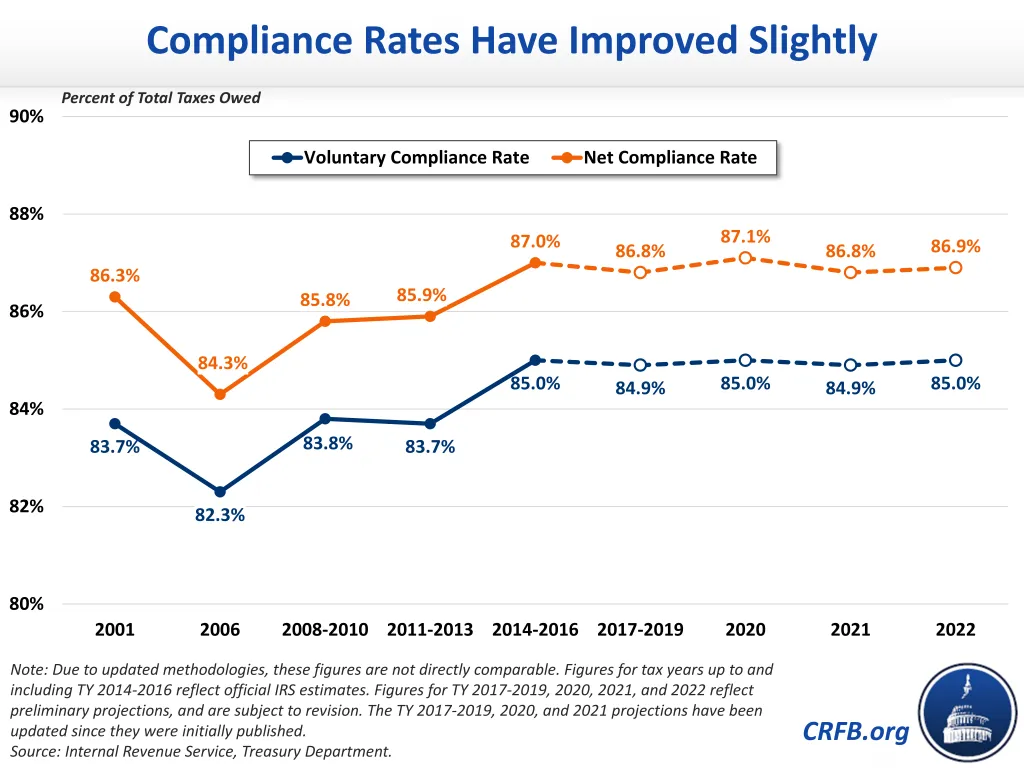

One way to measure the size of the tax gap is as a share of total taxes owed. The Voluntary Compliance Rate (VCR) describes what share of taxes is paid voluntarily (corresponding to the gross tax gap), while the Net Compliance Rate (NCR) describes the share of taxes ultimately collected after accounting for late payments and IRS enforcement actions (corresponding to the net tax gap).

For tax year 2022, the IRS projects the VCR was 85 percent, while the NCR was just shy of 87 percent – meaning late payments and enforcement only increased compliance by about two percentage points and over 13 percent of taxes owed remain uncollected. These compliance rates are roughly in line with previous IRS tax gap analyses – though both VCR and NCR are up by about one percentage point on average over the past decade compared to tax years 2011 through 2013.

Importantly, the figures above may be in some ways incomplete. Incorporating certain offshore funds and passthrough evasion methods, a 2021 report from the Department of the Treasury estimated that the true tax gap in tax year 2019 could have been $46 billion more than the standing IRS estimate.

The process of estimating the tax gap is extremely complex and time consuming, which is why the IRS’s official estimates feature a significant lag and figures for more recent years are only “projections”. However, the IRS frequently updates its methodology in order to provide more accurate and timely estimates of the tax gap going forward.

Others have estimated that the tax gap could be even larger than the IRS projects. In a 2019 paper, economists Larry Summers and Natasha Sarin estimated that the gross tax gap would total approximately $7.5 trillion from 2020 through 2029, averaging $750 billon per year. In 2021, then IRS Commissioner Charles Rettig estimated that the true tax gap could be as large as $1 trillion per year if newer and more elusive sources of income were included, such as trading in cryptocurrencies, foreign-sourced income, and business income improperly passed through as individual income.

Why Is There a Tax Gap?

Taxes are underpaid for one of three reasons – either tax returns are never filed, taxes owed are underreported, or taxes are accurately reported but underpaid.

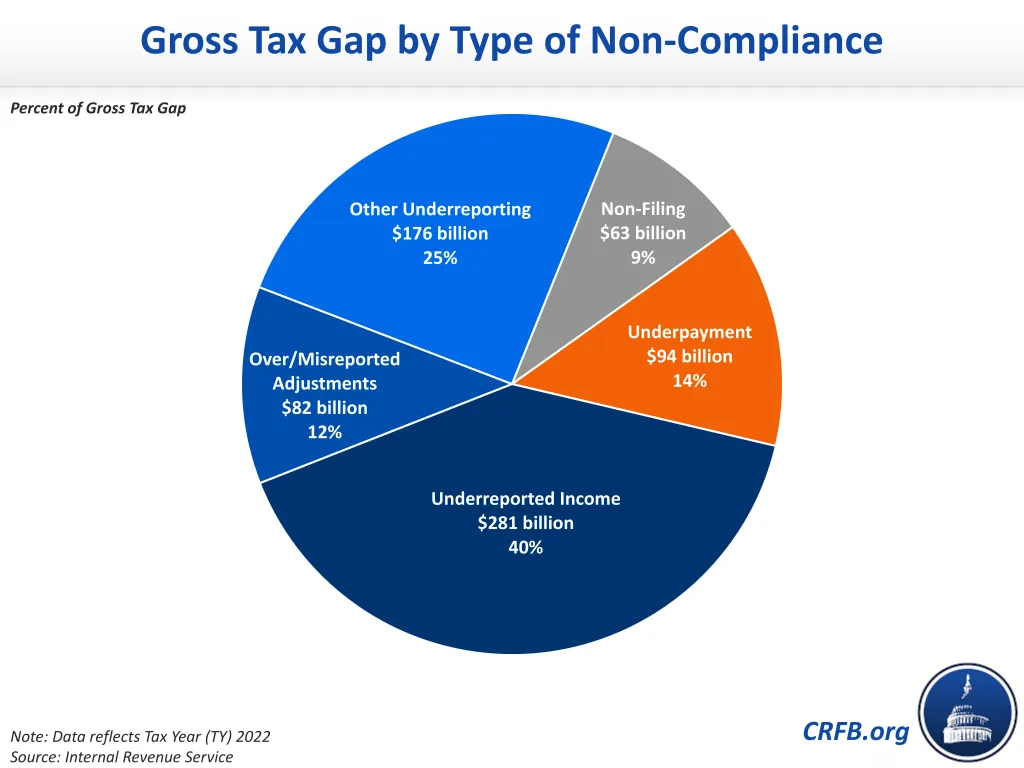

According to IRS projections for tax year 2022, 9 percent of the gross tax gap comes from non-filing, 14 percent comes from underpayment, and 77 percent comes from underreporting – with at least 40 percent due to underreporting of income and at least 12 percent due to over-reporting or misreporting of adjustments (the remaining 25 percent is not defined).

Non-filing occurs when an individual or business that earned taxable income and should have filed a tax return with the IRS fails to do so. In 2022, the non-filing gap was $63 billion, or 9 percent of the gross tax gap, with the vast majority coming from individual income tax filers.1

Underpayment occurs when an individual or business that did file a tax return with the IRS fails to pay all the taxes it owes on that return. In 2022, the underpayment gap was $94 billion, or 14 percent of the gross tax gap. Again, the vast majority of this gap comes from individual income tax filers.2

By far the biggest contributor to the tax gap is underreporting, or when an individual or business files a tax return that incorrectly underreports the taxes it owes in a given year. In 2022, the underreporting gap was $539 billion, or 77 percent of the gross tax gap.

Of the $539 billion in estimated underreporting in 2022, $381 billion comes from individual income taxes, $111 billion from payroll taxes, $44 billion from corporate income taxes, and $2 billion from the estate tax.

Nearly three-fourths of individual underreporting comes from underreporting of income – $194 billion from business income and $87 billion from non-business income – and just over one-fifth comes from overreporting or misreporting of various adjustments (the rest comes from interactions and other effects).

Of the $82 billion that comes from overreporting or misreporting of various adjustments, $24 billion comes from the Earned Income Tax Credit (EITC); $17 billion from the Child Tax Credit (CTC); $6 billion from education-related and other tax credits; $7 billion from misreporting of filing status; and the remaining $27 billion from other deductions, exemptions, and adjustments.3

Which Unpaid Taxes Contribute to the Tax Gap?

Approximately 74 percent of the overall 2022 gross tax gap comes from the individual income tax, 18 percent comes from payroll taxes, and 8 percent comes from the corporate income tax and other taxes.

In 2022, the individual income tax accounted for $514 billion, or 74 percent, of the $696 billion gross tax gap. After accounting for $68 billion from late payments and enforcement, individual income taxes accounted for $447 billion of the $606 billion net tax gap.

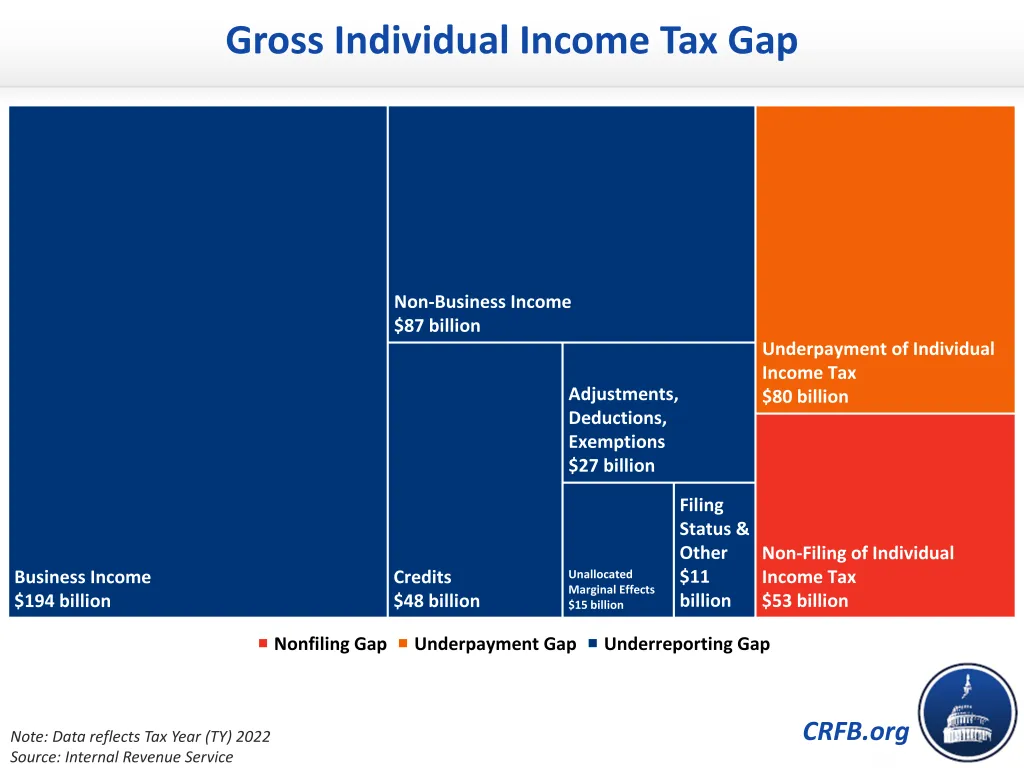

Of the $514 billion gross individual income tax gap, $53 billion was due to non-filing (about 10 percent), $80 billion was due to underpayment (about 16 percent), and $381 billion was due to underreporting (about 74 percent). Within that $381 billion of underreporting, $194 billion – just over half – was attributable to taxes on “pass-through” business income. Another $87 billion came from non-business income; $48 billion from overpayment of credits; $27 billion from awarded adjustments, deductions, and exemptions; and $26 billion from incorrect filing statuses, other taxes, and unallocated marginal effects.

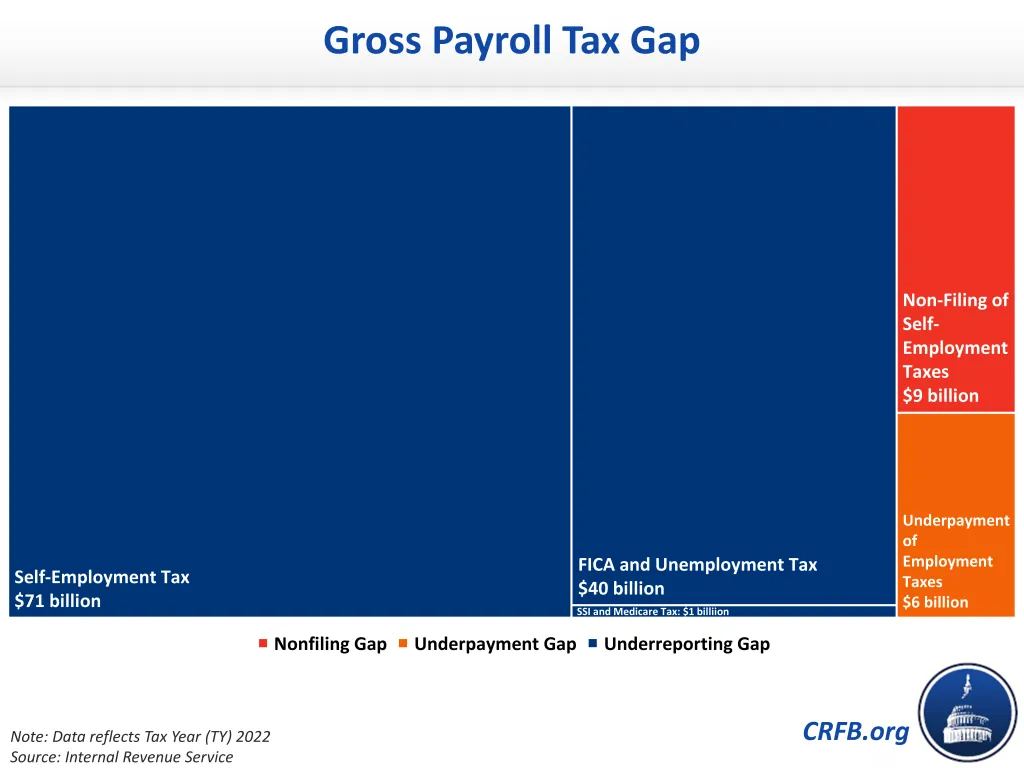

Unpaid payroll taxes account for $127 billion of the gross tax gap in 2022, or $119 billion of the net tax gap. Of the gross amount, $9 billion was due to non-filing (about 7 percent), another $6 billion was due to underpayment (nearly 5 percent), and $111 billion was due to underreporting (over 87 percent).

Most payroll taxes that went unpaid in 2022 – including $71 billion from underpayments and $9 billion from non-filing – came from self-employment taxes paid by small business owners, sole proprietors, and independent contractors. Underreported and underpaid employee and employer payroll taxes made up another $40 billion and $6 billion, respectively.

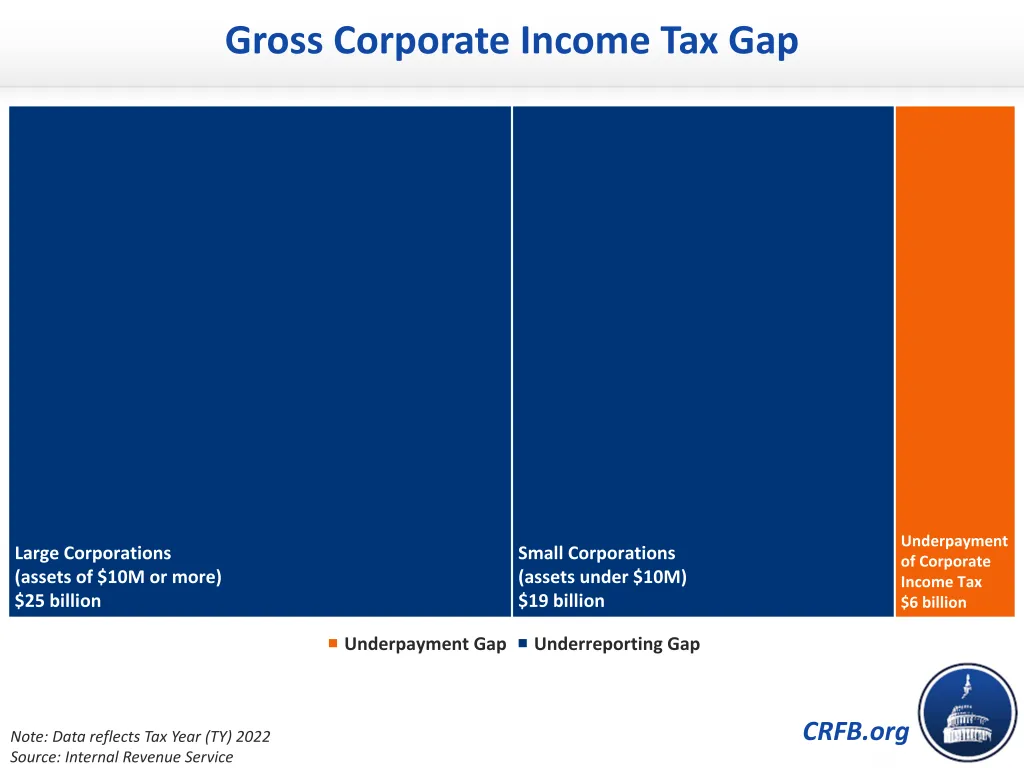

Meanwhile, the corporate income tax accounted for $50 billion of the gross tax gap, or $40 billion of the net tax gap after $10 billion of late and recovered payments.

This gross figure includes $6 billion due to underpayment (12 percent) and $44 billion due to underreporting (88 percent). The IRS breaks this number down further into underreporting of corporate income taxes from “small corporations” with assets of less than $10 million and underreporting of corporate income taxes from “large corporations” with assets of $10 million or more, which accounted for $19 billion and $25 billion, respectively.

Because the IRS currently lacks an accurate method for estimating unpaid taxes due to non-filing of corporate income tax returns, the actual figures may differ significantly.

Finally, a very small part of the overall gross tax gap comes from unpaid estate taxes and, to a much lesser extent, unpaid excise taxes. In 2022, unpaid estate and excise taxes contributed approximately $5 billion to the gross tax gap, or less than 1 percent. Like most other categories of tax, most unpaid estate taxes are due to underreporting, representing $2 billion per year. Underpaying and nonfiling of estate taxes each contribute about $1 billion to the gross tax gap. Unpaid excise taxes represent less than $500 million.

Unlike most other categories of tax, however, the majority of estate taxes that were not paid in a timely manner – more than 90 percent – were eventually collected through late payments or enforcement activities. This means that only $400 million of the $606 billion net tax gap from 2022 came from estate taxes.

Who Contributes to the Tax Gap?

As projected for 2022, most of the gross tax gap – 61 percent by our estimate – comes from unpaid or underpaid business and self-employment income taxes, the vast majority of which comes from pass-through entities such as sole proprietorships, partnerships, and S corporations.

We estimate only 31 percent of the tax gap comes from taxation of wages and other ordinary income, even though this category covers the majority of taxable income and taxes paid.

Another 8 percent of the tax gap comes from capital income, along with some other taxes and adjustments.

That so much of the tax gap comes from business income – and pass-through income in particular – is a consequence of the way these entities report their taxes. While taxes are withheld from wages when they are paid and are at least reported for most other types of ordinary and capital income, business income (and especially self-employment income) is effectively reported on a voluntary basis with little, if any, third-party verification.

As an example, the IRS estimates wages and salaries, which are subject to substantial information reporting and withholding, have a one percent misreporting rate, while sole-proprietor business income, which is subject to little or no information reporting, has a misreporting rate closer to 55 percent.

* * * * *

Nearly $700 billion in taxes owed to the federal government are not paid on-time each year, resulting in more than $600 billion of revenue loss. Nearly four-fifths of those unpaid taxes are due to underreporting, almost three-fourths are individual income taxes and three-fifths come from business and self-employment income, mainly from self-employed workers and pass-through entities. The vast majority of the tax gap is associated with income or tax breaks where there is no withholding and little information reporting.

Policymakers should work together to enact legislation to reduce the tax gap and improve tax compliance.

1 To measure the non-filing tax gap, the IRS first identifies all individuals who did not appear as primary or secondary taxpayers on a timely or late-filed return (using a process it calls the Administrative Data Method), then assembles comprehensive data for these individuals from third-party reporters. It then assigns these individuals to hypothetical tax units, which are stratified to correspond with aggregate income distributions observed in Census data. Finally, the IRS estimates the tax liability of those non-filers who likely did earn taxable income and subtracts from that an estimate of the tax those individuals likely did pay through withholding and other means.

2 Of the three types of noncompliance, underpayment is by far the easiest for the IRS to estimate because all the income in question has already been made visible to the IRS through filed tax returns. To measure the underpayment gap, the IRS simply calculates the difference between the amount of taxes owed as reported on returns and the amount of taxes paid on time.

3 The underreporting gap is the most difficult of the three to estimate. The IRS primarily relies upon actual audit data taken from a stratified, random statistical sample of tax returns performed under a program called the National Research Program (NRP). Unlike typical compliance or risk-based audits, NRP audits are broad in scope and meant to glean as much information as possible, which then helps inform the IRS’s risk-based audit selection tools and other compliance efforts.