CBO Estimates TCJA Extensions Could Cost Up to $2.7 Trillion

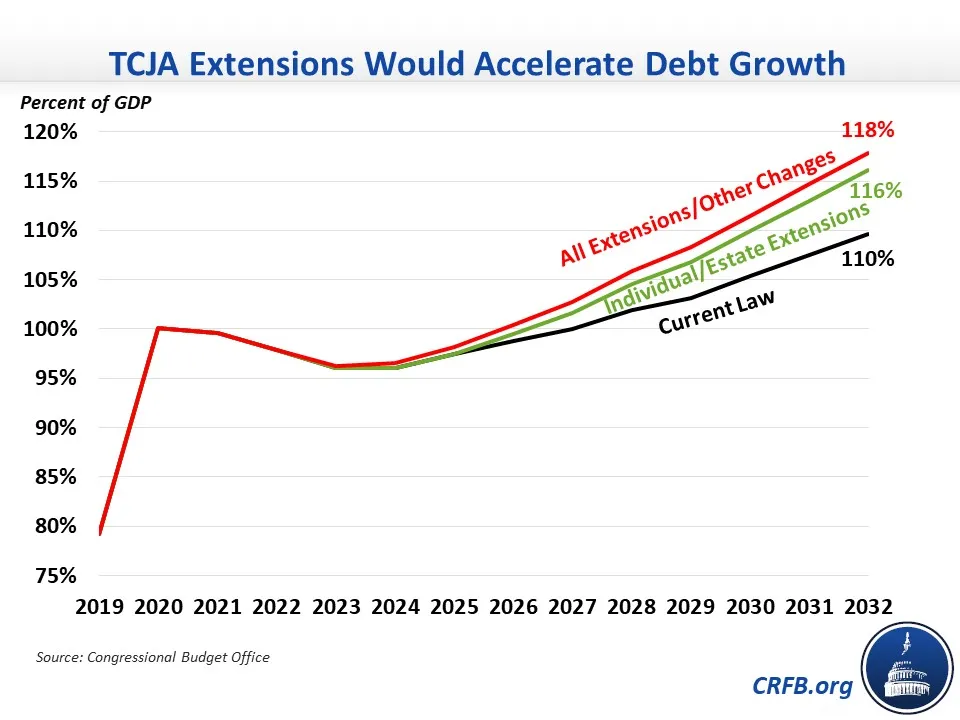

The Congressional Budget Office's (CBO) latest baseline spells out what the federal budget will look like under current law, but also estimates the cost of several policy alternatives. The most notable one is the cost of extending most temporary provisions in the Tax Cuts and Jobs Act (TCJA) of 2017, which CBO hadn't officially estimated since 2019. CBO estimates that extending the individual income and estate tax provisions that are set to expire after 2025 would cost $2.2 trillion through 2032; also extending business tax provisions that are set to expire or become less generous would increase the cost to $2.7 trillion. These costs would increase debt as a share of Gross Domestic Product (GDP) in Fiscal Year (FY) 2032 to 116 to 118 percent of GDP, compared to 110 percent of GDP under current law.

The TCJA made significant changes to the federal tax code, including lowering corporate and individual income tax rates, increasing the standard deduction, reforming child tax benefits, and reforming the corporate international tax system, amongst other provisions. In an effort to mask its true cost and fit within cost limits, almost all of the individual and estate tax provisions are set to expire after 2025, while several business tax provisions are set to either expire, go into effect, or become less generous at various points.

Extending the individual and estate tax provisions permanently would cost $2.2 trillion through FY 2032 and $362 billion in 2032 alone. The largest extension costs include the reductions in individual income tax rates ($1.5 trillion), the increase in the standard deduction ($887 billion), the scaling back of the Alternative Minimum Tax (AMT) ($884 billion), the expansion of the Child Tax Credit (CTC) ($514 billion), and the 20 percent deduction for pass-through business income ($459 billion). These costs are partially offset by extending revenue-raising provisions like the repeal of personal exemptions ($1.4 trillion saved), the $10,000 cap on the State and Local Tax (SALT) deduction and other deduction changes ($765 billion), and the cap on pass-through business loss deductions ($154 billion).

Deficit Impact of Extending Tax Cuts and Jobs Act Provisions

| Policy (First Year Policy Expires/Changes) | Cost/Savings (-) Through FY 2032 |

|---|---|

| Reduced individual income tax rates (2026) | $1.5 trillion |

| Higher AMT exemption thresholds (2026) | $884 billion |

| Itemized deduction changes, including $10,000 SALT deduction cap (2026) | -$765 billion |

| Doubled standard deduction (2026) | $887 billion |

| Elimination of personal exemptions (2026) | -$1.4 trillion |

| Increased child tax credit from $1,000 to $2,000 (2026) | $514 billion |

| 20 percent pass-through deduction (2026) | $459 billion |

| Pass-through business loss deduction limit (2027) | -$154 billion |

| Opportunity zone capital gains deferrals (2027) | $103 billion |

| Doubled estate tax exemption threshold (2026) | $102 billion |

| Other changes (2026) | -$28 billion |

| Subtotal, Individual and Estate Tax Extensions | $2.2 trillion |

| 100 percent bonus depreciation (2023) | $250 billion |

| Reinstated R&E expensing (2022) | $153 billion |

| Business provisions kept at 2025 parameters (2026) | $125 billion |

| Subtotal, Business Extensions/Other Changes | $529 billion |

| Total | $2.7 trillion |

Source: Congressional Budget Office. Numbers may not sum due to rounding.

In addition to this extension, the TCJA includes business tax provisions that are either temporary, revenue-raisers that go into effect with a delay, or set to become less generous at various points. The one expiring provision in this category is bonus depreciation, which allows businesses to deduct the cost of equipment immediately instead of over time. Bonus depreciation is set to phase down starting next year and phase out completely by 2027; extending the full policy would cost $250 billion through FY 2032. A revenue-raiser that takes effect with a delay is the TCJA's elimination of R&E expensing, instead requiring R&E costs to be written off over five years. This policy already went into effect this year and would cost $153 billion to repeal permanently. The TCJA also contains a few policies that will become stricter after 2025, specifically tighter restrictions on meals deductions, a reduction in the foreign-derived intangible income (FDII) deduction from 37.5 to 21.875 percent, and an increase in the base erosion and anti-abuse tax (BEAT) rate from 10 to 12.5 percent. Avoiding these changes would cost $125 billion, with the majority coming from the FDII deduction.

Extending these provisions or avoiding these changes would cost $529 billion through FY 2032, for a total cost of $2.7 trillion.

Either of these scenarios would have significant implications for the debt despite the fact that the changes largely would not take effect until 2026. Extending the individual and estate tax provisions would cause the debt to reach 116 percent of GDP by FY 2032, up from 110 percent under current law, while also extending or avoiding the business tax provisions would increase debt to 118 percent of GDP.

TCJA extensions will be a major decision point in 2025 (or this year for a few policies). Either extension scenario would add hundreds of billions of dollars to deficits each year after 2025 if not offset. Lawmakers must work toward a solution that either allows the tax cuts to expire, offsets the cost of extensions, or some combination.