A Brief History of (Financial) Time

This week marks the one year anniversary of the Lehman Brothers collapse, an event that both seriously destabilized and ominously ruptured the U.S. and global financial system. Beginning in 2007, losses in mortgage markets weakened the balance sheets of large banking institutions. In an effort to maintain their capital ratios (the percent of a bank’s capital to its risk-weighted assets), these banks reduced their lending and liquidity support for the economy.

Given the financial system’s interconnectedness, problems at individual institutions severely reduced confidence in the system as a whole.

Officials within the Bush administration and the Fed allowed Lehman Brothers to fail but mustered the political will one day later to rescue AIG.

In the weeks and months following the Lehman collapse, the Bush administration, the Obama administration, the Fed, and Congress have established several unprecedented programs to restore confidence in the financial system. Here is a list of the most notable programs and actions:

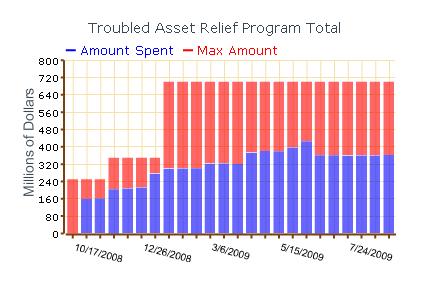

• The Bush Administration and Congress created the Troubled Asset Relief Program (TARP), which has injected over $360 billion into hundreds of banks, systemically important institutions, and several auto companies

• FDIC established the Temporary Liquidity Guarantee Program (TLGP) to provide guarantees to new medium-term bank debt

• FDIC deposit insurance increased from $100,000 to $250,000 per account

• Fed reduced interest rates to a target range between 0-0.25%

• Fed has expanded liquidity support for the banking system, money market mutual funds, commercial paper issuers, and securitization markets.

Overall, the general consensus has been that the extraordinary actions taken by the Fed and government have averted financial catastrophe. Yet, this has come at the cost of enormous government commitment to the financial system.

Exiting from Commitments

Several emergency programs at set to expire with the next several weeks as demand for emergency loans has rescinded: the Money Market Mutual Fund Guarantee Program and the FDIC’s TLGP. In addition, the Fed has provided less and less funding through the Commercial Paper Funding Facility (CPFF), Term Auction Facility (TAF), and the Asset-Back Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF). Most of the Fed’s liquidity programs are scheduled to expire in 2009 or early 2010. Yet, the Treasury still promises to “continue to provide support where it is necessary to sustain confidence in the financial system and to support critical channels of credit to households and businesses.”

Financial Sector Reform

In June the Administration released its plan to overhaul the financial system. Overall, the proposals would increase government scrutiny over most aspects of finance: more power for the Fed; creation of a new consumer protection agency; stronger oversight of financial products; and a new government authority to break up big firms under stress.

The health care debate and pushback from banks and conservative lawmakers have sidetracked calls for financial reform. However, the president has now redoubled his efforts to pass new legislation. Many financial sector observers have noted bank problems may even be worse now than pre-crisis as too-big-to-fail banks have grown even larger.

We believe that the Administrations proposals for greater financial oversight are steps in the right direction to ensure that another crisis like this does not repeat itself. The economic crisis has drained the country’s resources, restricting our ability in the short-term for financing another round of financial bailouts.

For in-depth information on the costs and history of Fed liquidity programs, TARP funds, and other government guarantees of the financial sector, visit Stimulus.org.