Op-Ed: Drawing a AAA-Road Map for Post-Downgrade America

The Atlantic | August 11, 2011

The country's most critical structural problem isn't employment or entitlements. It's Washington. And its window to govern by leadership rather than crisis is getting narrower every day.

The S&P downgrade late Friday afternoon in Washington kicked off the most anxious and frenetic week in world markets since the Great Recession ended. The rating agency's observation that U.S. politics was broken might have seemed like old news to voters, but to outsiders it was a stunning confirmation that the recovery is all but over and Washington has no clue how to get it back on track. But the panic over the downgrade and subsequent sell-off has glossed over what exactly our AA+ means for the economy, our prospects, and the road back to a sterling rating. With a little help from a report published yesterday by the Committee for a Responsible Federal Budget, here is your guide to the downgrade.

Don't Panic ...

The first thing to understand about this downgrade is that it is not, in itself, a reason to panic. U.S. long-term Treasury bonds have been downgraded from AAA to AA+, which according to S&P means that instead of an "extremely strong capacity to meet" our financial commitments, we now have a "very strong capacity" to do so - not much of a difference.

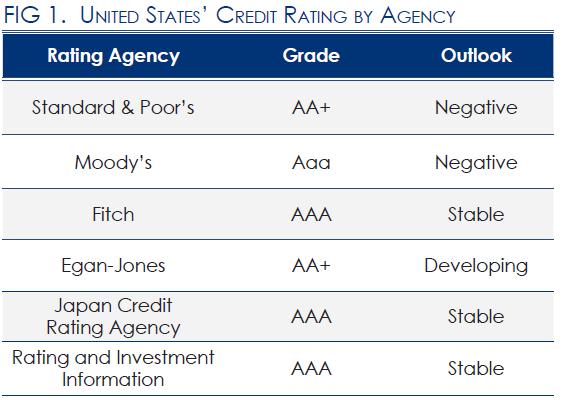

In addition, at least for now, the other two major rating agencies - as well two of the other three minor certified agencies that rate US debt - still rate U.S. Treasuries as AAA, also denoted "Aaa."

Those concerned that everyone will start dumping our debt en masse as a result of this downgrade shouldn't be. In the case of domestic money market funds, recent regulations basically deem U.S. Treasuries as safe assets no matter what happens to them; and frankly there aren't many other assets to flock to right now. As former CBO Director Rudy Penner would say, "we're still the finest looking horse in the glue factory." This second point also rings true with respect to our international investors. We are the world's reserve currency and have more bonds in the global market than all AAA-rated countries combined.

Rather than going up, interest rates have actually fallen a bit since the rating downgrade. This is not inconsistent with what has happened to other AAA-downgraded countries, where interest rate effects have generally been quite small.

... Okay, Panic a Little

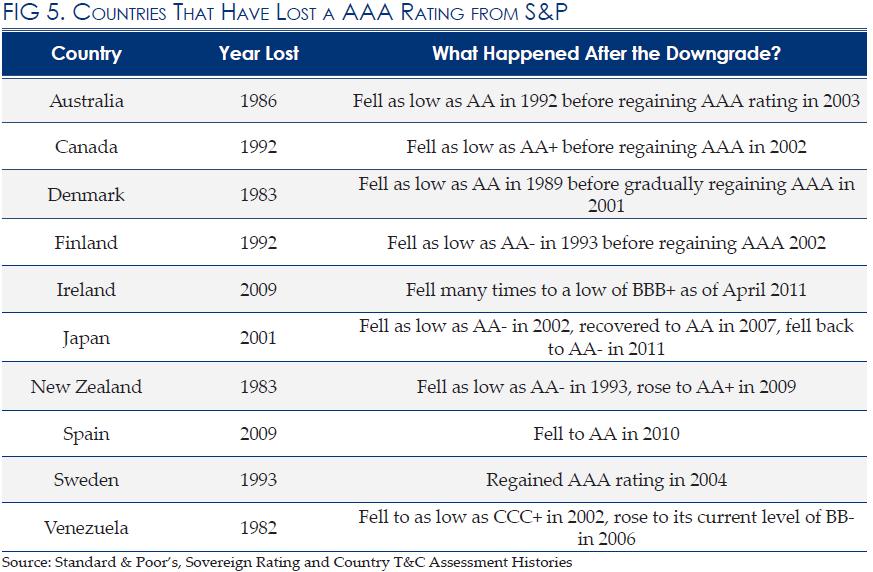

If rating downgrades don't augur immediate crises, they tend to indicate trouble on the horizon. Of the 10 other countries that have been downgraded from AAA, eight experienced further downgrades and five have still never recovered their AAA rating. Deeper downgrades have been associated with interest rate spikes, and the fact that both S&P and Moody's have us on a negative outlook suggests that more downgrades could be in our future.

What are the consequences of further downgrades? The most direct one could be higher interest rates, as investors insist on a risk premium. Even a 0.1 percent increase in interest rates would mean an additional $130 billion in government spending on interest over the next 10 years that we would have to offset in hiring taxes or fewer investments to meet the same debt goal. A 0.7% increase in interest rates would be enough to erase all of the gains from the recent debt deal.

In addition, higher interest rates could reverberate throughout the market, impacting everything from mortgages to small business loans - and ultimately leading to something economists call "crowd out," where fewer dollars go into growth-driving investments.

The biggest concern, though, should be that these rating downgrades could advance the day of a fiscal crisis. At some point, if we don't make some changes, investors will lose confidence in our nation's ability to make good on its debt. When that occurs, it is possible we could experience a global economic crisis akin to the financial crisis of 2009, except with no one available to bail out the U.S. government.

It's Not About the Money

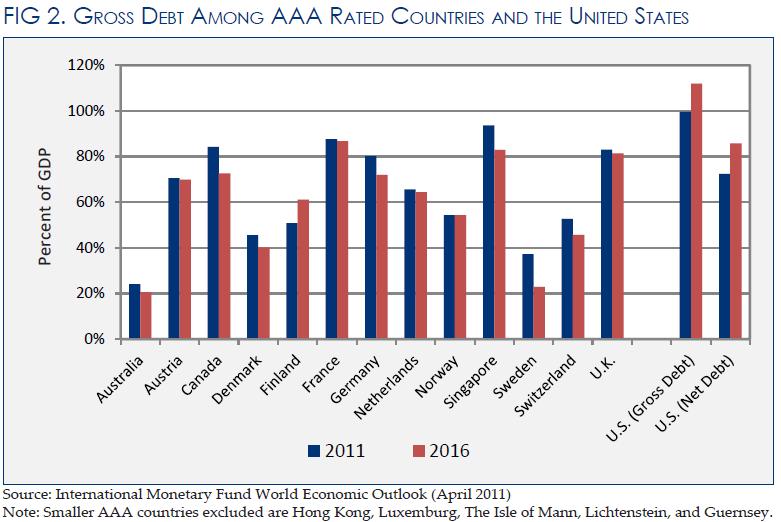

The United States has a higher burden of gross debt than any other AAA-rated country in the world. We're also the only country besides Finland to expect our debt share to grow through 2016. Our entitlement programs are growing uncontrollably as a result of an aging population and rapid health care cost growth - structural problems that make it difficult to deal with our debt. But despite all this, the downgrade was not fundamentally about money. It was about politics.

The country's most critical structural problem isn't employment or entitlements. It's Washington. There is, outside the wide halls and narrow minds of Congress, an emerging consensus on how to fix our problems: Cut future spending and raise future revenue. Enact stimulus today and reform taxes tomorrow. Encourage people to work longer and take more responsibility for their own retirement. Do everything we know how to do to slow health care costs now, and keep looking for solutions.

But the political system hasn't yet been able to reach these solutions and address the inherent tradeoffs between them. As S&P wrote:

"The difficulties in bridging the gulf between the political parties over fiscal policy... makes us pessimistic about the capacity of Congress and the Administration to be able to leverage their agreement this week into a broader fiscal consolidation plan that stabilizes the government's debt dynamics any time soon."

If Washington can't fix itself, the opinion of S&P should be the least of our worries.

As Leon Panetta used to say, "we govern by leadership or crisis." We need to do the former. Our time is running out.