Governing through Leadership: Steps to Secure Our Fiscal Future

A Memorandum to President-Elect Donald J. Trump

| TO: | President-Elect Donald J. Trump |

| FROM: | Governor Mitch Daniels, Secretary Leon Panetta, Congressman Tim Penny; Chairmen, Committee for a Responsible Federal Budget |

| CC: | Vice President-Elect Mike Pence, Speaker Paul Ryan, Senator Mitch McConnell, Senator Chuck Schumer, Representative Nancy Pelosi |

Congratulations on your election to the highest office in the land. When you take office, you will face many challenges both at home and abroad. At the same time, your position as chief executive of our great nation will present you with unparalleled opportunities to shape our collective future.

It has often been said that politicians campaign in poetry but govern in prose. While you campaigned on not being a traditional politician, you will soon confront the age-old challenge of translating your ambitious campaign promises into a governing agenda. As you develop your agenda, we hope you will follow through on your promise to address many of our country’s greatest challenges, including our rising national debt.

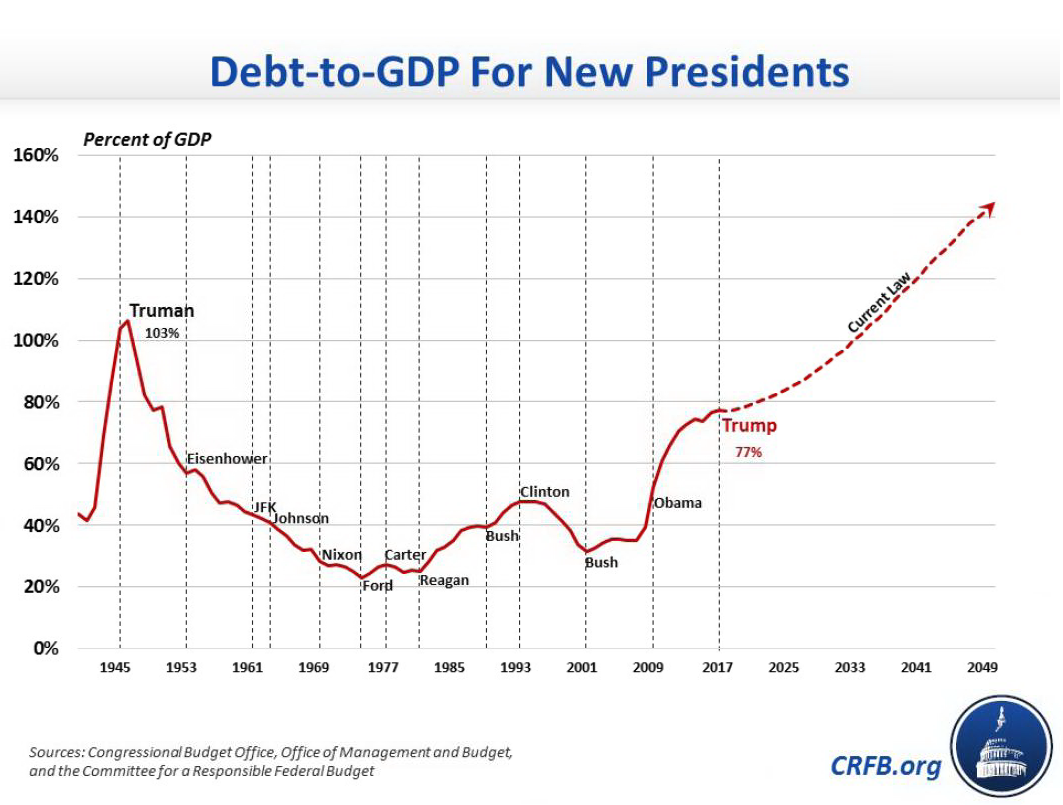

With the exception of President Harry Truman during World War II, no new president has entered office with a debt burden as high as the one you will face upon being sworn in.1 And unlike under Truman’s presidency, when debt was expected to come down quickly, during your administration debt levels are projected to grow continuously and rapidly. Meanwhile, Social Security and Medicare will continue moving toward insolvency, threatening the retirement security of tens of millions of Americans.

During the campaign, you repeatedly raised concern over the nation’s $20 trillion gross debt and presented yourself as a fixer who would embrace negotiation and break the partisan gridlock in Washington. You also pledged to save Social Security and Medicare. Following through on these promises will not be easy, but success is vital.

We believe ensuring a sustainable fiscal outlook is among the most important things you can do to support economic growth and shared prosperity for current and future generations. We recommend beginning with the following concrete steps early in your term:

- Use the power of the presidency to elevate the importance of fiscal responsibility.

- Set a fiscal goal or goals, and meet them in your first budget.

- Pursue principled, bipartisan compromise, including by beginning negotiations with Congress on a multi-year budget agreement.

- Promote strong economic growth, without relying solely on growth to fix the debt.

- Work with Congress to advance pro-growth, fiscally responsible tax reform.

- Pay for your proposed initiatives and veto legislation that adds to the debt.

- Task federal agencies to identify waste and inefficiencies.

- Implement health care reform focused on cost containment.

- Take initial steps to save Social Security.

- Appoint a strong and experienced economic team.

Our Nation’s Fiscal Challenge

During the presidential campaign, you promised to deliver faster job and wage growth, a more competitive tax code, a robust national defense, affordable child care, a better health care system, improved national infrastructure, a more effective government, and a stronger middle class. None of these goals can ultimately be achieved and sustained if you neglect our high and rising debt.

Slowing the unsustainable growth of our national debt is a key ingredient to growing the economy and ensuring adequate government resources to afford other important priorities. Unfortunately, you will enter office with a deteriorating fiscal outlook.

Consider the following:2

- On the day you take office, debt held by the public will be at a post-World War II era record high of 77 percent of Gross Domestic Product (GDP), and it is projected to almost double by 2050.

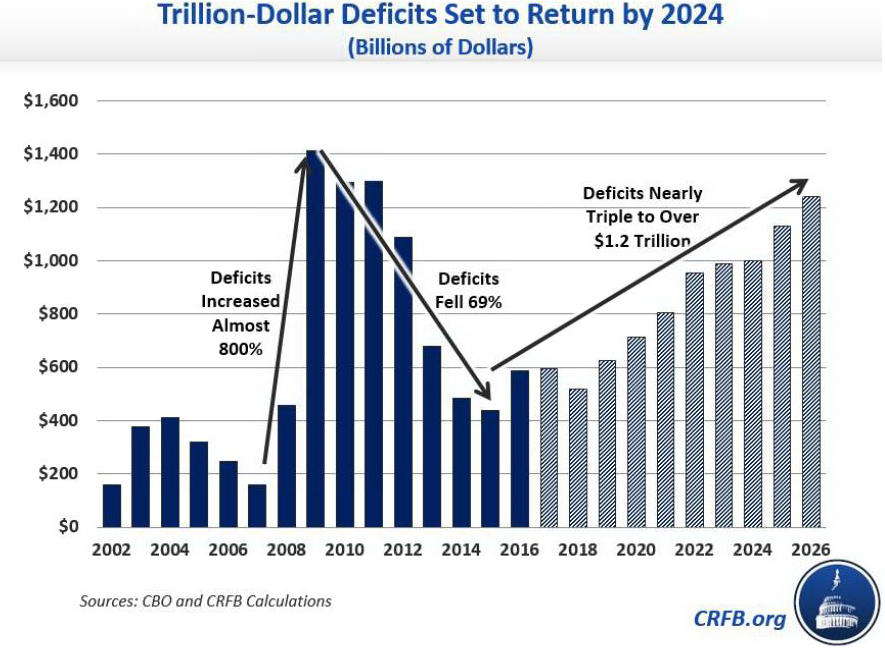

- The deficit, which stands at nearly $600 billion, will grow to $800 billion in the final fiscal year of your first term and exceed $1 trillion by the end of a hypothetical second term.

- Over your 4-year term, 85 percent of federal revenue will have been pre-committed to auto-pilot spending, such as Social Security, Medicare, and interest on the debt.

- The Highway, Social Security Disability Insurance, and Medicare Hospital Insurance trust funds will all run out of reserves in the next decade, and the Social Security Old-Age trust fund will be depleted just a few years later. Without action, devastating across-the-board cuts are scheduled for all four programs.

High and rising debt levels threaten to stunt economic growth, curb rising incomes, raise interest rates, increase federal borrowing costs, and limit our ability to respond to unforeseen emergencies. Growing mandatory spending and interest payments in particular threaten to crowd out other important priorities – including public investments and national security – and compromise the solvency of our nation’s most important health and retirement programs.

| While some have suggested ignoring our debt problems in light of today’s low interest rates, we believe such an approach would be shortsighted and ill-advised. The United States currently faces a low cost of borrowing but a high cost of waiting, and should leverage these realities by gradually phasing in measures that simultaneously slow the growth of the debt and accelerate the growth of the economy. Recent growth has relied heavily on monetary policy, but sustained long-term growth will require a comprehensive economic strategy, including smarter fiscal policy as a central component of a pro-growth agenda. |

|

Ten Steps to Secure Our Fiscal Future

Accomplishing all the policy changes necessary to fix our fiscal situation will take time, and will not necessarily occur in any single “grand bargain” piece of legislation in your first few months in office. But ten immediate steps can be taken early in your administration to set the table for real progress on addressing the debt and growing the economy:

- Use the power of the presidency to elevate the importance of fiscal responsibility. During the campaign,you frequently mentioned the threat posed by our high and rising national debt. At the same time, you put forth positions that, if unchanged, could significantly worsen our fiscal situation. Going forward, your administration should embrace the facts about our nation’s fiscal situation and the tough choices necessary to address it. You should also use the power of your office to put the debt issue on the national agenda through speeches, town halls, press conferences, radio addresses, and other tools at your disposal. On the campaign trail you showed an impressive ability to connect with the American public. Therefore while the solutions to our nation’s fiscal challenges may not be easy, you should directly engage the American public about the seriousness of the problem and the many benefits of enacting the necessary solutions.

- Set a fiscal goal or goals, and meet them in your first budget. It is hard to lead people toward a destination without first showing where you will take them. Early in your administration, you should set fiscal goals for the short, medium, and long terms. There is no one right goal; you may propose balancing the budget or primary budget by a certain year, reducing the national debt to a certain share of GDP, setting specific spending and revenue targets, or eliminating the nation’s long-term fiscal gap. Whatever goal you choose should be sufficient to ensure debt is not growing faster than the economy. And importantly, your first budget should include specific policy proposals sufficient to meet this goal or goals, and you should ask Congress to do the same in their budget.

- Pursue principled, bipartisan compromise, including by beginning negotiations with Congress on a multi-year budget agreement. As president, you will have little ability to grow the economy or fix the debt on your own; it will require working with a deeply divided Congress. But your skills as a negotiator can serve you well in this respect if you are willing to work across the aisle with Democrats and Republicans in the House and Senate. In fact, some of the largest improvements in our fiscal situation have resulted from major bipartisan budget agreements between the House, Senate, and the White House. During your first year in office, you should reach out to leaders of both parties in both chambers to begin bipartisan negotiations on a multi-year budget agreement. Such an agreement could simultaneously address many areas of the budget and tax code and replace some of the pending “sequester” cuts to defense and nondefense spending with more thoughtful reforms that improve the overall fiscal situation over the next few years and the long term. It could also include a long-term increase in the debt limit, as many previous budget agreements that improved the fiscal outlook have done in the past.

- Promote strong economic growth, without relying solely on growth to fix the debt. Faster and broadlyshared economic growth should be a primary objective of your administration. Only greater economic growth can meaningfully lift wages, expand wealth, create jobs, and enhance economic security. Faster growth can also improve the country’s fiscal position, chiefly by increasing revenue collection. Unfortunately, the economy has not grown as fast as needed in recent years, and it has been heavily reliant on monetary policy. Your administration should therefore focus on pursuing structural pro-growth reforms to the tax code, government spending, energy policy, trade policy, and regulatory policy. At the same time, importantly, you should set forth realistic expectations and rely on credible economic assumptions and estimates. No amount of pro-growth reforms will do enough to fix all of our country’s problems, particularly in the context of an aging population. In order to simply prevent debt levels from rising as a share of the economy – even assuming no cost to any pro-growth reforms – projected productivity growth would need to roughly double to levels never achieved on a sustained basis in modern history.

- Work with Congress to advance pro-growth, fiscally responsible tax reform. The United States tax code is currently anti-growth, uncompetitive, overly complex, and raises too little revenue to finance current spending. In part, these concerns are driven by the $1.3 trillion of tax expenditures that distort behavior and leave both tax rates and deficits higher than they otherwise would be. The last time policymakers reformed the tax code by reducing these tax expenditures in favor of lower tax rates was 30 years ago. Further reform, both to the individual and corporate tax codes, is certainly due. As you know, developing a plan for comprehensive reform will take significant time and resources; the 1986 tax reform was the result of an effort in the Treasury Department that began in 1984. Early in your administration, you should instruct your Treasury Department to begin working with the Ways & Means and Finance Committees to develop detailed tax reform legislation. Reform should ultimately increase revenue collection and generate funds in a more efficient way than current law.

- Pay for your proposed initiatives and veto legislation that adds to the debt. When you are in a hole, the first step toward getting out is to stop digging. This is why past efforts to get the debt under control have begun with support of pay-as-you-go rules that codify the principle of not making the existing situation worse. In this spirit, all of your proposals – whether for infrastructure investment, child care, tax reform, or health reform – should be fully offset with spending cuts and/or revenue increases elsewhere in the budget. You should also hold Congress to the same standard of fiscal responsibility by pledging to veto any nonemergency legislation that adds to the debt under current law. It is important that you reject the old politics of agreeing to fiscal responsibility on paper but evading it in practice.

- Task federal agencies to identify waste and inefficiencies. To create a culture of fiscal responsibility, the government must show that each dollar of government spending is a dollar well spent. During the campaign you highlighted the need to reduce waste and excesses throughout government, and as president you must follow through with this objective. Although discretionary spending represents less than one-third of the budget and 10 percent of projected spending growth over the next decade, it is important for all agencies to lead by example. In your first hundred days, you should instruct each federal agency to send you a list of programs, policies, or rules that they view as wasteful, low-priority, duplicative, obsolete, inefficient, or damaging to economic growth. And then you should work to eliminate, consolidate, or reform these areas of government.

- Implement health care reform focused on cost containment. The federal government spends more on health care than any other part of the budget, and these costs are growing rapidly due to rising per-capita health costs and an aging population. Over the next 30 years, combined federal health spending is projected to grow by 3.3 percent of GDP – from 5.5 to 8.8 percent – explaining more than half the increase in projected deficits. Legislation addressing health care is likely to come up early in your administration, as House and Senate Republicans work to repeal and replace the Affordable Care Act (“Obamacare”). You should insist that any such legislation not only reduces deficits on net, but includes cost control measures to slow the growth of Medicare and Medicaid, as well as private sector health spending. There have been many such policies offered by experts on both sides of the aisle that are worthy of consideration.

- Take initial steps to save Social Security. Social Security is less than 18 years from insolvency, at which point all recipients, regardless of age or income, will face an immediate 21 percent benefit cut under current law. Avoiding this cut at the last minute would require substantial borrowing or massive tax increases on working citizens. In order to phase in targeted reforms and protect those who rely on the program, changes must begin in the next few years. Thoughtful reform will require both parties to work together. The last time we fixed Social Security, back in 1983, it was because Republican President Ronald Reagan and Democratic Speaker Tip O’Neill appointed a bipartisan commission and drew heavily from its recommendations. You should appoint a similar commission today to break the political stalemate and ensure Social Security can pay adequate benefits to current and future generations.

- Appoint a strong and experienced economic team. Assembling the right economic team is critical to moving your priorities forward. As a business leader, you understand the importance of surrounding yourself with strong experts, advisors, managers, and honest brokers. Most relevant for economic and fiscal policy are the Secretary of the Treasury, Director of the Office of Management and Budget, Director of the National Economic Council, and Chair of the Council of Economic Advisers. These positions should be filled by candidates with expertise and experience who bring a diverse set of perspectives to the table. Economic policymaking inherently requires weighing tradeoffs and risks, and a strong economic team can help you do this.

Conclusion

Putting our nation on a sound fiscal path will require a comprehensive approach to economic policy that promotes economic growth while addressing the core drivers of our long-term fiscal challenge. Several milestones await you early in your administration. But those milestones – including the submission of your first budget, the next debt limit breach, and the return of sequestration in fiscal year 2018 – also present opportunities to show leadership.

As you take office, you face not only daunting fiscal and economic challenges, but a deeply divided country that is losing faith in its leaders’ willingness to do the right thing. Americans are looking for action – not only on the real problems we face, but in ways that restore their confidence in Washington. Strong leadership is required to restore the country’s fiscal footing, and only by doing so will you be able to achieve sustained economic growth and secure your own presidential legacy. Perhaps the single best way to set your presidency apart would be to break the trend of ever-higher debt before it breaks the American economy and the American Dream.

1. This is measured as debt held by the public as a share of the economy in the first fiscal year of a president’s term. According to our estimates, debt held by the public will total about 77 percent of GDP when Trump takes office; the only higher amount was 103 percent when Truman took office at the end of World War II.

2. All facts, figures and statistics are based on projections from the nonpartisan Congressional Budget Office and calculations by the nonpartisan Committee for a Responsible Federal Budget.