The Cost of Rising Interest Rates

This paper has been updated and is avaible here

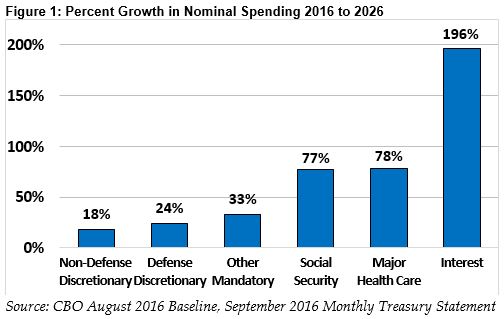

Over the next decade, interest payments on the debt are projected to be the fastest growing part of the federal budget.

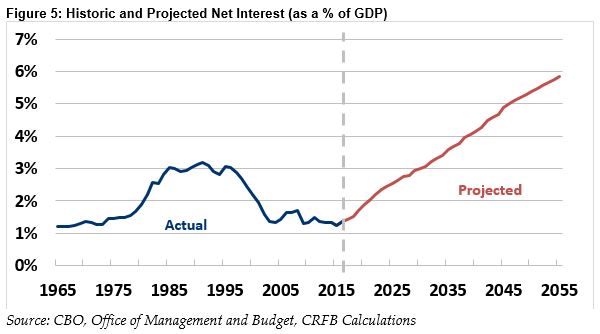

Last year, the federal government spent $241 billion – roughly 1.3 percent of Gross Domestic Product (GDP) – on interest payments. That’s among the lowest at any point since the 1970s, driven by historically low interest rates.

Yet recent market activity and expected Federal Reserve actions already suggest interest rates will rise; in fact, both the 3-month Treasury bill and 10-year Treasury note have increased by over 75 percent in the past 5 months.

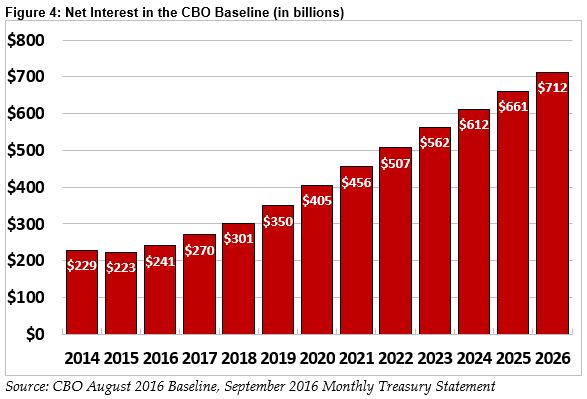

In combination with rising debt levels, this increase in rates will lead interest payments to grow rapidly. Under current law, the Congressional Budget Office (CBO) projects interest payments to nearly triple in nominal dollars and double as a percent of GDP – from $241 billion and 1.3 percent of GDP in Fiscal Year (FY) 2016 to $712 billion and 2.6 percent of GDP by FY 2026.

As these costs rise, interest spending threatens to crowd out other important priorities. Meanwhile, our high level of debt puts the country’s finances at substantial risk if interest rates rise even further than expected. Policies that reduce revenue or increase spending would worsen this situation further.

To mitigate the costs and risks of rising interest rates, policymakers should enact a plan or plans designed to gradually reduce the debt as a share of GDP.

The Current Costs of Interest on the Debt

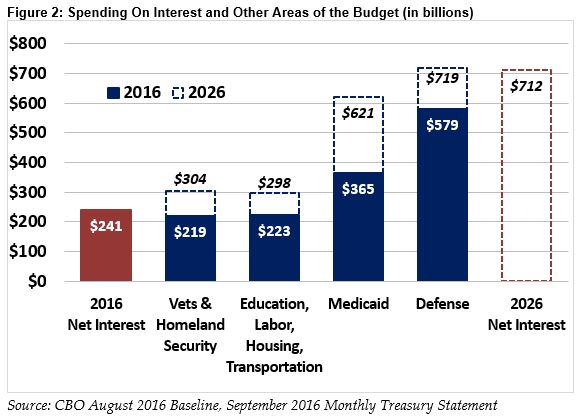

Last year, the federal government spent $241 billion on net to service roughly $14 trillion of debt – meaning it paid an average interest rate of less than 2 percent. Even at today’s exceptionally low interest rates, this is already more than we spend on the Departments of Homeland Security and Veterans Affairs combined. It is also more than our combined spending on the Departments of Education, Labor, Housing and Urban Development, and Transportation.

Every dollar the United States devotes to interest payments is a dollar that cannot fund national priorities or that must be financed through higher taxes or debt. And over time, interest costs will consume a rising share of the budget.

Projections of Interest on the Debt

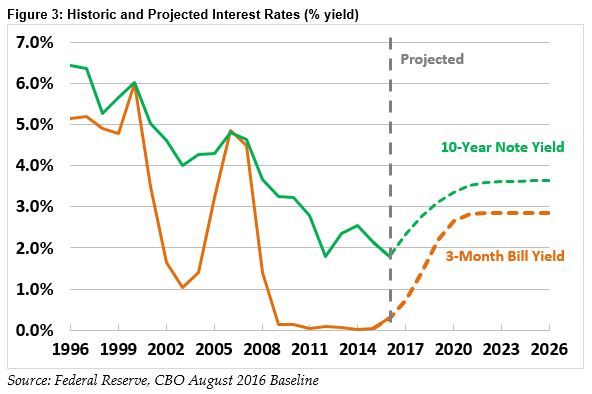

Over the past 20 years, interest rates have averaged 4.2 percent on 10-year notes and 2.4 percent on 3-month bills. By comparison, in FY 2016 they averaged 1.9 percent and 0.25 percent, respectively.

CBO does not expect interest rates to return to their historic levels any time soon – but it does project they will rise substantially from today’s near-record lows. By the early 2020s, CBO projects 10-year notes to pay 3.6 percent in interest and 3-month bills to pay 2.8 percent.

As interest rates rise and debt held by the public grows from $14 trillion today to $23 trillion by 2026, CBO expects spending on debt service to increase significantly. As a result of these factors, interest payments will rise.

Under current law – assuming no changes in policy – CBO projects:

- In nominal dollars, net interest costs will nearly double by FY 2021 and triple by FY 2026, growing from $241 billion to $456 billion to $712 billion.

- As a share of the economy, federal interest payments are expected to double in 10 years, from 1.3 to 2.6 percent of GDP.

- The annual budget deficit will rise from $587 billion in FY 2016 to $1.2 trillion in FY 2026. Nearly three-quarters of this can be explained by the $471 billion rise in interest payments.

- By FY 2024, interest payments will surpass how much the government spends on all of its investments, including research and development, education, training, and infrastructure.1 By FY 2027, it will exceed defense costs.

- Over the long term, interest costs will grow from 1.3 percent of GDP today to 3.7 percent in two decades and 5.9 percent in four decades.

What if Interest Rates Differ from Projections?

CBO expects interest rates to rise, but not to their pre-recession levels. As a result of slower labor force and productivity growth, growing income inequality, and other factors, CBO projects rates (on an inflation-adjusted basis) will be over one and a half percentage points lower than the average between 1990 and 2007. If interest rates differ from CBO’s projections in either direction, the budgetary implications could be significant.

We estimate based on CBO data that if (in isolation) interest rates were 1 percentage point higher than projected through 2026 – a level that would still be less than the pre-recession average—debt would be $1.5 trillion higher, or 6 percent of GDP, higher. A sustained 1 percentage point decrease in interest rate projections would have a roughly similar magnitude in the opposite direction.

Last year, we estimated the impact of a number of other changes in interest rates on the size of the federal debt. While we have not re-estimated these costs, we expect them to be similar in magnitude, though a bit smaller.

Fiscal Irresponsibility Would Make Interest Costs Much Worse

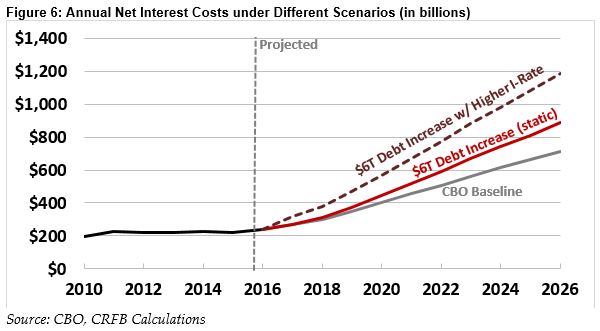

While interest costs are already the fastest growing part of the budget under current law, they would grow much faster if policymakers further add to the debt. Whereas interest spending would almost triple under current law, we estimate it could quadruple or even quintuple under President-elect Donald Trump’s $6 trillion campaign plans.2

Policies that add to the federal debt increase interest costs for two reasons. First, these policies increase the government’s debt holdings, which it must then pay further interest on. Second, higher levels of federal debt tend to push up interest rates themselves –even more so when additional borrowing is used to finance productivity-increasing policies such as infrastructure projects or certain changes to the business tax code.

By our estimates, Trump’s tax and spending plans would increase the primary deficit by $5.2 trillion. That would lead directly to an $800 billion increase in interest costs over a decade, including over $150 billion in FY 2026 alone. If that higher debt led interest rates to rise 1 percent above projections – a very rough but likely conservative estimate – interest costs would increase by $2.5 trillion over a decade, including over $450 billion in 2026 alone.

Conclusion

Even with today’s low interest rates, deficits are already on the rise. As debt continues to grow and interest rates return toward more normal levels, interest spending is slated to be the fastest growing part of the budget and will ultimately crowd out other important priorities. Adding to the debt, even for worthwhile policy changes, would only accelerate the growth in interest costs.

There is an argument for some borrowing at today’s low interest rates so long as this borrowing is accompanied by a plan to pay down the new debt over the next few years before interest rates rise. Ultimately, however, the best way to minimize the cost of rising interest rates and prevent against interest-rate risk is to enact a thoughtful mixture of tax and spending reforms that put the debt as a share of the economy on a clear downward path over the long run. Low interest rates have made the debt very manageable over the recent past, but as we’ve seen in recent weeks, interest rates have the ability to rise again quickly. It’s important to be prepared.

1 Congressional Budget Office, August 2016 baseline and “Federal Investment,” December 2013.

2 In October 2016, we estimated Trump’s plan would cost about $5.3 trillion over a decade. Since that estimate, Trump has proposed a $550 billion infrastructure plan. With interest, this would raise the total cost of his plans to about $6 trillion over a decade.