Short-Term Deficits May Be Shrinking, But Long-Term Problem Remains

Update: This blog has been updated to include the Mid-Session Review and CBO projections for the 2013 deficit.

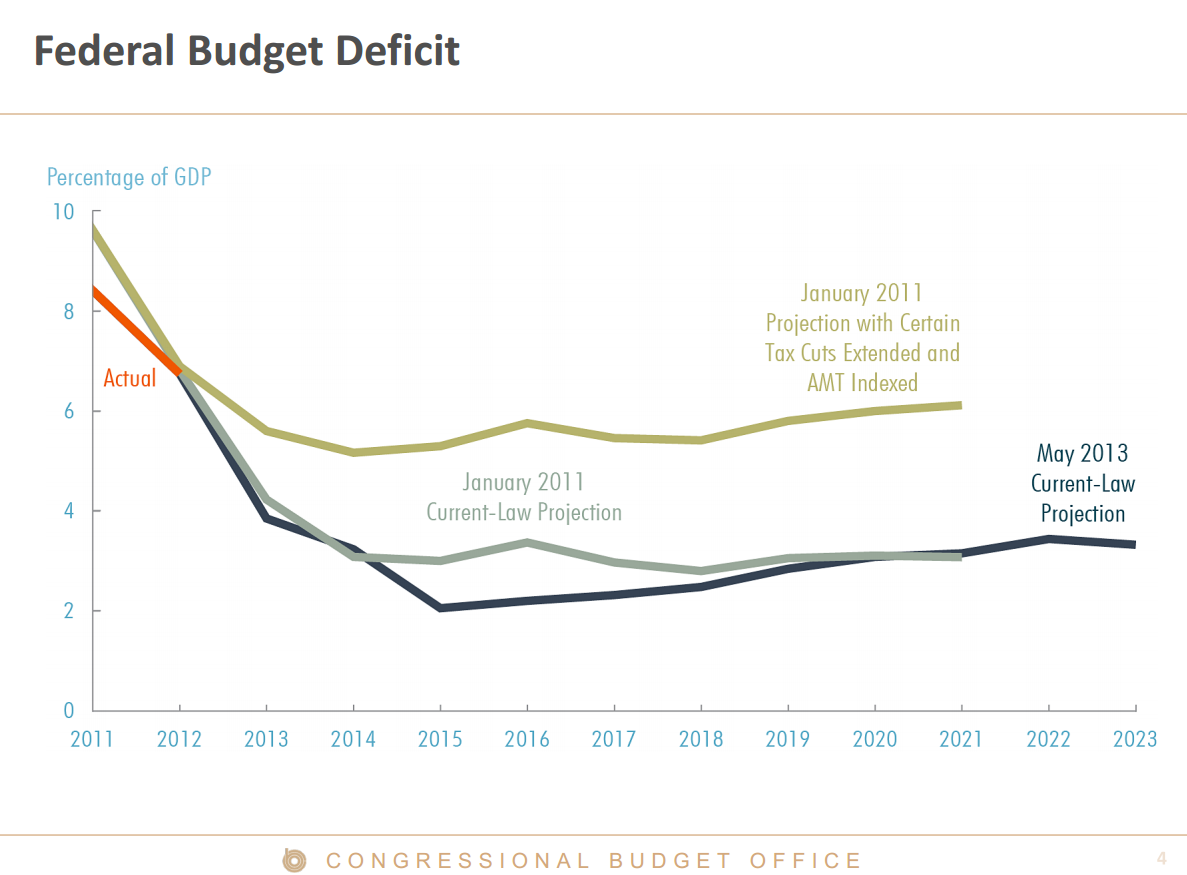

Yesterday, the Treasury Department and the Office of Management and Budget released final budget results for Fiscal Year 2013, which ended on September 30. The deficit fell to $680 billion - a drop of more than $400 billion from the $1.1 trillion deficit posted in 2012. Last year's deficit also came in substantially under the President's budget projections from April, which had projected the year-end deficit would be $919 billion, and the Mid-Session Review projection of $735 billion. It was also $40 billion above CBO's projection in May. Although this year's deficit has shrunk, deficits are projected to start growing again as a percentage of the economy after 2018 and the long-term debt problem driven by health care costs and an aging population has barely budged.

Treasury Secretary Jack Lew said in a statement that the deficit has fallen faster over the last four years than any period since World War II, but it's not coincidental that the fall comes off of the highest deficit since WWII, driven by the 2008 recession and stimulus spending. The deficit fell from 10.1 percent of GDP in 2009 to 4.1 percent of GDP in 2013, a drop of 6 percentage points. There was actually a larger drop in the deficit in the 1990s over a longer time period, from a 4.7 percent deficit in 1992 to a 2.4 percent surplus in 2000.

More to the point, this drop in deficits was largely a predictable result of a recovering economy. The year-end deficit of 4.1 percent was nearly the exact 4.2 percent deficit that the Congressional Budget Office predicted in May, or the 4.3 percent deficit predicted in January 2011 before any deficit-reduction agreements or sequestration. The new caps on discretionary spending enacted in the 2011 Budget Control Act saved money, but the savings were wiped out by additional spending and tax cuts enacted as part of the fiscal cliff deal last January.

Source: Congressional Budget Office

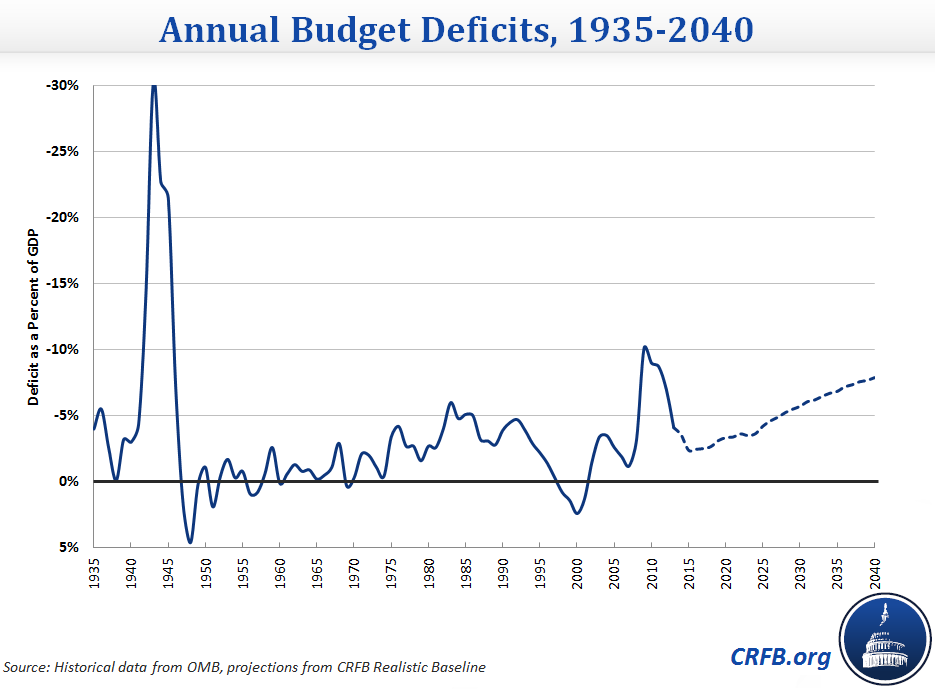

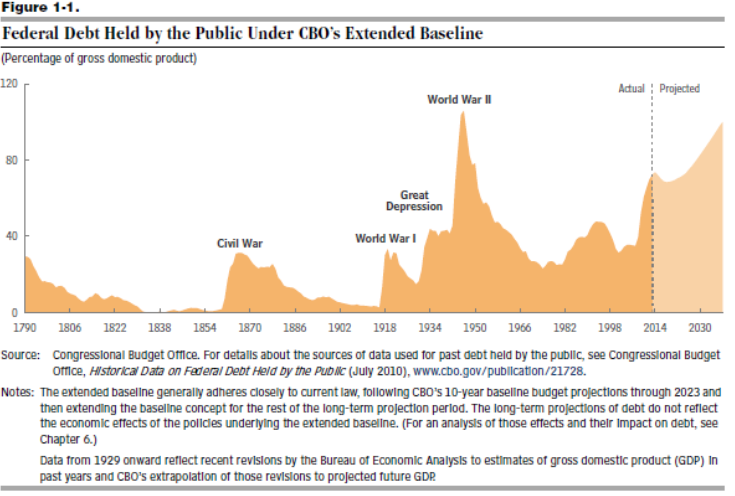

Even though our deficit is projected to shrink over the next few years, the predictions for the future decades have not gotten any rosier. Unlike World War II, when budget deficits were projected to decline dramatically due to a combination of ending the war, US global dominance, an expanding labor force, and decades of close-to-balanced budgets, our debt is now projected to rise unsustainably for the foreseeable future. Health care cost growth, an aging population, and rising interest costs all threaten to increase the debt, which is projected to rise to World War II levels by 2040. This rising path will be difficult to reverse unless lawmakers are willing to look at all parts of the budget, in particular entitlement and tax reform.

Source: Congressional Budget Office

The solution should not myopically focus only on short-term spending cuts like the sequester, which cut indicriminately, hurt economic growth, and only produce savings over the next few years without addressing the long-term drivers of our debt: health care costs and population aging. The solution should be focused on responsible, targeted, long-term savings, even if the short-term savings are more modest. The budget conference committee began negotiations yesterday, and hopefully will begin to tackle these issues. Along with agreeing to a budget for FY 2014, we hope they will focus on policies that can produce long-term savings to address our long-term debt challenges.

To see more of CRFB's recommendations, see our paper What We Expect From the Budget Conference Committee.