$200 Billion in Mandatory Savings Should Not Be Too Difficult

One of the debates preceding the House Budget resolution was whether the resolution should call for $200 billion of mandatory savings. This week's release of the House Republican budget includes these instructions, providing for deficit-neutral tax reform and $203 billion in mandatory savings.

Several weeks ago, twenty members of the Tuesday Group, a moderate House Republican caucus, signed a letter expressing concerns:

While fiscal responsibility and long-term budget stability is essential, requiring hundreds of billions – as much as $200 billion by some accounts – in budget savings from mandatory spending programs in the reconciliation package is not practical and will make enacting tax reform even more difficult than it already will be.

Committee for a Responsible Federal Budget President Maya MacGuineas wrote this week to Reps. Charlie Dent (R-PA) and Elise Stefanik (R-NY), leaders of the Tuesday Group, to encourage support for $200 billion in mandatory savings in the FY 2018 budget resolution, which it ultimately did.

MacGuineas put the $200 billion in context:

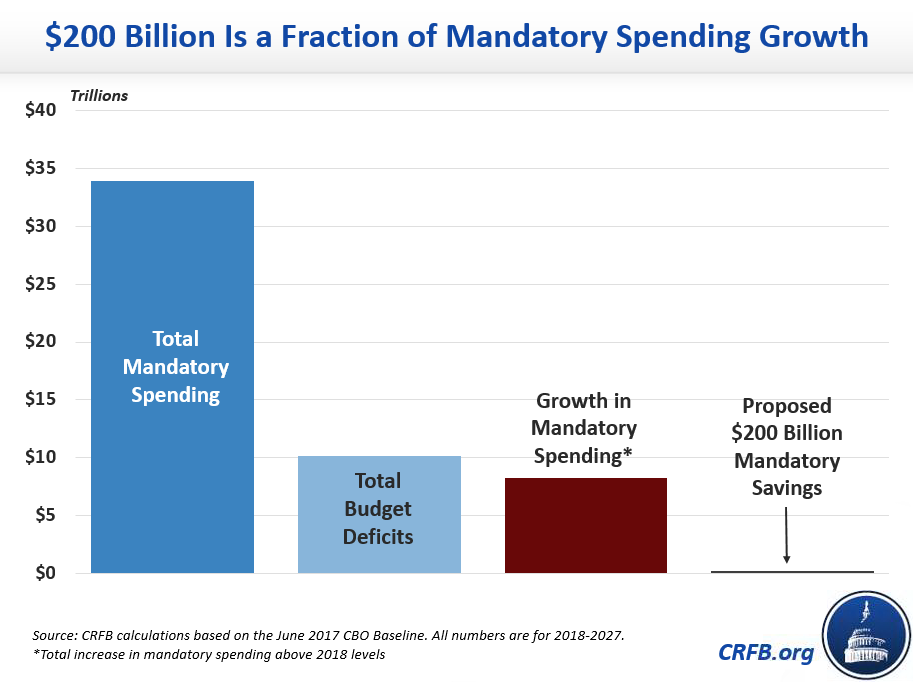

Some have argued that mandatory savings of $200 billion over 10 years is too politically difficult to achieve. If that were true, it would be a dire sign for the fiscal health of our country. The proposed $200 billion in savings is less than one-fiftieth of the $10.9 trillion the Congressional Budget Office (CBO) projects we will add to the debt over the next decade if lawmakers do not act.

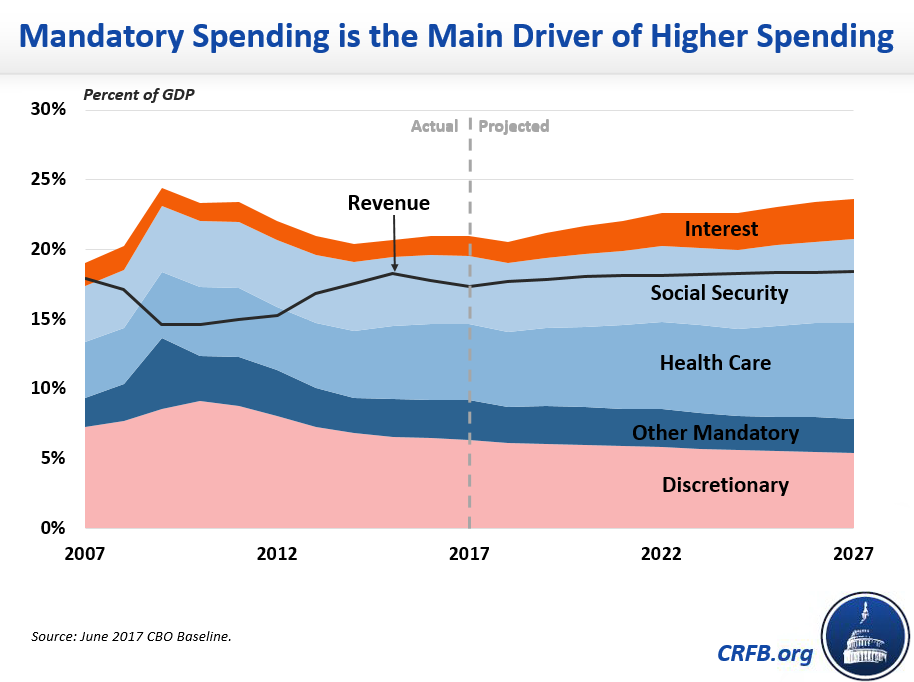

Mandatory spending is a primary driver of growing spending and budget deficits. It is projected to increase from $2.5 trillion in 2017 (13.3 percent of GDP) to $4.3 trillion in 2027 (15.4 of GDP), accounting for 68 percent of nominal spending growth. As a percent of GDP, mandatory spending accounts for 78 percent of spending growth.

MacGuineas stressed the need to specifically address mandatory spending in the budget:

It is imperative that Congress take action to start controlling the growth of mandatory spending to deal with the growing debt and reduce the pressure to cut discretionary spending further.

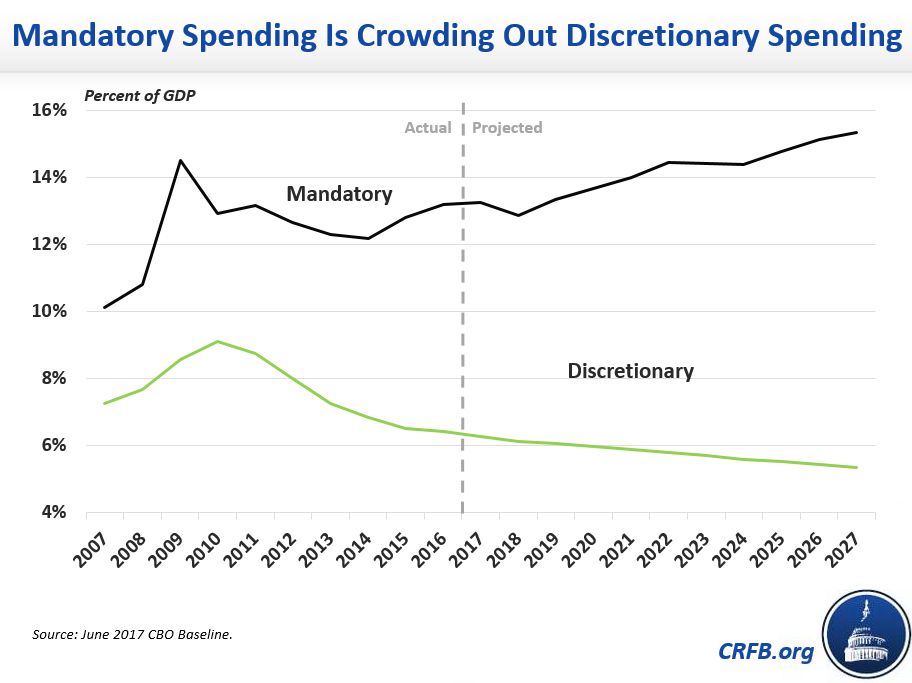

Mandatory spending is projected to crowd out discretionary spending, which is currently on track to fall to 5.4 percent of GDP – its lowest level in modern history.

If Congress continues to ignore mandatory spending growth, MacGuineas warned of dire consequences for discretionary spending programs:

Discretionary spending is effectively being squeezed out by the growth of mandatory spending, as the failure of Congress to take action to reduce the growth of mandatory spending results in increasing pressure to cut discretionary spending.

Including $200 billion in mandatory savings is a necessary but not sufficient step to addressing mandatory spending growth. MacGuineas emphasized the budget resolution as a vehicle for making these fiscal choices:

Previous budget resolutions have assumed several trillion dollars of mandatory savings to achieve balance. Reconciliation instructions requiring a small down payment toward the savings assumed in the budget are essential to the credibility of the budget.

In fact, $200 billion of mandatory savings is only a drop in the bucket of total mandatory spending.

MacGuineas went on to point out that there are plenty of bipartisan policy options available to achieve $200 billion in savings:

We have identified $200 billion in policies from Trump’s budget that were part of Obama’s budget, as well as another $75 billion from earlier Obama budgets. We have also found significant savings from Medicare reforms that save money without reducing benefits.

Further, there are other benefits to mandatory savings that might facilitate a future agreement:

Reconciliation instructions for mandatory savings could facilitate an agreement dealing with sequestration and the debt limit through regular order. The committees of jurisdiction would produce policies to achieve mandatory offsets that could accompany an increase in discretionary spending limits and the debt limit.

Earlier this year, MacGuineas sent a letter to House Budget Committee Chairman Diane Black (R-TN) and Senate Budget Committee Chairman Mike Enzi (R-WY) urging them to focus on the debt in this year’s budget resolutions. We also released a set of principles for a fiscally responsible FY 18 budget.

In her letter to the Tuesday Group, MacGuineas argued that mandatory savings be used to reduce the deficit and not to pay for fiscally irresponsible tax cuts:

In order to ensure that mandatory savings go to deficit reduction, the budget resolution must not allow tax reform to reduce revenues below the levels projected under current law. The budget resolution should not facilitate an increase in the deficit through reconciliation instructions for a reduction in revenues or use of a current policy baseline for tax reform.

By including reconciliation instructions for $203 billion in mandatory savings and a target of deficit-neutral tax reform, the House budget resolution is adopting an achievable target and a solid first step, even if more work will ultimately be needed.

Read the full letter here.