Analysis of the 2020 Social Security Trustees' Report

Today, the Social Security Trustees released their annual report, showing that Social Security faces a precarious and worsening financial situation – even before accounting for the current public health crisis. The novel coronavirus (COVID-19) pandemic is likely to further worsen the program’s finances, mainly by depressing payroll tax revenue.

Before incorporating any economic or health consequences of the pandemic into their projections, the Social Security Trustees found:

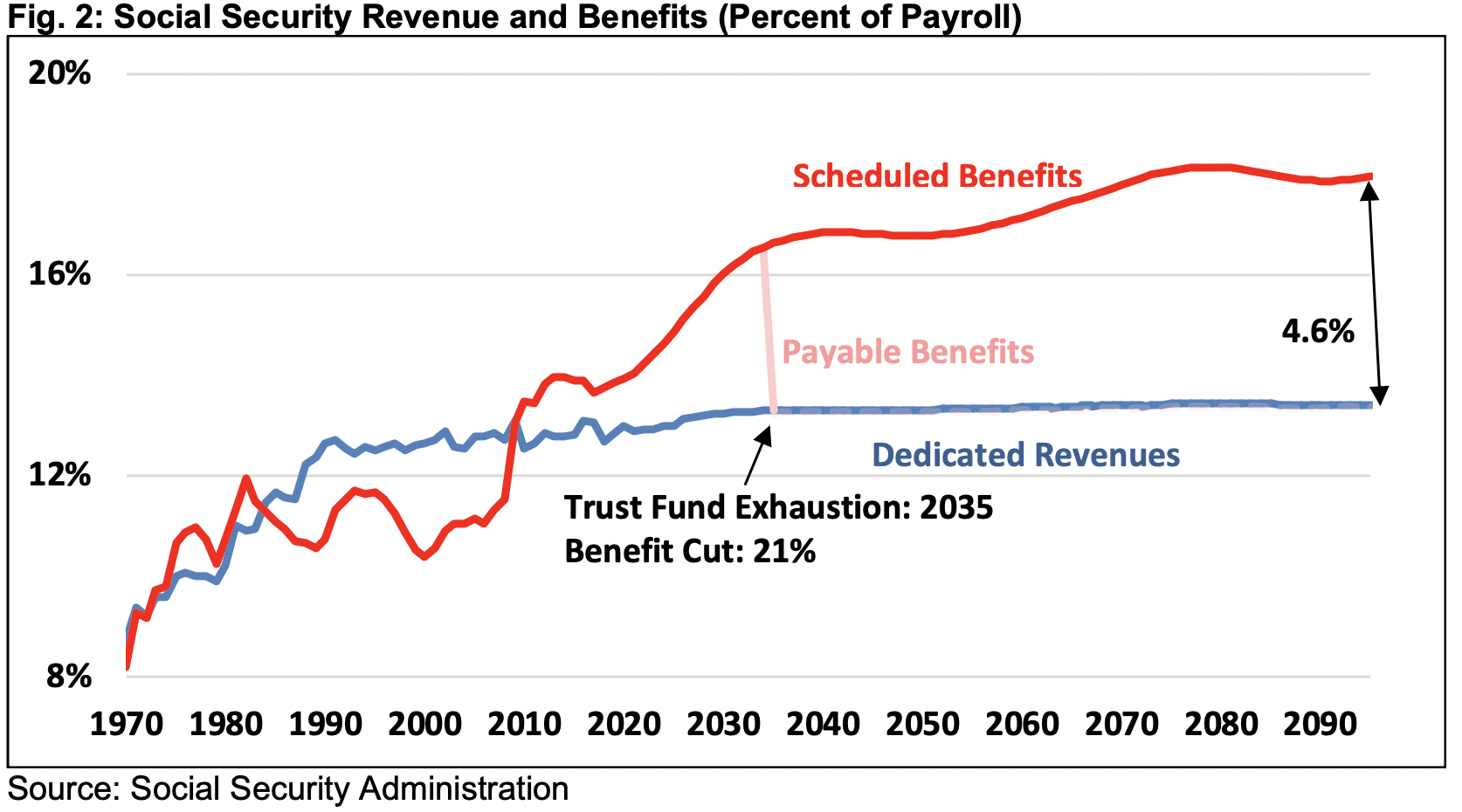

- Social Security Will Be Insolvent in Only 15 Years. Under current law, Social Security cannot guarantee full benefits for current retirees. The Trustees project that the theoretical combined trust funds will exhaust their reserves by 2035, when today’s 52-year-olds reach the full retirement age and today’s youngest retirees turn 77. Upon insolvency, all beneficiaries will face a 21 percent across-the-board benefit cut that will ultimately grow to 27 percent. The current crisis will almost certainly advance the date of insolvency by several years.

- Social Security Faces Large and Rising Imbalances. Prior to the current crisis, the Trustees projected Social Security program would run cash deficits of more than $2 trillion over the next decade, the equivalent of 2 percent of payroll or 0.7 percent of Gross Domestic Product (GDP). Program deficits will exceed 3.5 percent of payroll (1.2 percent of GDP) by 2040 and 4.5 percent of payroll (1.5 percent of GDP) by 2094. Social Security’s 75-year actuarial imbalance totals 3.21 percent of taxable payroll, which is 1.1 percent of GDP or $17.8 trillion in present value terms.

- Social Security’s Finances are Deteriorating. Between 2010 and 2019, the program’s actuarial deficit grew by nearly 50 percent from 1.92 percent of payroll to 2.78 percent. Over the past year, it has grown by an additional 15 percent to 3.21 percent of payroll. This projection does not account for the effects of the COVID-19 pandemic, which will significantly worsen the shortfall.

- Time is Running Out to Save Social Security. Once the current crisis passes, lawmakers will have only a few years to restore solvency to the program. Tax and spending adjustments will need to be phased in far more abruptly than is desirable. The longer action is delayed, the fewer options will be available and the more painful changes will be.

Given the short timeline to address the looming insolvency of Social Security – and of Medicare Hospital Insurance (Part A) – policymakers should support bipartisan efforts to improve these programs and restore them to long-term balance.

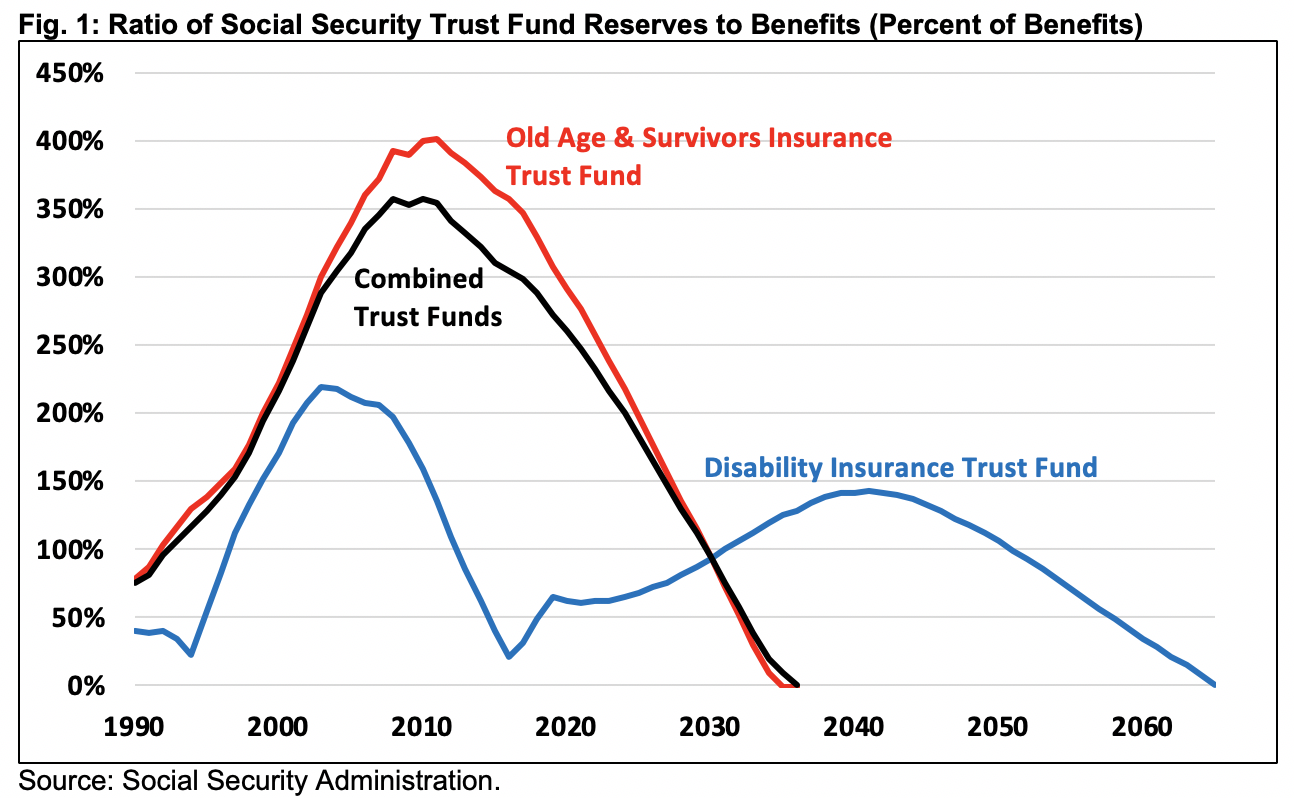

Social Security is Approaching Insolvency

Before incorporating the adverse effects of the COVID-19 crisis, the Social Security Trustees project the program is only 15 years from insolvency.

They project the Old-Age & Survivors Insurance (OASI) trust fund will deplete its reserves by 2034, while the Social Security Disability Insurance (SSDI) trust fund is projected to be exhausted by 2065. On a theoretical combined basis – assuming revenue is reallocated between the funds in the years between OASI and SSDI insolvency – Social Security will become insolvent by 2035.

Upon insolvency, all beneficiaries regardless of age, income, or need will face a 21 percent across-the-board benefit cut, which will grow to 27 percent by the end of the projection window.

The year 2035 is only 15 years away. That means the trust funds will run out of reserves when today’s 52-year-olds reach the normal retirement age and today’s youngest retirees turn 77. For perspective, the average new retiree will live to age 85, meaning Social Security cannot guarantee full benefits for many current retirees, let alone future beneficiaries (See How Old You Will Be When Social Security’s Funds Run Out).

In reality, the situation is far worse. The current economic crisis will dramatically reduce payroll tax revenue this year and beyond; it is also likely to increase disability applications. As a result, Social Security Disability Insurance is likely to be insolvent decades earlier than the Trustees project – perhaps in the 2020s – and the old age program several years earlier than projected.

Social Security Faces a Large and Growing Shortfall

The Social Security Trustees project the program will run ongoing deficits. This year, the Trustees estimate the program will run a cash-flow deficit of $73 billion. However, if the current crisis leads payroll tax revenue to fall 10 percent in 2020 (as an example), that deficit would expand to $177 billion. From 2021 through 2030, the Trustees project $2 trillion of cumulative deficits.

Over the longer term, the Trustees project Social Security’s cash shortfall (assuming full benefits are paid) will expand from 0.9 percent of payroll (0.3 percent of GDP) in 2020 to 2.8 percent of payroll (1.0 percent of GDP) by 2030, 3.5 percent of payroll (1.2 percent of GDP) by 2040, and 4.5 percent of payroll (1.5 percent of GDP) by 2094.

This rising shortfall is the result of continued benefit growth, most of which is due to the aging of the population. The program’s costs have risen from 10.4 percent of payroll in 2000 to 13.9 percent of payroll today and are projected to rise further to 16 percent of payroll by 2030 and 17.9 percent of payroll by 2094. Revenue will fail to keep up, rising only slightly from 13 percent of payroll today to 13.4 percent of payroll by 2094.

Generally, the Trustees measure Social Security's financial imbalance over 75 years. They find the program faces an actuarial shortfall of 3.21 percent of payroll, which is 1.1 percent of GDP or $17.8 trillion on a present value basis. That assumes no impact from the current crisis.

A plan to restore sustainable solvency would require the equivalent of increasing payroll taxes by one-quarter over the next 75 years and by one-third in the 75th year, reducing spending by one-fifth over 75 years and by one-quarter in the 75th year, or some combination. Actual reforms could be well targeted, rather than across-the-board, and phased in more gradually.

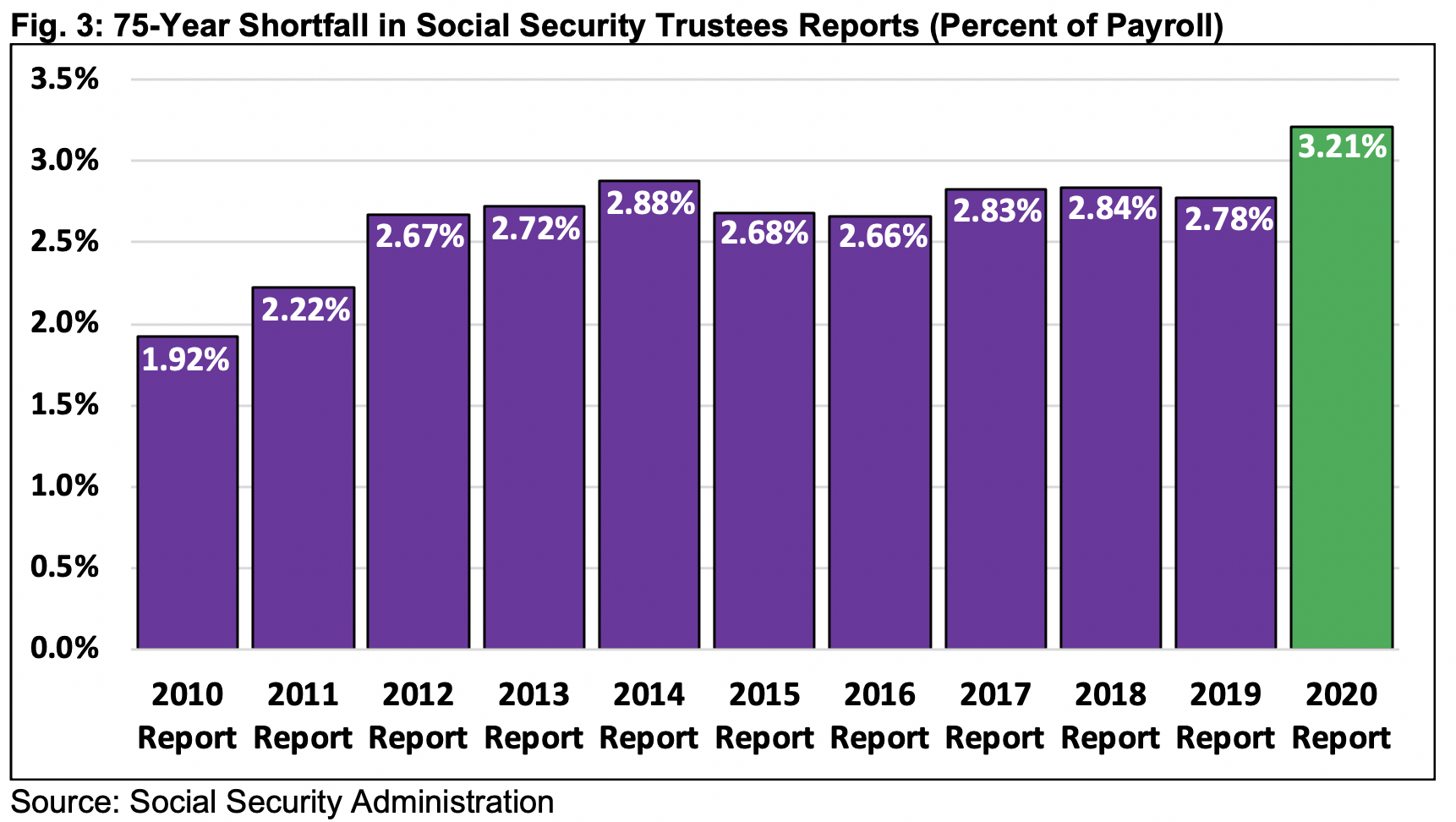

Social Security’s Finances Have Deteriorated and Will Only Get Worse

Social Security’s overall finances have worsened substantially over the past year and over the past decade. As a share of payroll, the projected 75-year shortfall is 15 percent worse than a year ago and 67 percent worse than it was in 2010. When the effects of the current crisis are incorporated, the financial state of the program will deteriorate further.

Back in 2010, the Trustees estimated the Social Security trust funds would be exhausted by 2037, and the program faced a 75-year shortfall of 1.92 percent of payroll. That shortfall rose to 2.22 percent of payroll in the 2011 Trustees Report, 2.67 in 2012, 2.78 by 2019, and 3.21 percent of payroll in the 2020 Trustees report. Meanwhile, the projected exhaustion date is now 2035, meaning the trust funds are 15 years from insolvency today compared to 27 years back in 2010.

Importantly, these projections do not take into account the negative effects of the current economic and public health crisis, which are likely to push the 75-year shortfall beyond 3.21 percent and the insolvency date up to the early 2030s or perhaps the late 2020s.

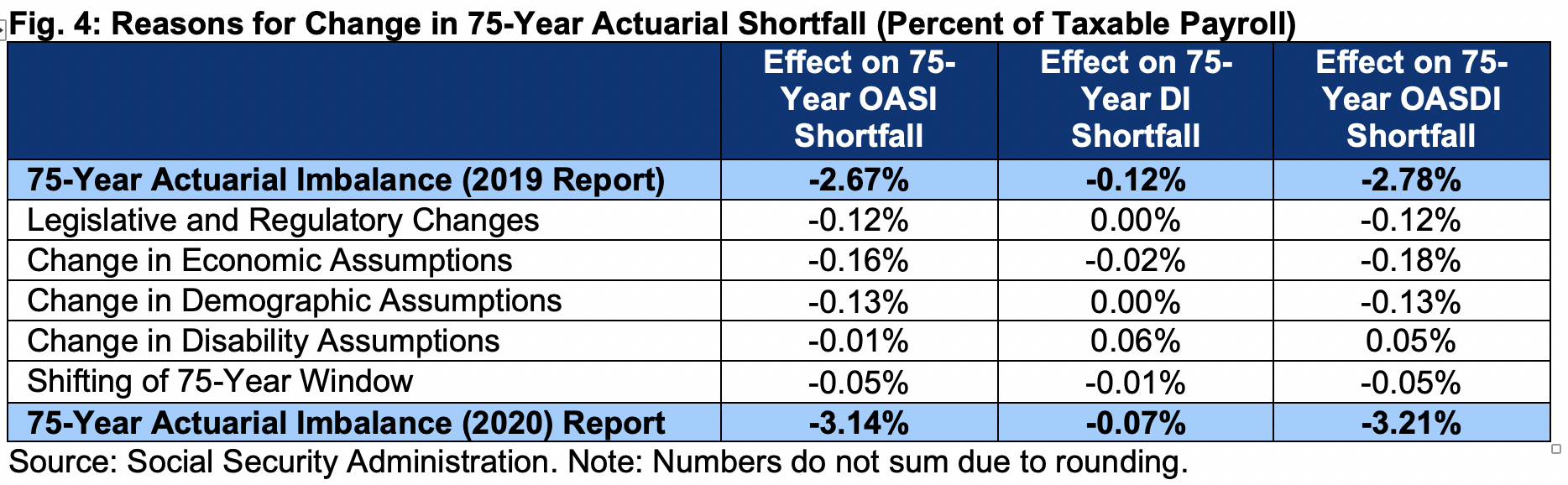

The 0.43 percent of payroll (15 percent) deterioration in the long-term finances of the program has been driven by several factors. Legislatively, the repeal of the Cadillac tax in last December's appropriations package is projected to result in more rapid growth of health insurance premiums, leading to slower wage growth and thus fewer wages subject to the payroll tax. The Trustees project the shortfall will widen by about 0.12 percentage points of payroll as a result.

Changes in economic assumptions, meanwhile, added 0.18 percentage points to the actuarial shortfall. This includes assuming that inflation will average 2.4 percent as opposed to 2.6 (accounting for 0.05 percent of payroll), real interest rates will fall from 2.5 to 2.3 percent (accounting for 0.07 percent of payroll), and economic output will be somewhat lower than previously estimated.

New demographic assumptions, meanwhile, increased the 75-year shortfall by 0.13 percentage points, mainly as a result of lower birth rates. Other factors, such as slightly higher estimates of new lawful permanent residents and higher death rates, mostly offset each other.

Finally, the program’s 75-year shortfall saw a 0.05 percentage point deterioration due to the new projection window. Including the year 2094, in which the Trustees project an annual shortfall of 4.51 percent of payroll, worsens the overall 75-year actuarial imbalance.

Partially offsetting these factors, the Trustees assume a reduction in current and projected disability applicants and awardees, building on the good news from last year. This improves the actuarial balance by 0.5 percentage points.

While the Trustees note that disability incidence rates have continued to fall well below expectations, this trend is unfortunately likely to reverse as a result of the current economic and public health crisis. COVID-19 itself is likely to increase the number of Americans with disabilities. Meanwhile, the deteriorating state of the economy is likely to dramatically reduce the number of jobs available for workers with disabilities, many of whom will instead turn to the SSDI program.

Policymakers should continue to support improvements to disability programs, particularly those that can help to support individuals with disabilities to remain in or return to the workforce, but even with these efforts, the disability rolls are likely to swell.

Once the Trustees update their projections to incorporate the current crisis, we expect to see both this disability assumption and overall economic assumptions worsen significantly. In particular, wages, inflation, interest rates, and gross domestic product are all likely to be lower, while unemployment will be higher. In the coming weeks, we will develop preliminary estimates of how these changes might affect Social Security.

Delaying Fixes to Social Security is Costly

Policymakers must slow Social Security’s cost growth, increase the program’s revenue sources, or do some combination. Changes should be made promptly, given the high cost of delay.

The sole recommendation of the Trustees is that “lawmakers address the projected trust fund shortfalls in a timely way in order to phase in necessary changes gradually and give workers and beneficiaries time to adjust to them” and “allow more generations to share in the needed revenue increases or reductions in scheduled benefits.” Early action would also allow policymakers more choices to target adjustments, enhance benefits for some, and structure more pro-growth reforms.

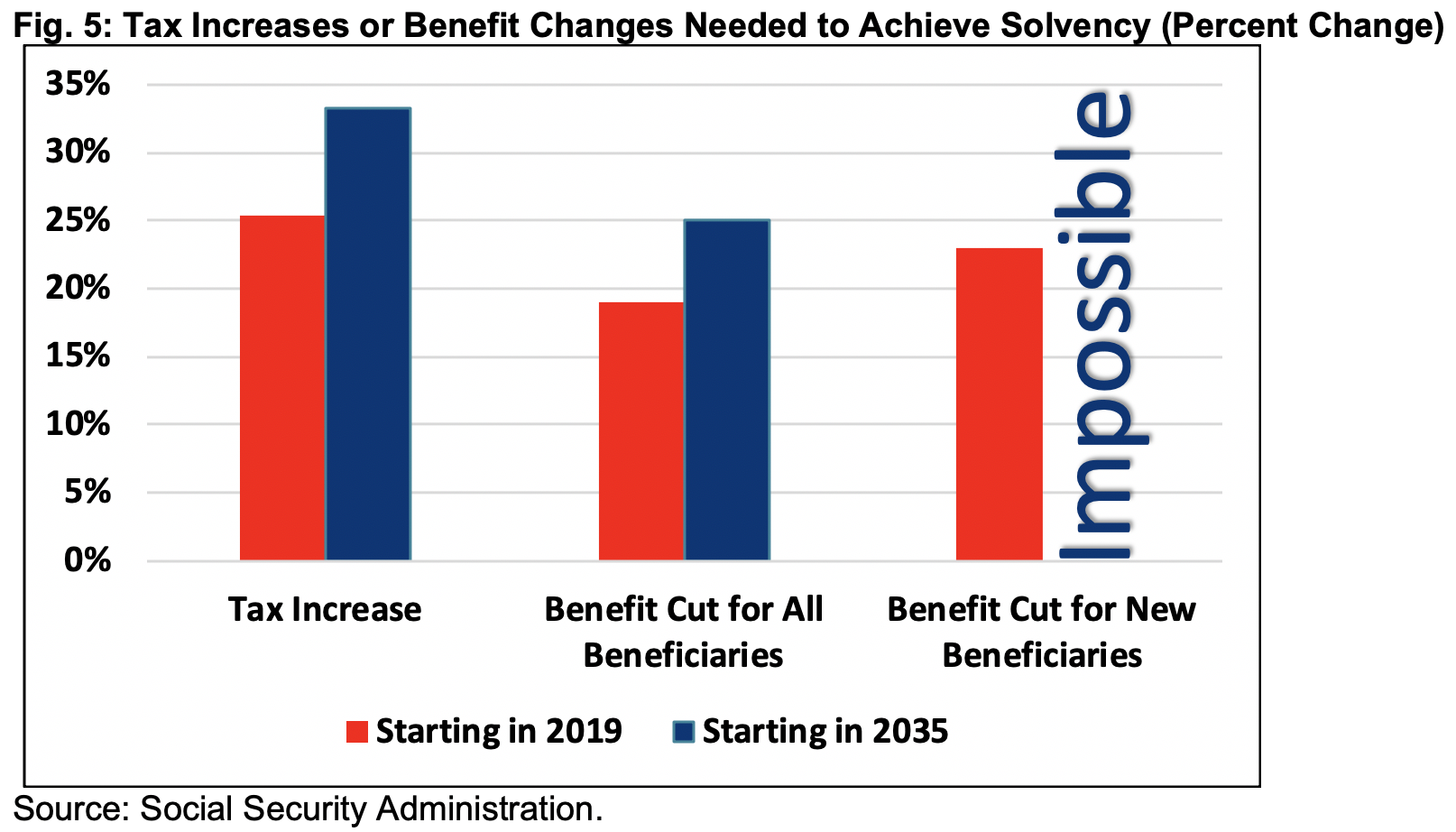

Delaying reform until 2035 would increase the magnitude of needed tax increases or benefit reductions by almost one-third. According to the Trustees, 75-year solvency could be achieved with the equivalent of a 25 percent (3.1 percentage point) payroll tax increase today but would require a 33 percent (4.1 percentage point) tax increase in 2035. Similarly, Social Security solvency could be achieved with a 19 percent across-the-board benefit cut today, which would rise to 25 percent by 2035. Cuts to new beneficiaries only would need to be 23 percent today, but even eliminating benefits for new beneficiaries in 2035 would not be enough to avoid insolvency.

Many options exist to secure Social Security. The Social Security 2100 Act from the left, the Social Security Reform Act from the right, and the Conrad-Lockhart plan from the center would all restore sustainable solvency. Other proposals could be designed with our Social Security Reformer tool.

To expedite action, the Time to Rescue United States Trusts (TRUST) Act would establish bipartisan commissions to ensure Social Security, Medicare, and highway program solvency. Policymakers should consider this or a similar approach in order to reach consensus sooner rather than later.

Conclusion

The Social Security Trustees continue to warn that the program is significantly out of balance and only a few years from insolvency. Excluding the adverse effects of the current economic and public health crisis, Social Security will not to be able to pay full benefits to many current beneficiaries, let alone today’s workers and future generations. Action must be taken soon to avoid a 21 percent across-the-board cut to all beneficiaries in 15 years or less.

Incorporating the economic and health consequences of the COVID-19 pandemic will likely lower payroll tax revenue, increase disability claims, accelerate collection of early retirement benefits, and reduce the interest accumulating on trust fund reserves. This will almost certainly accelerate the trust fund insolvency date and could worsen the long-term outlook as well.

Fortunately, many well-known options to fix Social Security’s finances exist and could be enacted and implemented with political will. A number of comprehensive plans already exist to restore solvency, and our Social Security Reformer Tool allows anyone to design their own. Policymakers should also consider pursuing new, innovative solutions to promote economic growth and improve retirement security in concert with addressing the program’s finances.

Fixing Social Security should not be the top legislative priority right now. But once the country makes it through the current crisis, the Social Security program will be only a few years from insolvency. Action will be needed quickly to secure the program and prevent a massive general revenue bailout or sharp and indiscriminate cuts in benefits.

What's Next

-

Image

-

Image

-

Image