Bipartisan Budget Act Means the Return of Trillion-Dollar Deficits

Lawmakers have passed a budget deal that will increase deficits by $320 billion over a decade or almost $420 billion with interest and sets the stage for adding $2 trillion to the debt over the next ten years if parts of the deal are made permanent.

The deal would significantly increase caps on discretionary spending by $296 billion over the next two years, provide nearly $90 billion in disaster relief, increase spending on health care in multiple ways, and retroactively extend tax breaks that expired at the end of 2016, among other policies. The deal includes roughly $100 billion of offsets, though many are budget gimmicks or one-time savings like selling oil from the Strategic Petroleum Reserve.

This deal is a blow to our nation's fiscal outlook – especially if it is extended permanently. In a statement this morning, CRFB president Maya MacGuineas said,

No one voting for this bill can claim to care about the debt and deficits – in fact, it is fiscal malpractice. Congress just ordered everything on the menu and then some and sent the bill over to the kids' table.

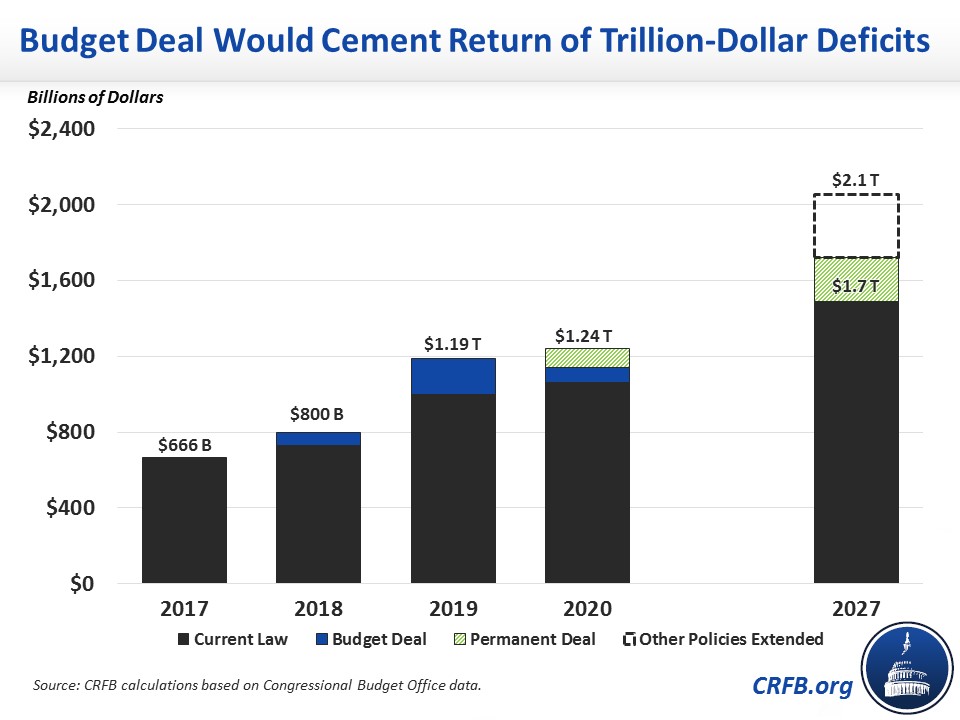

Based on the score from the Congressional Budget Office (CBO), the budget deal would increase next year's deficits to roughly $1.2 trillion. Annual deficits would remain over $1 trillion indefinitely.

It is highly unlikely lawmakers would allow a sharp $125 billion cut to discretionary funding to go into effect in 2020 when the deal expires. If the temporary policies in the deal were made permanent, deficits would rise to $1.7 trillion by 2027. If the recently-enacted tax bill and delays of Affordable Care Act taxes were also made permanent, the 2027 deficit would increase further to $2.1 trillion.

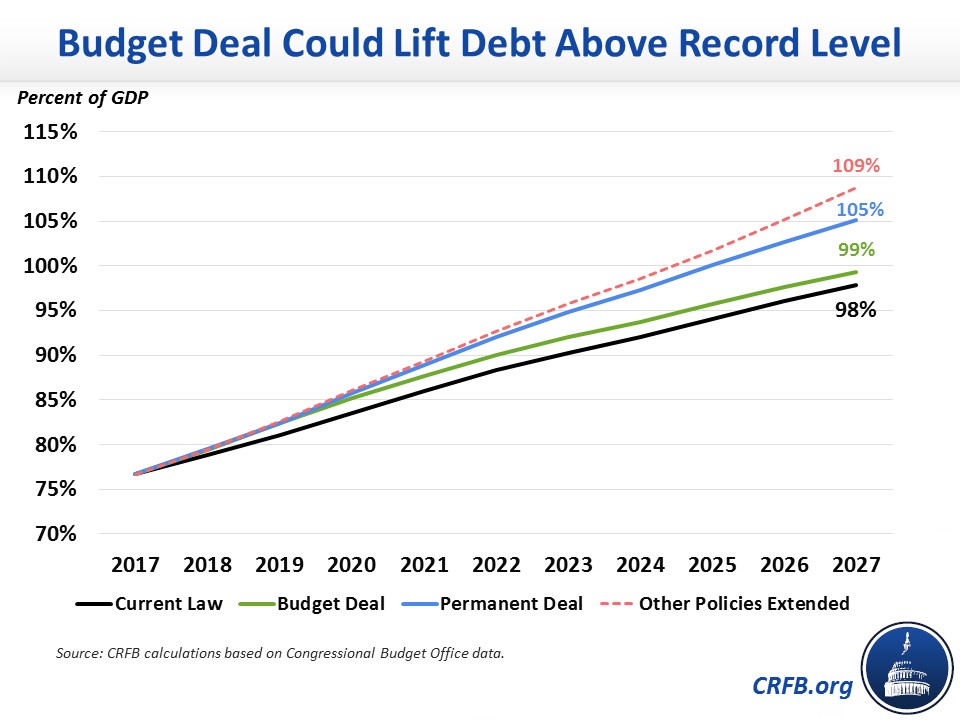

The budget deal itself would cause debt to rise to 99 percent of Gross Domestic Product (GDP) by 2027 – but if made permanent, debt would rise to 105 percent of GDP in 2027. With other tax provisions extended permanently, debt would reach 109 percent of GDP, higher than the previous record of 106 percent of GDP set just after World War II.

After a $1.5 trillion tax cut and with debt already higher than at any time since the World War II era, it is clearly time to get to work on enacting changes that remedy this dismal fiscal situation. Scaling back the tax cut, finding common-sense spending cuts, and enacting reforms to unsustainable entitlement programs will all be key to reversing the harm caused by reckless deficit-financed tax cuts and spending increases.