The Year-End Debt Dilemma

As the year comes to a close, lawmakers have a number of legislative deadlines and a variety of issues they need or want to address – many of which could add to the national debt. In this paper, we show:

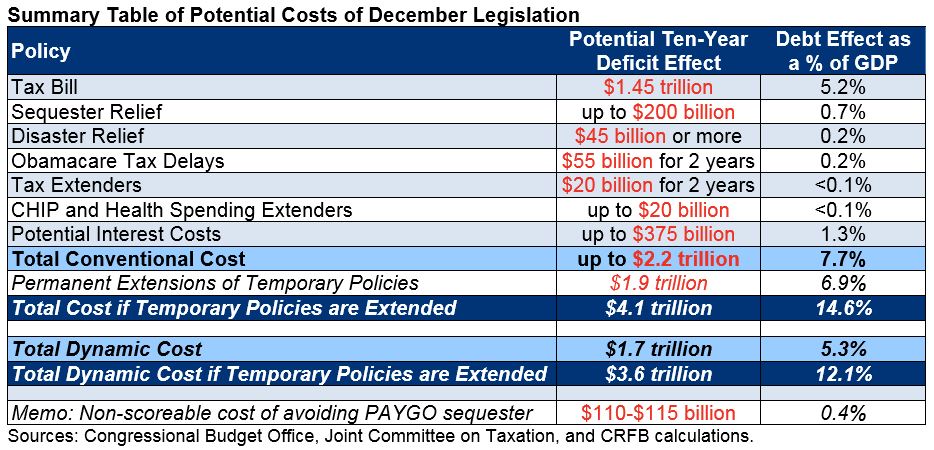

- Congress intends to deal with a number of legislative issues before the end of the year on top of the debt-financed tax cuts, including: discretionary spending levels (“the sequester”), disaster funding, Obamacare tax delays, tax extenders, reauthorization of the Children’s Health Insurance Program (CHIP), extension of other health spending, and the debit on the PAYGO scorecard.

- If these legislative priorities are not paid for, it could add up to $425 billion, or perhaps more, to the debt over the next decade.

- Many of these policies will only be dealt with on a temporary basis. Permanent versions of these policies could end up adding $1.75 trillion to the debt.

- Incorporating debt-financed tax cuts that are made permanent, Congress may ultimately add up to $4.1 trillion to the deficit over a decade, and trillion-dollar deficits could return as soon as next fiscal year.

Debt is Already on Course to Rise Unsustainably

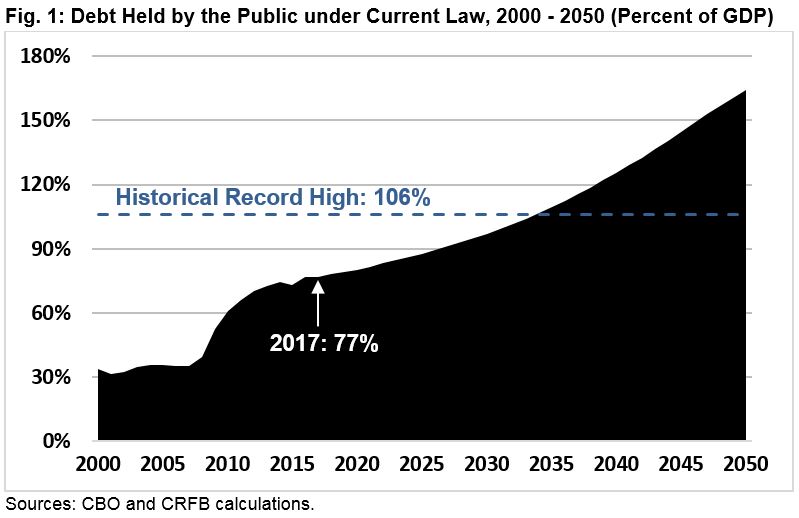

Over the past half century, debt held by the public has averaged about 40 percent of Gross Domestic Product (GDP), and as recently as 2007, it was just 35 percent of GDP. However, as the Great Recession and slow recovery took its toll, the aging of the population began to take root, and lawmakers passed fiscally irresponsible legislation, debt has grown dramatically and is now higher than at any other time apart from just after World War II.

Debt today totals 77 percent of the economy, and the Congressional Budget Office (CBO) projects that it will total 91 percent by 2027 under current law. Without any legislative changes, debt will eclipse its record of 106 percent of GDP by 2035 and exceed 150 percent of GDP before 2050.

According to CBO, “such high and rising debt would have serious negative consequences for the budget and the nation,” including slower economic growth, higher costs of maintaining it with interest payments, less fiscal space to addresses emergencies and vital priorities, and an increased risk of a fiscal crisis.

While the increase in debt over the last decade was largely the result of the Great Recession and responses to it (along with the passage of fiscally irresponsible legislation), the future growth of debt under current law is largely driven by the growth of Social Security, federal health spending, and interest on the debt. Those three categories will make up 83 percent of nominal spending growth over the next decade – and revenue growth won’t keep up under current law and even less so if tax cuts are enacted.

In order to solve these problems, policymakers will need to enact a thoughtful mix of entitlement reforms, revenue increases, and spending cuts that slow the growth of debt while improving growth of the economy.

The Tax Bill Will Increase the National Debt

While tax reform is needed to improve the tax code and promote economic growth, as we’ve pointed out repeatedly, our high level of debt means that tax reform should preferably reduce the debt and at a minimum not add to it. In fact, tax cuts tend to be far less pro-growth than revenue-neutral reform, so fiscal responsibility would also better increase growth.

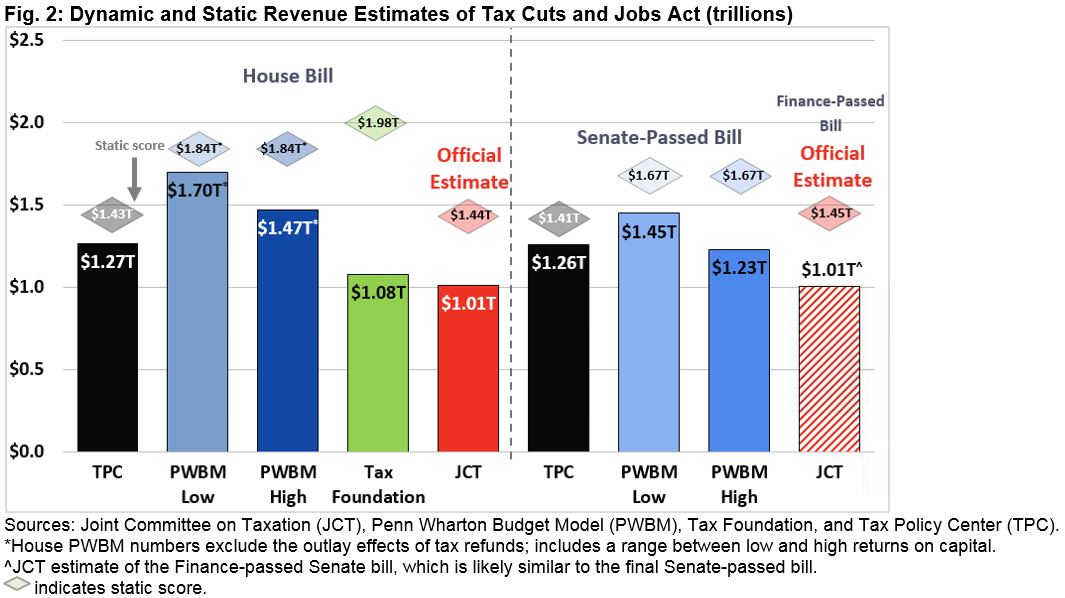

Unfortunately, both the House and Senate tax bills would cost over $1.4 trillion under conventional scoring, or over $1 trillion when accounting for faster economic growth resulting from the bill. Indeed, no outside estimator has found that either tax bill as passed by the House or Senate would cost less than $1 trillion over a decade.

On top of this, both the tax bills contain several gimmicks that mask their true costs by at least half of a trillion dollars over a decade. After interest, tax reform could therefore add anywhere from $1.3 trillion to $2.3 trillion to the debt over the next decade (including interest) depending on how they are measured, which would be on top of the more than $10 trillion debt increase projected under current law through 2027.

As a share of GDP, that means debt could rise from 77 percent today to anywhere from 96 percent to 100 percent by 2027 if lawmakers pass either tax bill.

Year-End Legislation Could Have a High Price Tag

In addition to the push for tax reform, Congress has several deadlines that would require legislation in December – legislation that could add even further to the national debt, including:

Discretionary Spending Cap Sequester Relief. Sequester-level caps on discretionary spending are slated to return for FY 2018 after being raised for the last two years in the Bipartisan Budget Act of 2015. Press reports indicate that lawmakers are proposing a $200 billion deal to both repeal the sequester for the next two years and increase discretionary spending slightly beyond that.

Disaster Funding. Lawmakers have already approved over $50 billion of disaster-related relief for the damage caused by Hurricanes Harvey, Irma, and Maria. They are likely to approve even more assistance (possibly including western wildfire relief as well), with the President already requesting an additional $45 billion just for the hurricanes – and that number may grow further.

Obamacare Tax Delays. The Affordable Care Act’s (ACA or “Obamacare”) medical device tax and health insurers tax will come back into effect next year, and the ACA’s scheduled tightening of medical expense deductibility will go into effect as well. In 2015, lawmakers delayed the first two taxes along with the “Cadillac” tax on high-cost health insurance, which is now scheduled take effect in 2020. Delaying all four of these tax changes for two years would cost $55 billion over ten years.

Tax Extenders. Historically, Congress has regularly continued a number of temporary tax breaks known as “tax extenders.” While the 2015 PATH Act made most of the largest ones permanent and set most of the remaining extenders to expire at the end of 2016, some lawmakers have suggested bringing back these expired tax breaks. Doing so through the end of 2018 would cost roughly $20 billion.

CHIP and Health Spending Extenders. Authorization for CHIP expired at the end of September, and lawmakers in both chambers have proposed five-year reauthorization plans. The House’s plan contains offsets for its cost, while the Senate’s does not. Additionally, several temporary health extenders expire at the end of the year. A five-year CHIP reauthorization and two-year extenders deal would cost about $20 billion.

PAYGO Sequester Waiver. If the tax bill is passed, it would violate Pay-As-You-Go (PAYGO) rules. PAYGO requires legislation to be paid for with offsets over a five- and ten-year period or else trigger a sequester. For 2018, this amount could be over $130 billion, but there is only enough non-exempt spending to cut $110 billion to $115 billion that year. Lawmakers have promised legislation to avoid these cuts. Note that under conventional scoring, there is no scored budgetary cost for canceling or avoiding the PAYGO sequester since that cost is effectively already scored as part of the tax cuts.

If Congress does not pay for any of the policies above (excluding the PAYGO waiver), they could add an additional $425 billion or more to the debt – mostly from policies that would take place over the next year or two (the cost would rise to roughly $550 billion if avoiding a one-year PAYGO sequester were counted).

If these changes were continued permanently, they would add $1.3 trillion to the debt. And that’s on top of the tax bill. Including the tax bill, December legislation could cost up to $2.2 trillion over a decade and set the stage for adding over $4 trillion to the debt.

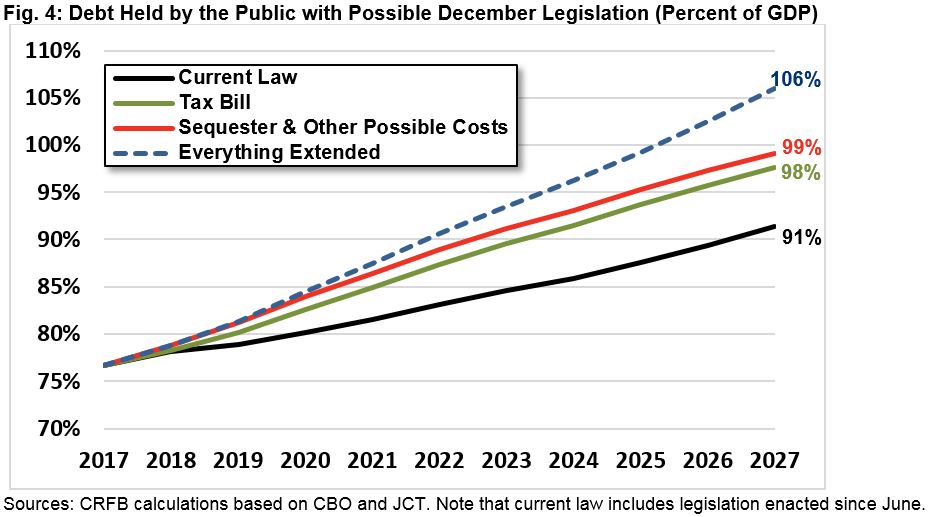

Enacting these policies will bring back trillion-dollar deficits sooner than expected. The tax bill alone would push the return of trillion-dollar deficits to 2020, while enacting all of this legislation without offsets would likely push the deficit to over $1 trillion starting next year (FY 2019).

Adopting a final tax bill alone would also be enough to increase debt held by the public from today’s post-war record high of 77 percent of GDP to 98 percent by 2027 (instead of 91 percent under current law). Adding sequester relief and the other additional policies under consideration without offsets would push this number to 99 percent of GDP by 2027, and debt would exceed the size of the economy the following year.

If all of the temporary policies are made permanent, debt would reach 106 percent of GDP by 2027. This would tie the U.S. record, and debt would likely exceed the record the following year.

Congress Needs to Work to Offset the Costs of Legislation

Taking this fiscal situation seriously will require tough choices and tradeoffs. As noted above, policymakers need to consider entitlement, revenue, and spending changes that ensure the economy and revenue grows faster and spending programs grow slower.

First, it is not too late for lawmakers to make changes to the pending tax bills to make them fiscally responsible. Even including the economic effects of the Senate bill, it would still add over $1 trillion to the debt over the next decade and even more if lawmakers extend the provisions that are set to expire or phase down. There are many solutions to limit the tax bill’s debt effect by taking the best ideas from each bill and enacting additional base broadening.

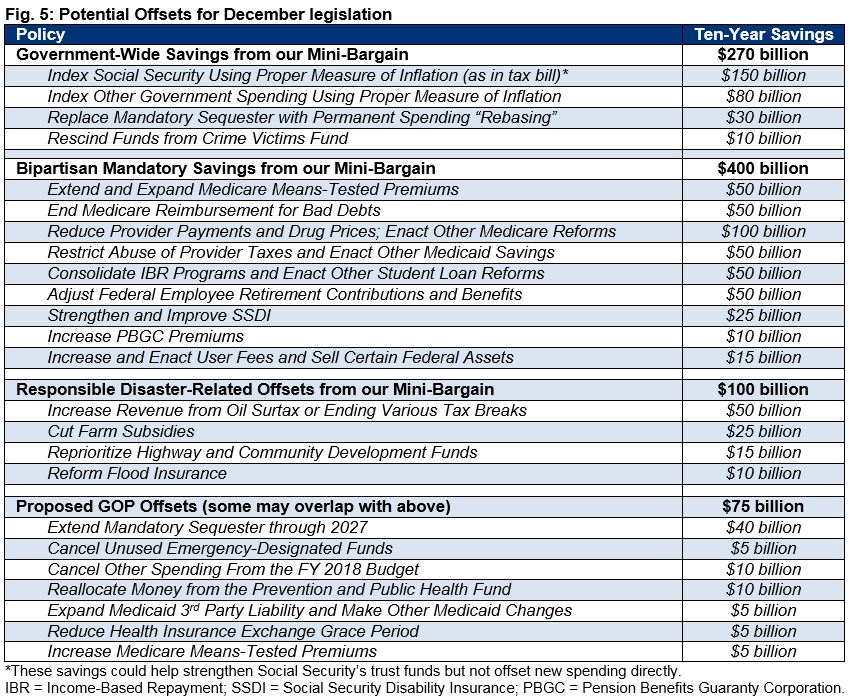

To pay for discretionary sequester relief, lawmakers could look towards savings from our Mini-Bargain to Improve the Budget, which proposes nearly $700 billion of potential savings that could have bipartisan support. Some of these policies include switching all government inflation adjustments over to the more-accurate chained CPI, reducing Medicare and Medicaid cost growth, reforming the student loan program, and adjusting federal employee retirement benefits and contributions, among other options below.

Our Mini-Bargain also offers $100 billion of possible disaster funding offsets by reallocating existing funds, reforming farm subsidies, and cutting fossil fuel tax breaks or enacting an oil surtax. Lawmakers could also look to the $60 billion of potential disaster offsets proposed by the Trump Administration.

When it comes to CHIP and other health extenders, the House-passed bill offers a fiscally responsible set of offsets that both parties should work from to ensure a final package takes steps to slow health care cost growth rather than adding to the debt.

With regard to the Obamacare taxes, Congress should make permanent decisions rather than enacting temporary delays. They could offset the cost of any tax repeals with limits to the tax exclusion for employer-sponsored insurance, reforms to federal health care programs, or alternative revenue or spending cut options.

And in terms of the tax extenders, Congress should allow those not addressed in tax reform to remain expired, as intended under current law.

Finally, assuming debt-financed tax cuts do pass at their current magnitude, policymakers should consider demanding they be scaled back – or a trigger be incorporated into them – in exchange for avoiding the PAYGO sequester.

Conclusion

The national debt is at a post-war record high and rising unsustainably. Fixing the debt will take a bipartisan effort to slow spending growth and increase revenues. The first step, however, is to agree not to make the existing fiscal situation worse.

These unprecedented fiscal challenges present an opportunity for policymakers to come together and restore fiscal sustainability. Doing so is critical to securing both our fiscal and economic futures, and it will increase the resources and flexibility needed to address other critical priorities.