Pro-Growth Infrastructure Needs Concrete Pay-Fors

Policymakers in Washington have turned their attention to infrastructure, with members of both parties putting forward their own competing proposals to boost federal funding for roads, bridges, waterways, and other public works by $200 billion to over $1 trillion over the next decade.

Several analysts have raised concerns over the state of the nation’s infrastructure, and efforts to repair and modernize deficient transportation and communication assets could have a meaningful impact on economic growth.

However, infrastructure should not be the latest addition to the growing list of unpaid-for legislation. Ramping up infrastructure spending without paying for it would not only worsen our already grim budget outlook, it would also undermine the pro-growth effects these proposals might have.

Failure to insist on offsets will also likely reduce the quality of any infrastructure package because lower priority spending is more likely to emerge when it appears costless and tradeoffs need not be considered.

Fortunately, there are numerous options for lawmakers to pay for new infrastructure funding, including several that have received bipartisan support and that could help ensure that public infrastructure assets are used in an efficient manner.

In this explainer, we describe:

- The competing infrastructure plans proposed by President Trump and Senate Democrats,

- Why any new infrastructure funding must be fully paid for if it is to have a meaningful positive impact on economic growth, and

- Potential options for financing new infrastructure initiatives.

Ultimately, increased public infrastructure can be an important element of an overall economic growth strategy. But if the cost of this investment is to increase the country’s already massive levels of debt, it will likely do more harm than good. That is why any infrastructure plan must be paid for in a responsible manner.

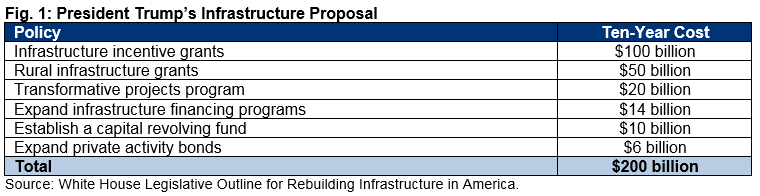

The President’s Infrastructure Plan

President Trump has outlined a proposal to increase federal infrastructure funding by $200 billion over ten years, which the Administration claims will leverage another $1.3 trillion in additional investment from state and local governments and the private sector. The initiative would consist largely of grants and tax incentives to support projects that are likely to eventually generate revenue, such as toll roads or certain transit system improvements.

Specifically, the proposal would include:

- $100 billion in competitive grants awarded to states and localities with promising infrastructure projects that are likely to generate revenue. Grants could not exceed 20 percent of the cost of the project, and no single state could receive more than 10 percent of the total grant funds.

- $50 billion in rural infrastructure grants for states to address various infrastructure needs in rural areas, including nontraditional infrastructure such as broadband internet service. Of the total amount, $40 billion would be provided to states via block grants determined by a formula. The remaining $10 billion would be used for additional performance grants for states that met particular requirements and benchmarks in using their formula funds.

- $20 billion in competitive grants to help cover the demonstration, planning, and construction costs of transformative projects that could be commercially viable but are too risky for private sector investors.

- $14 billion for expanding federal credit programs that help state and local governments finance large-scale infrastructure projects.

- $10 billion to establish a federal capital revolving fund to finance the purchase, construction, or renovation of federally owned civilian property for federal agencies. Agencies would gradually repay the fund over time out of their appropriated budgets instead of requiring a large one-time increase in their appropriations or resorting to leasing the property.

- $6 billion to expand private activity bonds and broaden their eligibility to include a wider range of infrastructure projects.

The initiative also includes some smaller changes, such as creating a new fund to support public lands infrastructure, as well as reforms to expedite the sale of certain federal property and streamline permitting decisions.

The Administration has not identified a specific funding source for the plan, but the President’s budget includes a number of spending cuts that could potentially offset the cost of the proposal (including several reductions to existing infrastructure programs).

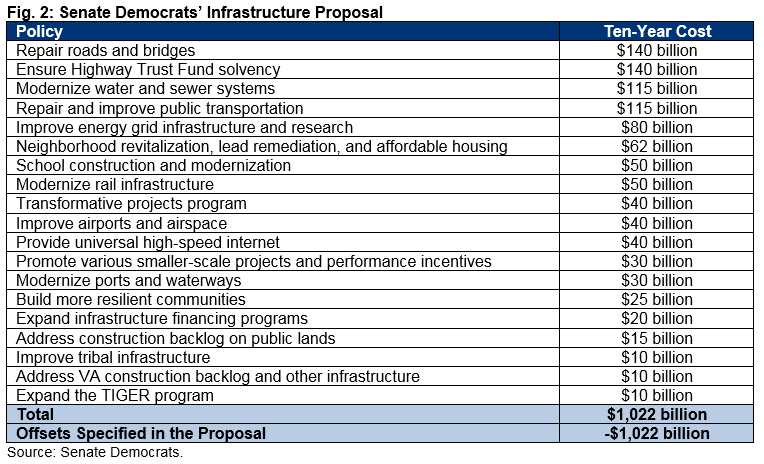

Senate Democrats’ Infrastructure Plan

Democrats in the Senate have released their own plan calling for over $1 trillion in federal infrastructure funding over the next decade. Unlike the President’s plan, the Democrats’ proposal would largely increase infrastructure spending by expanding existing federal programs and tax incentives, though it would create several new programs.

The proposal includes:

- $315 billion to repair and improve ground transportation infrastructure, including $140 billion of grants and direct spending to repair roads and bridges, $115 billion for public transit system maintenance, $50 billion to improve Amtrak and other rail infrastructure, and $10 billion for the Transportation Investment Generating Economic Recovery (TIGER) program.

- $140 billion for the Highway Trust Fund to ensure its solvency through at least 2027.

- $115 billion to modernize water and sewer systems through Environmental Protection Agency and Department of Agriculture grant programs.

- $80 billion to support energy grid improvements and research. The plan would also consolidate most existing renewable energy tax incentives into three new credits.

- $70 billion in spending on air and water transportation infrastructure, with $40 billion allocated for additional Federal Aviation Administration funding and competitive airport improvement grants and $30 billion going towards water, harbor, and seaport projects.

- $70 billion to support large-scale transformative projects ($40 billion) and performance incentives as well as various smaller-scale projects such as bicycle facilities, pedestrian routes, and fueling stations for alternative fuel vehicles ($30 billion).

- $62 billion in additional federal support for affordable housing and lead remediation initiatives through a combination of direct funding and enhanced tax incentives, such as expanding the Low-Income Housing Tax Credit.

- $50 billion to assist states, school districts, and community colleges in school construction and modernization projects.

- $40 billion to provide universal high-speed internet through a Universal Internet Grant Program and other efforts.

- $25 billion to help communities better prepare for disasters through new grants and loan programs.

- $20 billion for expanding federal infrastructure financing programs and creating a new infrastructure bank to promote private financing of infrastructure.

- $35 billion in additional infrastructure spending, including $15 billion to address public land infrastructure backlogs, $10 billion for VA construction and improvements, and $10 billion to improve tribal infrastructure.

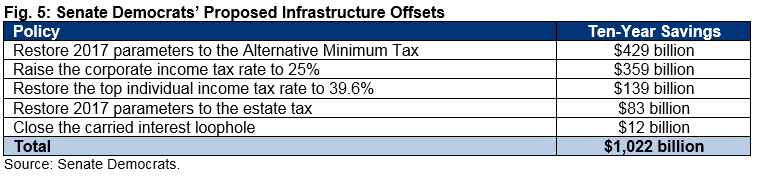

The Senate Democrats’ infrastructure plan also identifies specific offsets that it states would fully pay for its costs, largely by scaling back several provisions of the Tax Cuts and Jobs Act (TCJA). Specifically, it proposes raising the top income tax rate to 39.6 percent ($139 billion), returning the Alternative Minimum Tax ($429 billion) and estate tax ($83 billion) to their 2017 parameters, raising the corporate income tax to 25 percent ($359 billion), and closing the carried interest loophole ($12 billion).

Any New Infrastructure Spending Must Be Paid For

While it is unclear the United States needs an additional $1 trillion or $1.5 trillion of new infrastructure spending, a well-designed package of infrastructure spending can improve public welfare, increase the nation’s capital stock, and thus enhance economic output.

If financed with additional federal borrowing, however, the positive economic effects of infrastructure will shrink or disappear as a result of the growth-impeding effects of higher debt. The benefits of increased public investment will be offset over the long run by reduced private investment.

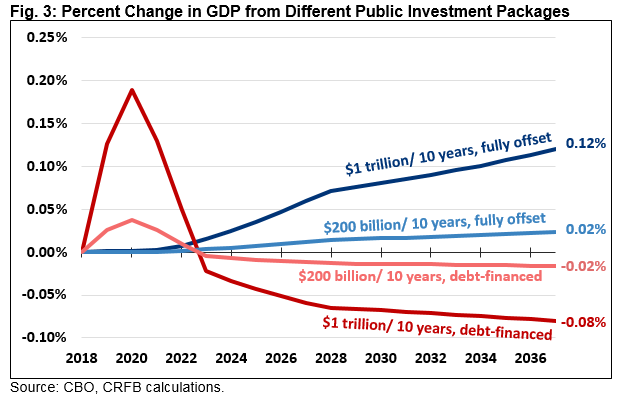

In June 2016, the Congressional Budget Office (CBO) analyzed the impact of a $500 billion increase in federal investment – both paid for and unpaid for. We wrote about that analysis here and here.

Applying CBO’s finding to a generic $1 trillion infrastructure package, we find such a package might increase Gross Domestic Product (GDP) by 0.12 percent after two decades, if offset with growth-neutral pay-fors (some offsets themselves may be pro- or anti-growth). However, if the exact same trillion-dollar infrastructure package were debt financed, it would shrink GDP by 0.08 percent. Similarly, a $200 billion plan with offsets might increase GDP by more than 0.02 percent while an unoffset plan would shrink it by nearly 0.02 percent.

A deficit-financed infrastructure plan would also ultimately add more to the debt than its direct cost, as it would produce higher interest rates and lower GDP, thus increasing federal spending and reducing tax revenues. Based on CBO’s estimates, a $1 trillion increase in infrastructure outlays over a decade would ultimately add roughly $1.2 trillion to the debt when interest and economic feedback are included.

Importantly, these numbers are based on a generic package of investments – in reality, some infrastructure investments are better than others, and some may even produce more in investment than they cost the federal government. However, the Penn Wharton Budget Model (PWBM) reached a similar conclusion in its analysis of the White House’s infrastructure plan (PWBM has not yet analyzed the Senate Democrats’ plan).

PWBM finds that if fully financed with efficient user fees, the President’s infrastructure plan could increase GDP by 0.0 to 0.1 percent. If the plan was paid for with higher debt, however, PWBM finds the impact on GDP would range from virtually nothing to a 0.1 percent decrease over 20 years.

PWBM explains that part of the reason for these low or negative returns is that federal infrastructure grants actually tend to partially crowd out state and local infrastructure spending; the more the federal government spends or offers states to spend on infrastructure, the less states will spend of their own money. In its central estimate, PWBM projects that the President’s proposed $200 billion increase in federal infrastructure spending would increase total public infrastructure spending by $125 billion (their estimates range from $20 billion to $230 billion).

Importantly, the White House has disputed these findings and argued their plan would actually produce more in investment than what it spends. PWBM has responded to this critique. Neither the White House nor the PWBM analysis look at the specific infrastructure investments that might be made under the President’s proposal and what return they might produce.

Still, PWBM’s finding that increased federal infrastructure spending reduces state and local spending is consistent with CBO’s estimate that one-third of federal investment will be offset by reductions at the state and local level and is backed up by a considerable body of research.

Options for Paying for Infrastructure

If greater federal infrastructure spending is to have any chance of meaningfully increasing output, then it needs to be paid for. There are many different options for doing so.

As noted earlier, the Senate Democrats’ plan proposes reversing many of the TCJA’s tax cuts and closing the carried interest loophole. While scaling back the TCJA is a legitimate option for offsetting the infrastructure plan’s costs under pay-as-you-go (PAYGO) rules, it would essentially reallocate rather than reverse the law’s fiscal damage and still ensure the return of trillion-dollar deficits next year. It would be far more preferable to use these savings to reverse the tax law’s increase in the deficit.

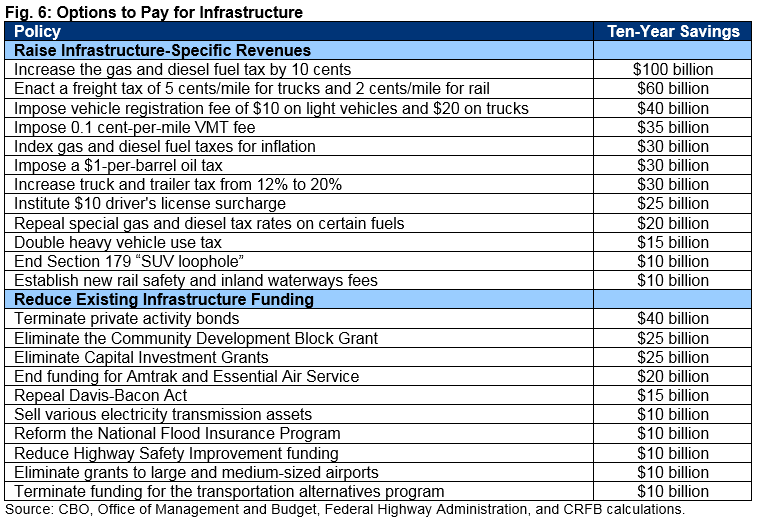

Alternatively, policymakers could raise or levy new infrastructure-specific taxes. For example, the President has floated the idea of increasing the federal gas tax by 25 cents, which could raise around $250 billion. That would be enough to fund his $200 billion infrastructure plan and close about one-third of the Highway Trust Fund shortfall. A higher gas tax is one of many options that abides by the “user pays” principle by requiring those who receive the greatest benefits from new infrastructure investment to pay for it – even if indirectly.

New infrastructure initiatives could also be paid for by reducing spending, including existing infrastructure programs judged as less efficient or lower priority (though some of these options would conflict with elements of either the President’s or Senate Democrats’ proposals).

The table below includes a select set of infrastructure offsets. Most are scaleable – for example, if a $1-per-barrel oil tax raises $30 billion, a $10-per-barrel oil tax would likely raise almost $300 billion. All estimates are rough. Additional transportation related savings options can be found on our website.

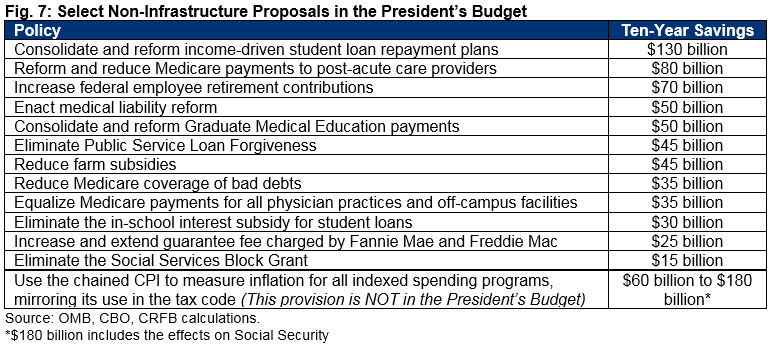

Finally, lawmakers could offset infrastructure spending with savings elsewhere in the budget. The President’s latest budget includes a number of proposals to reduce non-infrastructure spending that could potentially be used as offsets.

Conclusion

Both parties have come forward with distinct proposals to significantly increase infrastructure funding, but neither would have a meaningful impact on sustained economic growth unless appropriately offset with savings elsewhere in the budget.

Importantly, even if new infrastructure spending were fully paid for, the federal budget would still be on an unsustainable fiscal trajectory with trillion-dollar deficits set to return permanently next year. The best strategy for growth would be to pair any increase in public investment with a comprehensive plan to boost labor force participation, encourage innovation, promote investment, and – perhaps most importantly – bring the unsustainable growth of our national debt under control.

Tags

What's Next

-

Image

-

Image

-

Image