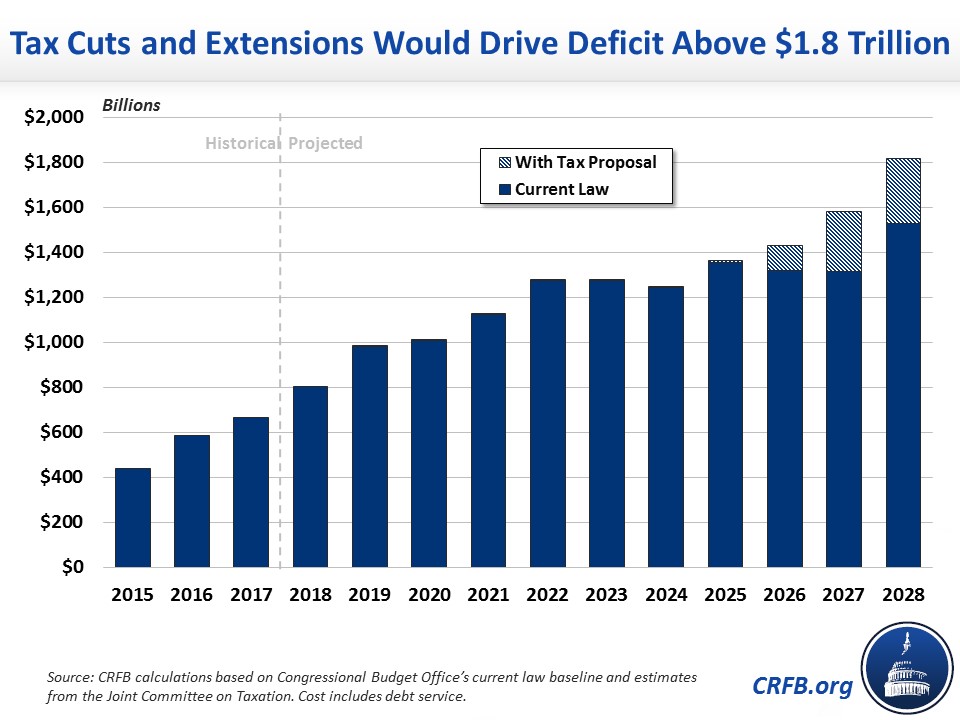

Tax Cut Extensions Would Cost $657 Billion

The House Ways and Means Committee on Monday released three bills they are dubbing "Tax Reform 2.0." The biggest of these bills would extend many of last year's tax cuts permanently while the other two would enact smaller tax cuts. The extensions and new cuts would cost a combined $657 billion over the next decade according to the Joint Committee on Taxation – on top of the tax cut costs already enacted of $1.8 trillion, or $1.9 trillion counting largely offsetting dynamic effects and interest costs.

Most of the non-corporate tax cuts enacted in the December 2017 tax law are set to expire at the end of 2025 as a budget gimmick to reduce the bill's cost and comply with the reconciliation rules that governed the bill's passage. Because current law budget projections include the 2017 tax law, the cost of the extensions is largely in the final three years of the budget window.

As a result of these permanent extensions, the budget deficit in 2028 would be $1.8 trillion, or about $300 billion higher than the $1.5 trillion projected under current law. In dollar terms, 2028's deficit would be more than double the FY 2018 deficit of $800 billion.

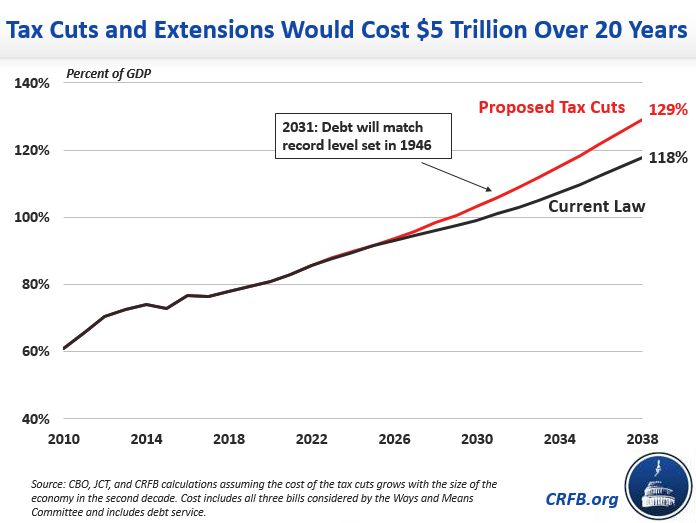

Because the tax cuts are concentrated in the last three years, the bills' costs look artificially smaller over the typically used ten-year budget window. Assuming the tax cuts' costs in 2028 grow along with the economy, they would add roughly $4 trillion to debt over the next 20 years, or $5 trillion with interest.

As a result, debt held by the public would climb to 129 percent of Gross Domestic Product (GDP) by 2038, up from the 118 percent it is projected to reach if the tax cuts were not extended.

By 2031, debt would match the record high of 106 percent of GDP set in 1946 immediately after World War II. Debt would continue climbing thereafter.

In a statement on the bill "Further Tax Cuts are the Height of Fiscal Irresponsibility", CRFB president Maya MacGuineas continued:

The tax cut bill was a sad, missed opportunity. Congress should scrap this plan and pursue real tax reform that broadens the base to finance lower rates, closes loopholes, simplifies the code, and creates lasting economic growth while reducing or at least not worsening the national debt. And while they are at it, they should control spending rather than increase it. Instead, policymakers’ choices seem to grow more irresponsible every day.