President Trump’s Full FY 2018 Budget

The President released the full version of his first budget yesterday, laying out his proposals for Fiscal Year (FY) 2018 and the following decade. The budget proposes significant spending cuts over the next decade, along with extremely optimistic economic growth assumptions, in order to show debt on a downward path.

Our main findings from the budget are:

- The budget proposes about $3.6 trillion of deficit reduction, including $1.5 trillion from largely unspecified discretionary cuts, $2.8 trillion in net mandatory cuts, $1 trillion less in revenue – mainly from repealing and replacing the Affordable Care Act (ACA) – and $300 billion in interest savings.

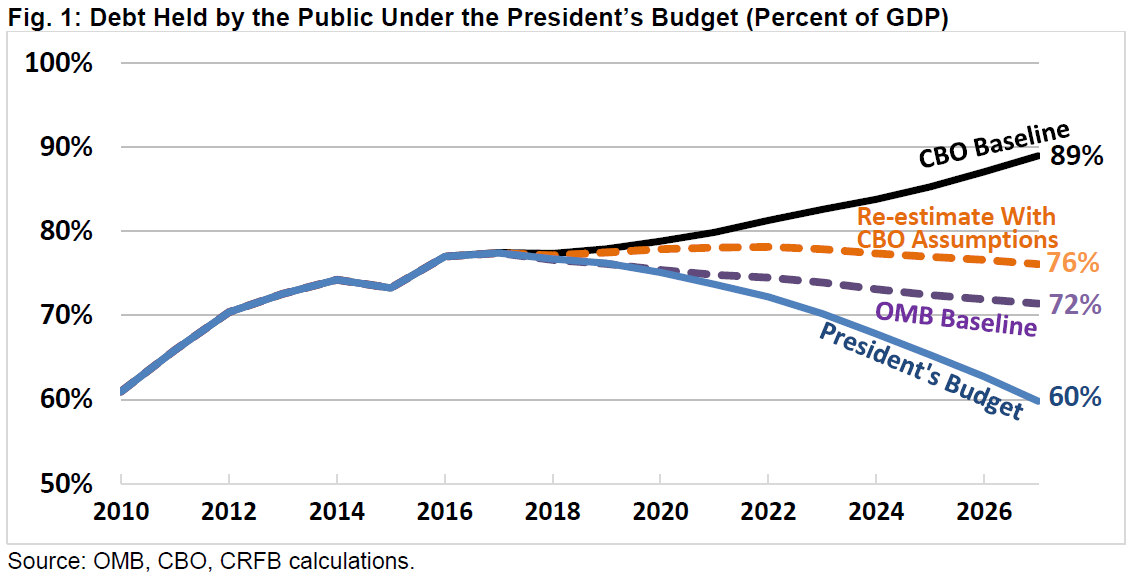

- According to the Office of Management and Budget (OMB), the budget would reduce debt from 77 percent of Gross Domestic Product ($14.8 trillion) today to 60 percent of GDP ($18.6 trillion) by 2027.

- OMB also estimates the budget will balance by 2027, down from a deficit of 3.1 percent of GDP ($603 billion) in 2017.

- To achieve balance, the budget projects spending will shrink from 21.2 percent of GDP ($4.1 trillion) today to 18.4 percent of GDP ($5.7 trillion) by 2027 and revenue will grow from 18.1 percent of GDP ($3.5 trillion) today to 18.4 percent ($5.7 trillion) of GDP by 2027.

- The estimates in the President’s budget are based on overly optimistic economic projections, which we recently estimated are responsible for $2.7 trillion of debt reduction. Using the Congressional Budget Office's (CBO) growth numbers, we found debt under the budget would likely remain stable, and deficits would remain above 2 percent of GDP.

- The budget also relies on a number of unrealistic policy assumptions by assuming deep unspecified non-defense discretionary spending cuts and omitting any details on the President’s potentially costly tax plan.

The President deserves credit for setting a fiscal goal and working to meet it and should be commended for putting forward a number of specific and significant spending cuts to help address the debt.

Unfortunately, these policies are not enough to truly repair our nation’s unsustainable fiscal situation, and the budget does a huge disservice by relying on unrealistic assumptions to get the rest of the way there.

Instead of relying on phony growth and unachievable cuts, the President should focus on controlling the rising costs of Social Security and Medicare, two of the nation’s largest and fastest growing programs, which the budget almost completely ignores. The President should also be serious about tax reform that reduces the deficit – at least on a dynamic basis – rather than simply assuming as much. Tough choices, not wishful thinking, are needed to fix the debt.

Spending, Revenue, Deficits, and Debt in the President’s Budget

According to its own estimates, the President’s budget would achieve balance by 2027, thus dramatically slowing the growth of the national debt.

Specifically, debt would grow from $14.2 trillion today to $18.6 trillion by 2027, compared to $20.6 trillion under OMB’s baseline and $24.9 trillion under CBO’s current law baseline.

As a share of GDP, under the President’s projections, debt would shrink from 77 percent today to 60 percent of GDP by 2027. By comparison, OMB’s baseline projects debt will reach 72 percent of GDP before accounting for spending cuts within the budget (although after assuming 3 percent economic growth), and CBO’s baseline projects debt will reach 89 percent.

Importantly, OMB’s debt projections are significantly reduced by their rosy growth assumptions. We recently estimated that using CBO’s economic assumptions, debt under their budget would rise from $14.2 trillion today to $21.2 trillion by 2027 and remain roughly flat as a share of GDP, reaching 76 percent by 2027.

Under the President’s projections, annual deficits would drop in the first year, climb slightly higher in the second year, and continue to fall over rest of the decade. Deficits would fall from $603 billion in 2017 to $440 billion in 2018, rise to $526 billion in 2019, and ultimately turn into a $16 billion surplus in 2027. As a share of GDP, deficits would shrink from 3.1 percent in 2017 to 2.0 percent by 2021 and turn into a 0.1 percent surplus by 2027. By comparison, OMB’s baseline projects deficits of 2.7 percent of GDP in 2027, and CBO’s baseline projects deficits of 5.0 percent.

However, if the budget used CBO's economic assumptions, we find deficits would total $624 billion (2.2 percent of GDP) in 2027, rather than reaching balance.

To achieve balance, the budget projects that under the President’s policies revenue would grow slowly while spending would fall considerably as a share of the economy. Specifically, spending would fall from 21.2 percent of GDP in 2017 to 18.4 percent by 2027, while revenue would grow from 18.1 percent of GDP in 2017 to 18.4 percent by 2027.

In contrast, revenue in the OMB baseline would climb to 18.8 percent of GDP by 2027 and spending would fall to 21.5 percent. In CBO’s baseline, revenue is at 18.4 percent of GDP by 2027 and spending at 23.4 percent.

Spending decreases are largely driven by cuts to discretionary programs, Medicaid, welfare-related programs, the Social Security Disability Insurance (SSDI) program, other mandatory programs, and drawing down war spending from the overseas contingency operations (OCO) account. These decreases are partially offset by increases to defense and infrastructure spending. Social Security’s Old-Age and Survivors’ Insurance program and Medicare remain largely untouched.

Revenue increases are largely driven by “real bracket creep,” which – particularly in a high-growth environment – leads income to be taxed at higher brackets over time. This increase is partially offset by lower revenue from repealing and replacing the ACA’s taxes and mandates.

The President’s Budget does not include any estimates of tax reform.

At 18.4 percent of GDP in 2027, revenue would be above and spending below historical averages of 17.4 percent and 20.3 percent of GDP, respectively.

Proposals in the President's Budget

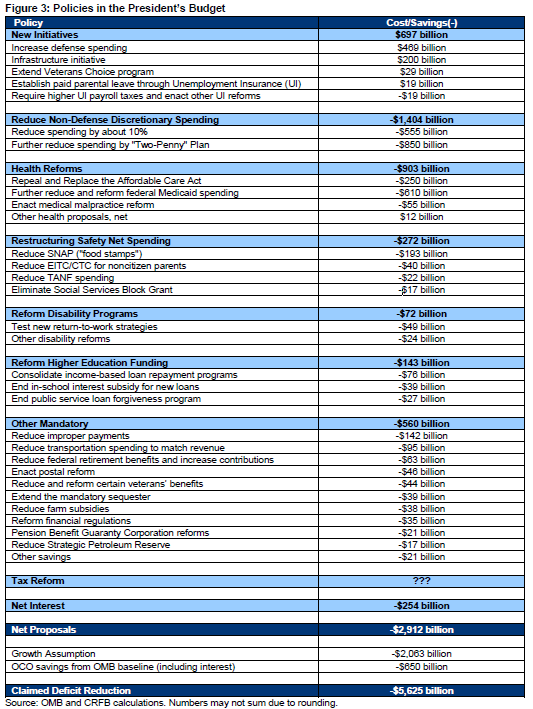

The President’s budget proposed $3.6 trillion of net spending reductions and reforms, the result of $4.5 trillion less in spending and $1 trillion less in revenue over the decade.

Promote New Initiatives ($697 billion) – The President’s budget increases spending on defense discretionary funding, veterans’ health programs, paid family leave, and infrastructure investment. The largest increase in spending comes from the repeal of the defense sequester cuts, which would cost nearly $470 billion. The budget spends another $200 billion as a placeholder for infrastructure investment, which it does not specify but illustrates as grants to state and local governments that hope to leverage $1 trillion of total public-private investment. The budget also includes two other significant spending initiatives. First, it would extend the Veterans Choice program, which allows veterans to choose doctors outside of the traditional VA hospitals if access is overly burdensome. Second, it would allow states to establish paid family leave through the unemployment insurance (UI) program to provide support to new parents for six weeks. To finance its paid leave policy, the Administration would require states to increase their UI payroll taxes while also pursuing several program integrity and back-to-work initiatives.

Reduce Non-Defense Discretionary (NDD) Spending by About 10% (-$555 billion) – As laid out in the “skinny” budget back in March, the President’s budget would reduce non-defense discretionary spending by $54 billion in 2018. The budget specifically identifies items such as eliminating the Low Income Home Energy Assistance Program (LIHEAP), reducing the budget for the National Institutes of Health, eliminating the Community Development Block Grant, ending global health and foreign assistance programs, and defunding the National Housing Trust Fund and Capital Magnet Fund. The budget also calls for very significant cuts to the Departments of State, Health and Human Services, Education, Agriculture and Labor as well as the Environmental Protection Agency. Partially offsetting these cuts, the budget calls for increased funding for the Departments of Justice and Homeland Security, largely for border protection and President Trump’s border wall proposal. Assuming these policies continue over a decade, they would save roughly $550 billion (though actual savings could differ modestly).

Apply the “Two Penny Plan” to Future NDD Spending (-$850 billion) – In addition to the roughly $550 billion of specified non-defense cuts, the budget includes about $850 billion of future unspecified cuts. To achieve these savings on paper, the budget assumes the NDD caps will decline by 2 percent per year below the prior year, even as inflation rises by a similar amount. The budget distributes roughly $120 billion of these savings within the budget functions, and the remaining $730 billion is assumed through “allowances.” As a result of these unspecified reductions, total NDD spending would be 40 percent below baseline levels by 2027 and 1.4 percent of GDP – about one-third the historical average.

Reform Health Care (-$903 billion) – Overall, the budget would reduce projected health spending by about $1.9 trillion, while reducing health-related revenue (mainly from the ACA's taxes and mandates) by $1 trillion, for net savings of $903 billion. The budget assumes $250 billion of net savings from repealing and replacing the ACA, offering support for the broad framework (but not the precise specifics) of the American Health Care Act (AHCA). The budget calls for an additional $610 billion in Medicaid reductions on top of any coming from “repeal and replace.” These savings would come from converting the program into a block grant or per capita cap starting in 2020, which is almost identical to the Medicaid changes already included in the AHCA. Finally, the budget would save about $55 billion from enacting medical malpractice reform to reduce health costs.

Restructure Safety Net Programs (-$272 billion) – The President’s proposes a number of reductions and reforms to safety net programs. Most significant, the budget would reduce the Supplemental Nutrition Assistance Program (SNAP or "food stamps") by $193 billion by limiting eligibility, changing benefit calculations, charging a fee to SNAP-authorized retailers, and requiring states to eventually match one-quarter of all SNAP costs. It would also reduce Temporary Assistance to Needy Families (TANF) grants by 10 percent and eliminate Social Services Block Grants, saving a combined $38 billion. The budget also saves $40 billion by requiring taxpayers to provide a Social Security Number in order to receive the Child Tax Credit and/or Earned Income Tax Credit.

Reform Disability Programs (-$72 billion) – The budget includes a number of changes to the SSDI and Supplemental Security Income (SSI) disability programs. Most significantly, it proposes exploring and testing several strategies to help beneficiaries return to work, such as promoting early intervention from state vocational rehabilitation offices, requiring physical therapy or job-seeking activities for certain applications, expanding wellness care and vocational services, replicating successful state efforts at better coordinating care and job services, and time limiting benefits for certain beneficiaries likely able to return to work. The budget assumes these strategies will eventually save $49 billion once fully implemented, though this estimate appears high. The budget would also make a number of other changes, such as limiting retroactive SSDI benefits, reinstating the reconsideration stage of appeals in all states, offsetting overlapping SSDI and UI payments, and reducing SSI benefits for households with multiple recipients.

Reform Higher Education Funding (-$143 billion) – The President’s budget would simplify and reform how the federal government subsidizes higher education. Specifically, about $76 billion in savings would come from consolidating the current five income-driven loan repayment programs into a single plan with a higher cap on monthly repayments. An additional $39 billion would come from ending a category of loans known as subsidized student loans, which offer an “in-school interest subsidy” that prevents debt from accruing interest so long as a student remains in school. The budget saves $27 billion from ending the program that forgives loan obligations in exchange for a commitment to public service. Additionally, the budget would cancel unobligated carryover funding for Pell grants and reinvest the savings into making Pell grants available year-round.

Other Spending Reductions (-$560 billion) – In addition to the policies above, the President’s budget includes a number of further spending reductions and reforms. The largest savings comes from an assumed halving of improper government payments, which they estimate will save $142 billion, though this estimate is far higher than what is likely achievable. The budget also saves around $150 billion by reducing or eliminating federal retiree cost-of-living adjustments, eliminating supplemental benefits for federal employees retiring before age 62, increasing the number of salary years used to calculate retirement benefits, and increase federal employee retirement contributions. More than half of these savings would be returned to various agencies, while just over $60 billion would go toward deficit reduction. Other savings come from reducing farm subsidies, enacting financial regulation reform (including restructuring the Consumer Financial Protection Bureau), postal reform, higher Pension Benefit Guaranty Corporation premiums, and a variety of other changes.

Comprehensive Tax Reform (???) – The President’s budget alludes to the Administration’s proposed tax reform but offers no estimates or specific details. The budget calls for lowering individual income tax rates, expanding the standard deduction, eliminating the Alternative Minimum Tax and estate tax, and lowering business tax rates while eliminating special interest tax breaks. This is actually less specific than the one-page tax framework released by the Administration a month ago. We estimated that the details of that framework would likely cost about $5.5 trillion, though additions and adjustments could surely lower that cost. While in the past the White House has said tax reform would be paid for in part by cutting tax preferences and in part through faster economic growth, the budget dedicates all the gains from economic growth toward deficit reduction and none to tax reform. This suggests an inconsistency between past and current assumptions that might be akin to a sort of ‘double-count’ (though there is no explicit double counting within the budget), or – more positively – a new recognition that tax reform should be deficit-neutral without relying on economic growth.

Economic Growth and War Drawdown (-$2.7 trillion) - The budget claims $2.7 trillion in savings that do not represent policy choices. As discussed in the next section, the budget assumes a very rosy economic scenario where annual real GDP growth reaches a sustained 3 percent per year by 2020, generating almost $2.1 trillion in savings from economic feedback. Note that as per long-standing convention, this feedback is built into the Administration’s baseline; however, the Administration also displays it separately. In addition, the budget requests $77 billion in OCO spending for 2018 and assumes a gradual reduction to $12 billion over five years, saving about $650 billion against OMB’s baseline when interest is included. However, this reduced war spending represents a drawdown already underway, may be unlikely to materialize given the budget’s defense increases for the current year, and are marked as “placeholder” values that do not illustrate a specific policy position along with future years' defense funding.

Economic Assumptions

Ultimately, fiscal and economic choices are intertwined. Manageable debt levels and smart tax and spending policies can promote economic growth, while strong economic growth can improve the budget picture. In the President’s budget, unlike estimates made by CBO, the presumed or estimated economic impact of the President’s policies are baked into OMB’s economic assumptions.

Sadly, economic forecasts in this budget are far outside of the mainstream and extremely unlikely to materialize in reality.

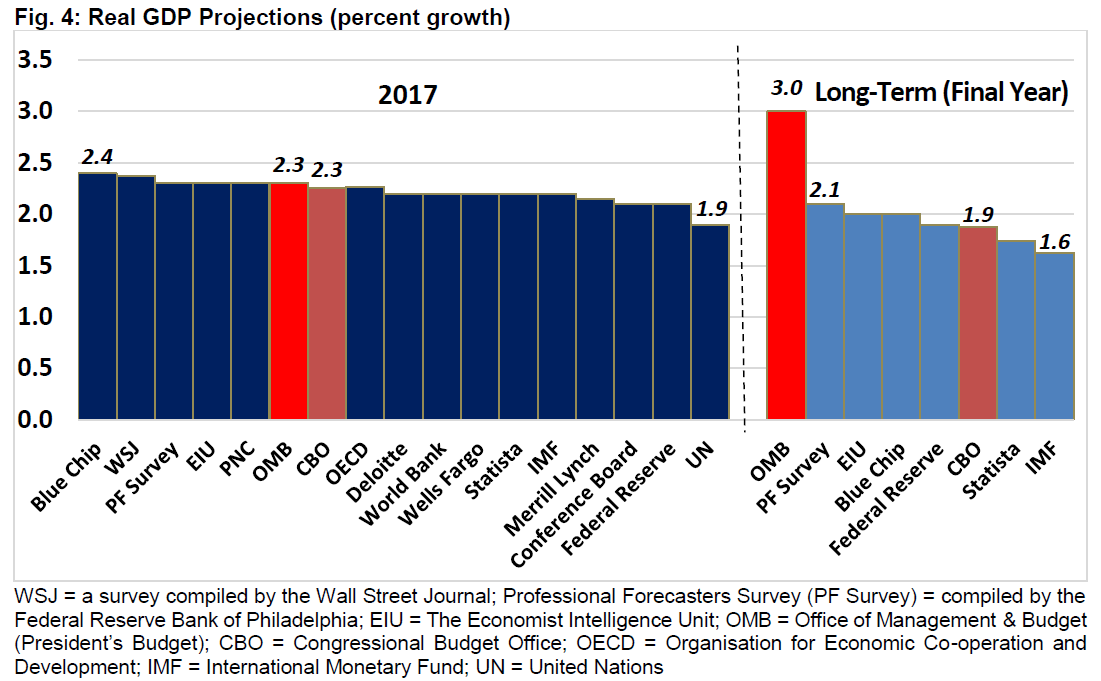

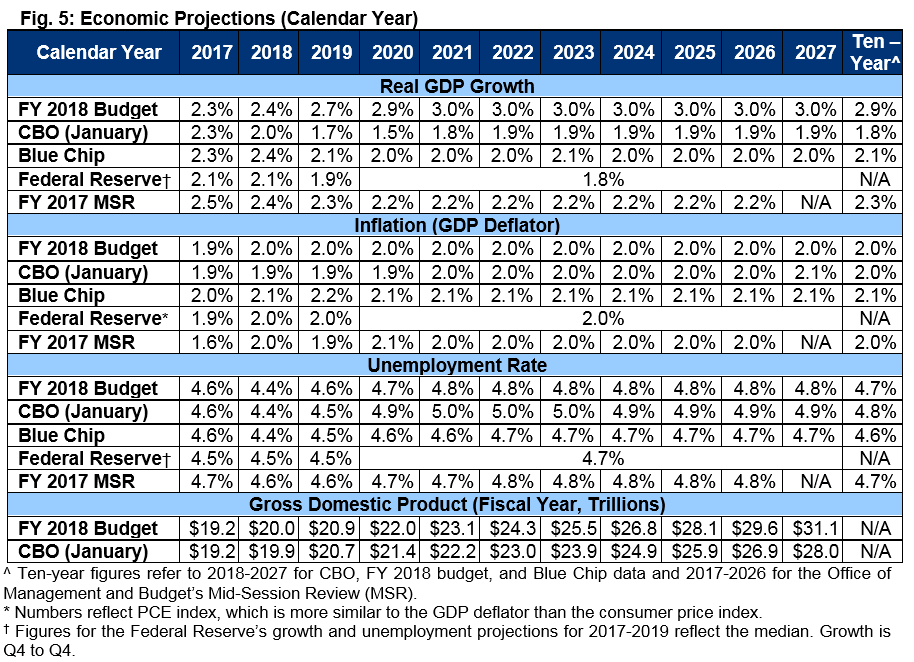

OMB projects real growth rates averaging 2.9 percent over the decade, reaching sustained growth rates of 3.0 percent per year. As we’ve shown before, the likelihood of reaching such levels of growth are quite low; given population aging, achieving 3 percent growth and would require exceeding the economic fundamentals of the 1990s.

OMB’s growth estimates are also far more optimistic than other projections. CBO, for example, projects growth will reach 1.9 percent per year. The Federal Reserve is even more pessimistic, projecting long-term sustained growth of 1.8 percent per year. Even the more optimistic Blue Chip average only projects sustained growth of 2.0 percent.

OMB’s overly optimistic growth assumptions lead to overly optimistic outcomes. By 2027, OMB projects the economy to be 11 percent larger than CBO projects, resulting in roughly $2.7 trillion less in total debt.

As we recently detailed, without these rosy growth assumptions debt would remain roughly stable at 76 percent of GDP, rather than falling below 60 percent of GDP by the end of the decade.

While OMB’s economic growth estimates differ wildly from outside forecasters, its other economic forecasts are well within the mainstream. OMB projects the unemployment rate to dip further from 4.6 percent in 2017 to a low of 4.4 percent in 2018 and then stabilize at 4.8 percent. By comparison, CBO projects the unemployment rate will settle around 4.9 percent, Blue Chip at 4.7 percent, and the Federal Reserve at 4.7 percent as well.

OMB projects inflation, as measured by the GDP deflator, to tick up from 1.9 percent in 2017 to 2.0 annually after. By comparison, CBO and Blue Chip project the GDP deflator will settle at 2.0 and 2.1 percent, respectively. The GDP price index is most comparable to the PCE deflator the Federal Reserve projects to settle at 2 percent.

With regard to interest rates, OMB's projections similar (3.1 and 3.8 percent for the 3-month and 10-year treasuries, respectively) to mainstream interest rates with a slightly quicker return to steady levels than CBO but similarly paced to Blue Chip's average. Projections of both short- and long-term rates are slightly higher than CBO’s 2.8 and 3.6 percent, respectively. However, given the higher projected real GDP growth rate OMB’s interest rate projections are probably a little too low. CBO as a rule of thumb says that a 0.1 percent increase in real growth rate roughly corresponds with a 0.1 percent increase in interest rates after a decade. Higher rates increase the interest cost of our large and growing national debt.

Conclusion

The Administration deserves credit for setting a fiscal goal and for working toward that goal with a number of specific policies that would help to reduce the debt. However, the President’s proposals would not meet his fiscal goal in reality.

Many of the policies in the budget are sensible and thoughtful reforms and are worthy of consideration. Overall, however, these cuts fall disproportionately on programs that benefit children, low-income individuals, and promote investment – an almost inevitable consequence of virtually ignoring the rapid growth of Social Security and Medicare, two of the largest and fastest growing parts of the budget.

The budget unfortunately relies on a number of questionable assumptions to make its math work. It assumes 3 percent sustained economic growth, which would be incredibly difficult to achieve and is far outside the estimates of mainstream forecasters. Absent this assumption, we recently found the budget would stabilize the debt at 76 percent of GDP, rather than reduce debt to 60 percent; it would leave deficits above 2 percent of GDP rather than balancing the budget.

The budget also relies on deep unspecified cuts to non-defense discretionary spending that are both unexplained and unlikely to occur. Finally, the budget omits a tax plan that could end up adding trillions of dollars to the overall debt.

Though the President deserves much praise for paying for all of his new initiatives and putting forward substantial new deficit reduction, his budget stripped of its rosy assumptions doesn’t do enough to put our post-war era record-high debt levels – or our entitlement programs – on a sustainable long-term path.

We hope that Congress and the President will work together over the next year, combining the best parts of this budget with other reforms to restore the country’s fiscal and economic health.