Major Challenges Await the Next Administration

US Budget Watch 2024 is a project of the nonpartisan Committee for a Responsible Federal Budget designed to educate the public on the fiscal impact of presidential candidates’ proposals and platforms. Through the election, we will issue policy explainers, fact checks, budget scores, and other analyses. We do not support or oppose any candidate for public office.

The winner of the 2024 presidential election will face many fiscal challenges, some of which are new, and some of which have been around for many years. Most are growing increasingly urgent. Fiscally responsible candidates should explain how they will address these challenges as well as detail how they will pay for any new proposals.

The winner of the 2024 presidential election will face:

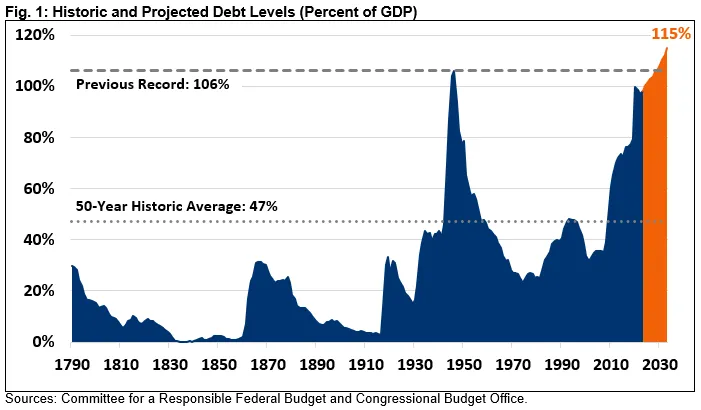

- Record Debt Levels. Debt held by the public is on course to reach a record 107 percent of GDP by the end of fiscal year (FY) 2029 – the fiscal year during which the next presidential term will end – exceeding its prior record set just after World War II. By 2033, debt will reach 115 percent of GDP or even higher if lawmakers continue irresponsible fiscal decision-making.

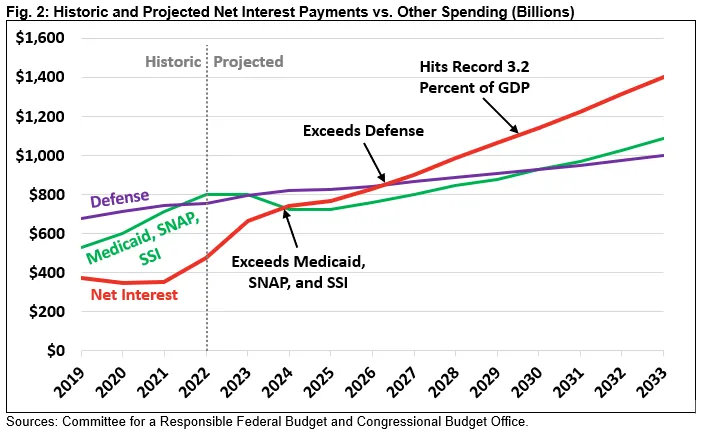

- Growing Interest Costs. Over the next presidential term, interest will be the fastest-growing part of the budget. Interest costs are projected to exceed total defense spending by FY 2027 and reach a record 3.2 percent of GDP by FY 2030.

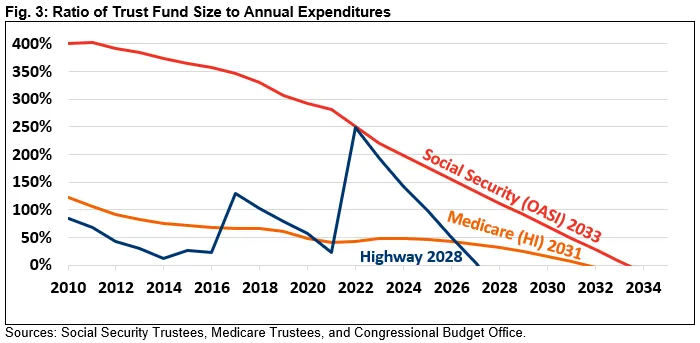

- Looming Trust Fund Insolvency. The Highway Trust Fund is projected to run out of reserves during the next presidential term in 2028. The Medicare Hospital Insurance trust fund is projected to run out three years later (2031), and Social Security’s Old-Age trust fund two years after that (2033). Action must be taken to avoid automatic, across-the-board cuts upon insolvency.

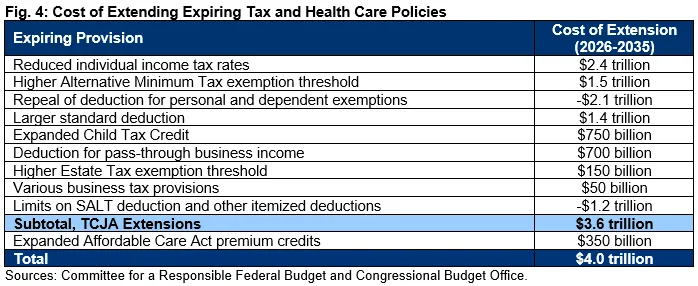

- Major Expirations and the Risk of Costly Extensions. In October 2025, the recently enacted statutory caps on appropriations will expire. By the end of 2025, major provisions in the Tax Cuts and Jobs Act of 2017 and the recent expansion of Affordable Care Act health insurance subsidies will expire as well. These expirations should be dealt with responsibly in order to improve the budget outlook rather than adding trillions of dollars to the debt.

Whoever occupies the Oval Office in 2025 will not be able to ignore these issues. Instead, candidates should be honest with voters about these challenges during the campaign and detail how they plan to address them.

Debt Will Reach Record Levels

The national debt is projected to reach a new record as a share of the economy just after the next presidential term and, in reality, is very likely to reach that record during that term. The Congressional Budget Office (CBO) projects federal debt held by the public will reach 107 percent of Gross Domestic Product (GDP) by the end of FY 2029 – more than twice the 50-year historic average of 47 percent and above the previous record of 106 percent set just after World War II.

Debt is projected to reach 115 percent of GDP by the end of the decade under current law, and is likely to rise even higher in reality. CBO’s projections do not account for lower-than-expected revenue collections this year, nor do they incorporate a number of appropriations “side deals” that are likely to boost spending. They also assume various expiring provisions are allowed to lapse as scheduled. Relaxing these and other assumptions, we previously estimated debt could reach record levels as early as 2026 and exceed 140 percent of GDP by 2033.

In nominal dollars, CBO projects debt to breach $35 trillion by the end of the next presidential term, with about $6 trillion – or 4 percentage points of GDP – added over the term. Although this debt will come almost entirely from actions taken prior to the next presidential term, it nonetheless means that the next administration could lead America into uncharted fiscal territory.

This level of borrowing will add to inflationary pressures, slow income growth, make it more difficult to borrow in the future to respond to recessions or emergencies, increase our exposure to geopolitical risk, exacerbate generational unfairness, and increase the risk of a fiscal crisis.

Interest Costs Will Rise

Interest costs will be the fastest-growing part of the federal budget over the next presidential term. By the end of the current presidential term, CBO projects interest costs will have more than doubled, growing from $352 billion (1.6 percent of GDP) in FY 2021 to $769 billion (2.7 percent of GDP) in 2025. Interest costs are projected to further rise to $1.1 trillion by 2030, reaching the previous record of 3.2 percent of GDP, and then to $1.4 trillion (3.6 percent of GDP) by 2033.

To put these figures in context, the federal government already spends more on interest than on children. By 2024, interest will cost more than the federal share of Medicaid, the Supplemental Nutrition Assistance Program (food stamps), and Supplemental Security Income combined. By 2027, during the next presidential term, interest spending will exceed federal defense spending.

Interest costs are projected to total $10.4 trillion over the next decade, accounting for more than half of the $18.8 trillion in projected deficits and leaving less room for everything else.

Should interest rates rise, rather than remain relatively flat as projected, interest costs would grow even further. Each 1 percentage point increase in interest rates would increase deficits by about $2.7 trillion over a decade, relative to CBO’s baseline.

Trust Funds Will Approach Insolvency

Over the coming decade, three major trust fund programs will face insolvency: the Highway Trust Fund, the Medicare Hospital Insurance (HI) trust fund, and Social Security’s Old-Age and Survivors Insurance (OASI) trust fund. These three programs are funded with dedicated revenue, and partially rely on trust fund reserves to fully fund payments. By law, these programs can only spend as much as they collect in current revenue, which means sharp benefit and spending cuts will be triggered upon trust fund insolvency.

According to CBO, the Highway Trust Fund will deplete its reserves by 2028, at which point all highway spending will be cut by 47 percent absent new legislation. The Medicare Trustees estimate that the Medicare HI trust fund will be exhausted by 2031, at which point Medicare Part A spending will be cut by 11 percent. Finally, the Social Security Trustees project that the OASI trust fund will be depleted by 2033, at which point retirement benefits will be cut by 23 percent.

These scheduled cuts would be deep, immediate, and across-the-board. For example, today’s youngest retirees would all face an immediate 23 percent Social Security benefit cut at age 72, regardless of income. That same cut would apply to today’s 57-year-olds when they reach the full retirement age and today’s 80-year-olds when they turn 90.

The President must work with Congress to avoid these harmful cuts in a fiscally responsible way, either by raising new revenue, slowing cost growth, or a combination of both. Thoughtful reforms could promote economic growth, reduce health care costs, support higher-value infrastructure, improve tax fairness and efficiency, and strengthen retirement security for vulnerable Americans.

Changes should be enacted well ahead of trust fund deadlines to allow time for policies to phase in gradually and to give workers, beneficiaries, and providers time to plan and adjust.

Major Policies Will Expire

In the first year of the next presidential term, policymakers will need to contend with the end of the recently agreed-upon discretionary spending caps and the expiration of several major tax and health care policies. Extending these tax and health provisions in their entirety would cost roughly $4 trillion from FY 2026 through FY 2035.

The first of these deadlines comes October 1, 2025, when the new fiscal year requires the passage of defense and nondefense appropriations. Unlike in FY 2024 and 2025, there will be no statutory cap to limit how much those appropriations can cost. Spending levels in that year, and decisions over whether to extend the caps, could have significant fiscal implications for years to follow.

Three months later, at the end of 2025, most individual income tax provisions from the 2017 Tax Cuts and Jobs Act (TCJA) are scheduled to expire. As a result, all individual rates will rise, the Child Tax Credit and standard deduction will shrink, the Alternative Minimum Tax and Estate Tax will expand, the deduction for pass-through business income will disappear, the personal exemption will return, and various tax preference limits – most notably the $10,000 cap on the state and local tax (SALT) deduction – will end. At the same time, a temporary expansion of the Affordable Care Act, which boosted insurance subsidies across-the-board and capped costs on the exchanges at 8.5 percent of income, is also scheduled to end.

Extending all these provisions without offsets would cost about $4 trillion over the subsequent decade – adding more than 10 percentage points of GDP to the debt. Costs could rise above $5 trillion if base-broadening measures such as the SALT cap are not extended.

The President will need to work with Congress to set new spending levels and address these expirations. A responsible plan would involve setting multi-year spending caps, letting some (or all) of the tax and health provisions expire as intended, and identifying reforms and offsets to ensure any remaining extensions do not add to the national debt.

Conclusion

Whoever wins the 2024 presidential election must be prepared to confront a myriad of challenges. With the national debt approaching a new record high and interest costs accelerating, the looming insolvency of critical trust fund programs, and multiple significant tax and spending provisions expiring, it is critical that whoever is elected to occupy the Oval Office in 2025 takes steps to address these issues.

It is especially important that the winner of the 2024 presidential election makes fiscal responsibility a key priority. Due in part to policies necessary to combat the COVID pandemic and related economic downturn, the federal government added nearly $9 trillion to our national debt over just the last four years. Recent legislation has helped to improve the nation’s fiscal outlook, but it remains on an unsustainable trajectory, and far more will need to be done.

As the 2024 presidential election proceeds over the coming months and candidates begin to unveil their policy platforms, voters should expect candidates to acknowledge these challenges directly and present clear, concrete, and workable solutions. In prior elections, many of the challenges discussed in this paper were still long-term issues, but no longer. Candidates must realize the need to confront many of these challenges within the next presidential term. Neither the candidates nor voters can afford to kick the can down the road any longer.

Throughout the 2024 presidential election cycle, US Budget Watch 2024 will bring information and accountability to the campaign by analyzing candidates’ proposals, fact-checking their claims, and scoring the fiscal cost of their agendas.

By injecting an impartial, fact-based approach into the national conversation, US Budget Watch 2024 will help voters better understand the nuances of the candidates’ policy proposals and what they would mean for the country’s economic and fiscal future.