The Progressive Caucus "People's Budget"

The Congressional Progressive Caucus (CPC) released their “The People’s Budget: A Roadmap for the Resistance.” The budget is the first release in this year's Fiscal Year (FY) 2018 budget season, coming before either the President's budget or any proposal from the Budget Committees. It includes dramatic increases in infrastructure and education spending and a wide range of tax increases focused on high earners. It contains enough budget savings to keep debt roughly at its current level over the next ten years, an improvement from its current upward trajectory. However, the budget does not put debt on a downward path, like in previous years.

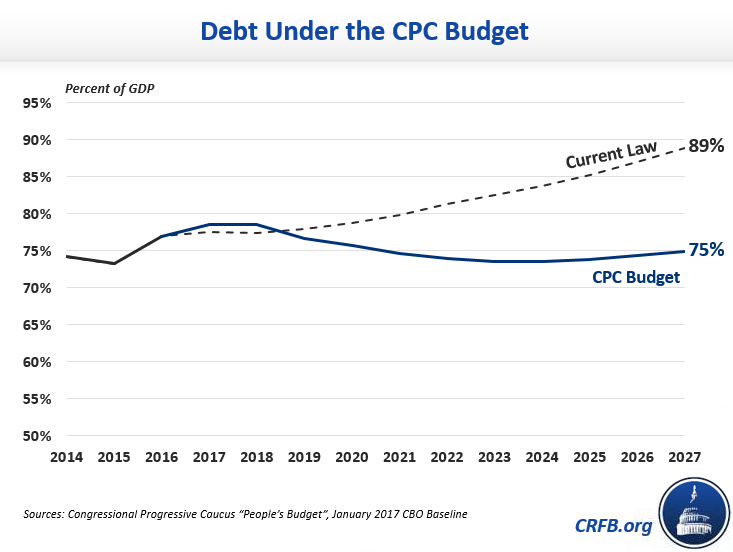

The CPC's budget proposes both higher taxes and higher spending in most areas. It calls for $9.6 trillion of gross savings and $6.6 trillion in investments and other costs over ten years, resulting in $3.0 trillion of deficit reduction over the next decade, including interest savings. This deficit reduction would roughly keep debt constant from today's level of 77 percent of Gross Domestic Product (GDP) to end at 75 percent of GDP in 2027. By contrast, the Congressional Budget Office (CBO) baseline projects that debt will rise to 89 percent by 2027.

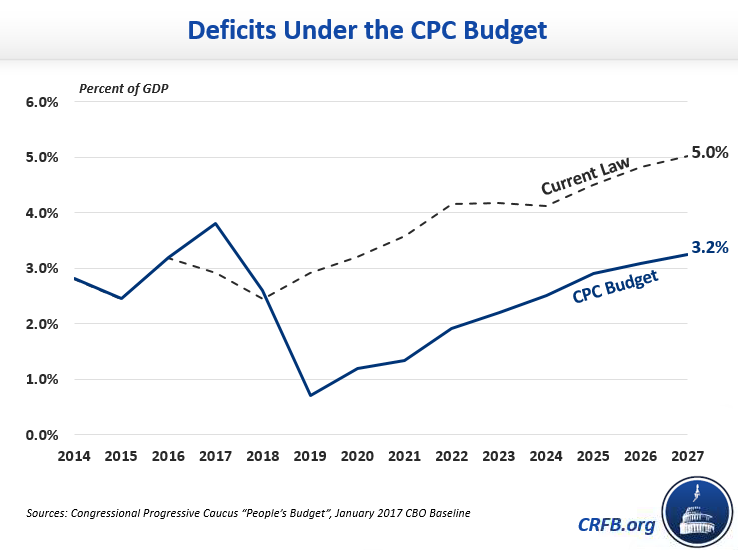

Under the People’s Budget, revenues would rise from 17.8 percent of GDP this year to 22.1 percent by 2027, about 4 percent of GDP higher than under current law. Outlays would increase from 20.7 percent of GDP in 2017 to reach 25.3 percent in 2027, or about 2 percent of GDP percent higher than under current law. Because of a little short-term stimulus, the 2017 deficit would shoot up to 3.8 percent of GDP, about 1.5 percent of GDP higher than current law. After that, deficits fall to a low of 0.7 percent of GDP in 2019 and end up at 3.2 percent of GDP at the end of the ten-year period, well below the 5 percent deficit CBO expects. Deficits would be increasing at the end of the ten-year window.

The budget includes sizeable spending increases in areas like infrastructure ($2 trillion through 2027), child care ($1 trillion through 2027), and higher education ($443 billion through 2027). In addition, the plan would repeal both the sequester and the original spending caps on non-defense spending, returning this category to its historical average as a percentage of GDP by 2022. On the tax side, it would enact job creation tax credits, expand current child care credits, and increase the Earned Income Tax Credit for childless workers.

The budget raises revenue by significantly changing tax rates. For very high earners, the budget raises top rates from 39.6 percent to a range between 45 and 49 percent for incomes over $1 million and over $1 billion, respectively, and taxes capital gains and dividends as ordinary income. It lowers the estate tax exemption to $3.5 million with rates between 55 and 65 percent and eliminates step-up basis for capital gains at death. The budget also includes President Obama’s $10.25 per barrel tax on oil to eliminate the Highway Trust Fund shortfall, a carbon tax, a financial transactions tax, and would move to a worldwide tax system where all foreign-earned income of U.S. businesses is taxed in the year it is earned. Though the budget proposes substantial tax increases, it appears the revenue raised from a financial transactions tax is about $1.2 trillion higher than what the Tax Policy Center thinks is achievable (the Tax Policy Center has estimated that transactions tax revenue would max out around $50 billion per year).

The plan also makes some health care changes. The budget would accelerate the use of bundled payments and repeal the Cadillac tax on high-cost health insurance plans, replacing it with a public option in the health exchanges. The budget also gives the Department of Health and Human Services authority to negotiate prescription drug costs in Medicare Part D – potentially using President’s Obama's Medicare drug rebate for savings since negotiation itself would save little.

Major Proposals in Congressional Progressive Caucus Budget

| Policy | 2016-2026 Savings/Costs (-) |

|---|---|

| Deficit Reduction Proposals | |

| Implement financial transactions and financial institution taxes | $1,909 billion |

| Enact worldwide taxation system and limit foreign tax credit | $1,708 billion |

| Increase tax rates on income above $250,000 (inc. capital gains/dividends) | $1,597 billion |

| Enact carbon tax (refunding 25% to households) and repeal fossil fuel tax preferences | $907 billion |

| Enact public option and prescription drug savings | $790 billion |

| Cap the value of itemized deductions at 28% | $577 billion |

| Repeal step-up basis and institute estate tax reform | $413 billion |

| Close John Edwards/Newt Gingrich loophole | $318 billion |

| Enact immigration reform | $301 billion |

| Enact $10.25 per barrel oil tax | $299 billion |

| Reform the corporate tax code | $128 billion |

| Reduce defense spending | $116 billion |

| Other policies | $193 billion |

| Net Interest savings | $381 billion |

| Subtotal, Deficit Reduction | $9.6 trillion |

| New Investment Proposals/Other Costs | |

| Repeal sequester and spending caps | -$692 billion |

| Further increase non-defense spending | -$1,640 billion |

| Increase infrastructure spending | -$1,975 billion |

| Subsidize "Child Care for All" | -$993 billion |

| Create and expand job creation and education programs | -$489 billion |

| Refinance student loans and other college cost proposals | -$443 billion |

| Boost childcare and early education proposals | -$144 billion |

| Repeal Cadillac tax | -$132 billion |

| Other investment proposals/costs | -$136 billion |

| Subtotal, New Investments | -$6.6 trillion |

| Subtotal, Policy Savings | $3.0 trillion |

| Draw down war spending starting in 2017* | $975 billion |

| Total Savings | $3.9 trillion |

Source: Congressional Progressive Caucus.

Note: Totals may not add due to rounding.

*Includes interest savings

The budget certainly contains a lot of tax and spending increases, but we welcome budget alternatives that improve the debt situation. While it's disappointing that the Congressional Progressive Caucus doesn't put debt on a downward path like in previous years, it would represent a substantial improvement over our current debt trajectory.