Johnson and Larson Show Two Ways to Fix Social Security

Yesterday, House Ways and Means Social Security Subcommittee Ranking Member John Larson (D-CT) introduced a Social Security reform bill. About four months ago, we wrote about a different Social Security plan from the subcommittee's chairman.

Social Security's long-term imbalance represents one of our most serious fiscal challenges and one that most lawmakers are all too willing to ignore. That is why it is encouraging that the top Republican and Democrat on the Social Security Subcommittee have now both introduced plans to make the program solvent for the next 75 years and beyond. Larson’s Social Security 2100 Act and subcommittee chair Sam Johnson’s (R-TX) Social Security Reform Act show two very different ways of fixing Social Security, but they share key areas of agreement that could show the foundations of an eventual bipartisan compromise.

Johnson and Larson Both Agree on Sustainable Solvency

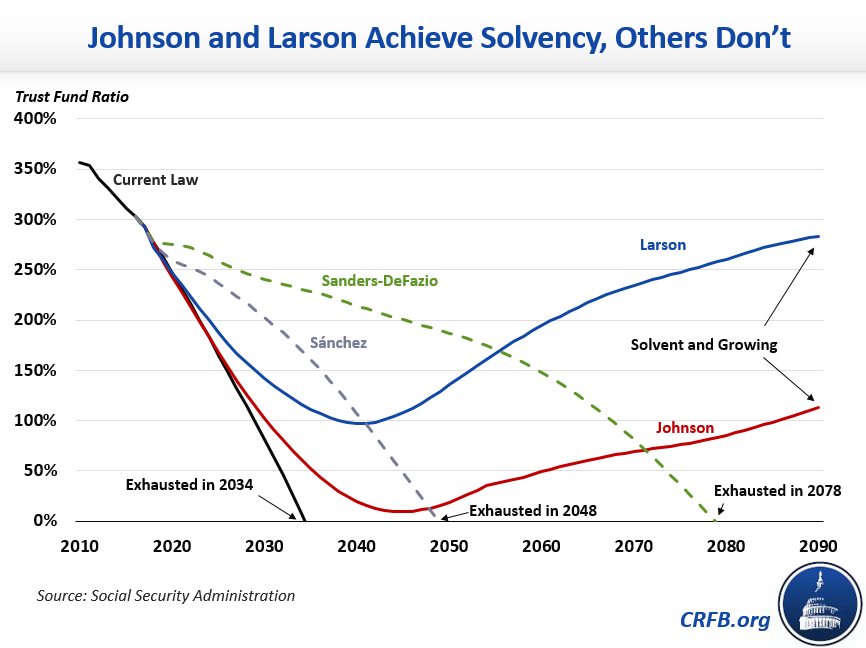

First and foremost, both Johnson and Larson share the goal of not only preventing the 21 percent cut in benefits for all current and future beneficiaries that will otherwise occur when the Social Security trust fund runs dry in 2034 but also making the program financially sound for the foreseeable future. Social Security's Office of the Chief Actuary has evaluated each of their plans and found that both would meet the actuaries' standard of sustainable solvency, making Social Security solvent for the next 75 years and leaving the program with a growing trust fund at the end of the valuation period.

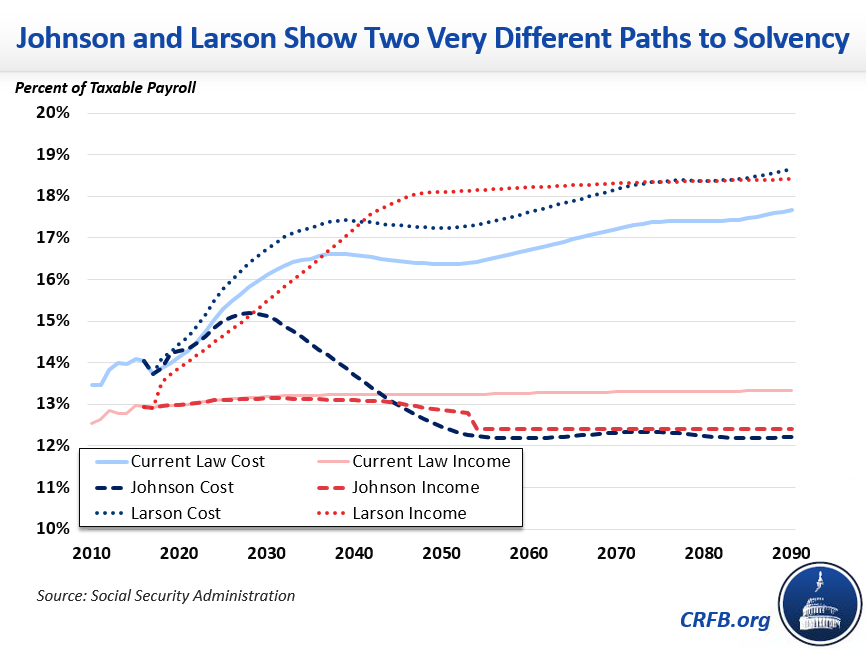

By 2090, Johnson's plan would have run a small surplus, while Larson's plan would run only a very small deficit (and have built up a larger trust fund). This is hugely important as it means that Social Security is financially sound, not just actuarially afloat, providing some assurance that policymakers won't have to revisit solvency in the near future (when far fewer options will be available).

That both plans achieve this important goal is especially important since it stands in sharp contrast to a host of recent proposals that would fall far short. One plan by Senator Bernie Sanders (I-VT) and Representative Peter DeFazio (D-OR), for example, would extend solvency just 44 years and close only half of Social Security's structural gap. Another plan from Representative Linda Sánchez (D-CA) would extend the solvency of the trust fund only 14 years and close just one-twentieth of Social Security's structural gap, using virtually all of the plan's new taxes to finance across-the-board benefit increases.

Johnson and Larson Share Other Principles

Johnson and Larson also agree in principle on concentrating most of the changes necessary to close the shortfall on those with higher incomes while also asking for some contribution from the middle class. Larson would improve solvency mainly by taxing earnings above an unindexed $400,000 threshold (all wages would be taxed once the current $127,200 cap exceeds $400,000) and by gradually raising the payroll tax from 12.4 to 14.8 percent on all workers. Johnson would improve solvency mainly by slowing benefit growth for higher earners but also by raising the retirement age from 67 to 69 for all workers.

This shows agreement that Social Security reform should be progressive, but recognizing that solvency can't be achieved simply by making the rich pay the same as everyone else or means-testing their benefits.

Both the Johnson and Larson proposals also increase progressivity by strengthening Social Security’s anti-poverty protections. They do so both by creating a new minimum benefit for low-wage workers and by increasing the standard benefit formula at the lower end (Larson would increase the bottom replacement factor from 90 to 93 percent, Johnson to 95 percent).

Finally, both reduce the share of Social Security benefits subject to the income tax, with Johnson eliminating the tax on benefits altogether in later years.

The Johnson and Larson Plans Differ Significantly

Yet despite these commonalities, the two plans are starkly different. Johnson’s proposal would close the financing shortfall entirely by slowing cost growth and even use some of the savings to cut taxes. Larson’s plan, on the other hand, would close the shortfall entirely by increasing taxes and even use some of that revenue for benefit increases.

In terms of aggregate spending and revenue levels, the two plans are nearly mirror images of one another. Under current law, by 2090 Social Security spending is projected to total 17.7 percent of taxable payroll, while revenue is projected to total 13.3 percent. Under the Johnson plan, spending and revenue would both total less than 12.5 percent of payroll, while under the Larson plan thye would would be closer to 18.5 percent of payroll.

The plans also differ diametrically on some specific choices. Larson would increase cost-of-living adjustments (COLAs) across-the-board by adopting the experimental CPI-E, a measure he argues would more accurately reflect seniors' cost of living but that we and many other experts find to be quite flawed. Johnson's plan would reduce COLAs across the board by adopting the chained CPI, which we've explained in the past is a more accurate measure of inflation and has been a part of many solvency plans. Perhaps more significantly, Johnson's plan would eliminate COLAs altogether for any beneficiary with annual income above $85,000 ($170,000 for couples), with the thresholds indexed for inflation.

Moreover, to the extent the plans do agree in some areas it is often in direction but not magnitude. While both would reduce income taxes on Social Security benefits, Johnson's plan would ultimately eliminate them while Larson's plan would retain them. And while both would include benefit increases, Johnson's enhancements are much more targeted to low-income groups while Larson's enhancements span all the way up the income ladder.

Each Plan Starts In Its Own End Zone, But They Are Playing the Same Game

To fix Social Security, policymakers will ultimately need to agree to slow the growth of spending on benefits, increase tax revenue, or most likely both. The plans put forward by Johnson and Larson are quite partisan, the former being an all-spending solution and the latter being an all-tax solution. Yet in a possible breakthrough relative to the recent debate, both teams believe in the same goal. Both plans accept the premise that Social Security must be made sustainably solvent – not just for 14 years or even 75 years but for the foreseeable future.

Agreeing to a common goal is the first step toward agreeing to a common plan. And where better to start than with a negotiation between the Chairman and Ranking Member of the Social Security Subcommittee?

Between the two plans, they have enough policies to achieve solvency nearly three times over. That suggests plenty of room for compromise and plenty of opportunity to meet at the 50-yard line.

The two can also look to the many other bipartisan plans that have offered a path forward.

They can also visit SocialSecurityReformer.org and design a plan using our newly-updated 'Social Security Reformer' tool. But whatever they do, they should act fast. Despite plenty of myths about the program's finances, time is running out to make sure Social Security remains strong for future generations.